|

|

市場調査レポート

商品コード

1910621

保険詐欺検知:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Insurance Fraud Detection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 保険詐欺検知:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 149 Pages

納期: 2~3営業日

|

概要

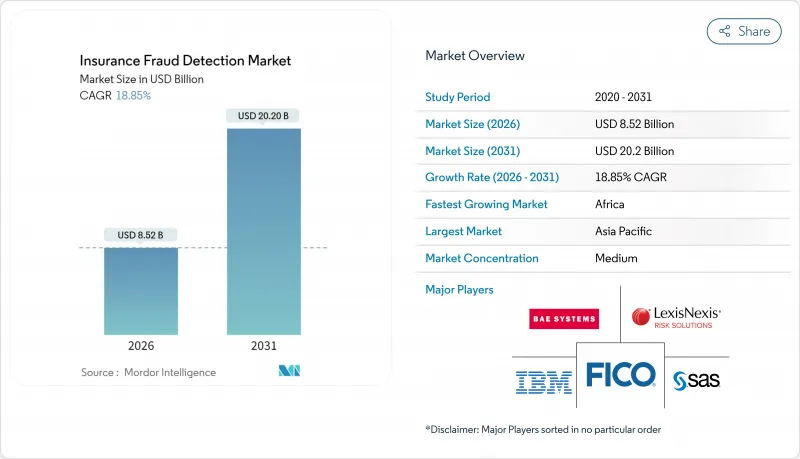

保険詐欺検知市場は、2025年に71億7,000万米ドルと評価され、2026年の85億2,000万米ドルから2031年までに202億米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは18.85%と見込まれます。

リアルタイム分析、AIを活用した保険金請求の自動化、クラウドネイティブ展開が、採用曲線を拡大する主な要因です。大手保険会社は現在、毎秒数百万件の取引を処理しており、規制当局は手作業によるワークフローをコスト面で非現実的なものとする厳しい民事罰則を課しています。アジア太平洋地域はモバイルファーストの保険モデルを通じてイノベーションのペースをリードし、北米ではテレマティクスとID管理を融合した高度な行動分析の規模拡大が進んでいます。競合の激しさは、単体ソリューションの精度からシームレスなエコシステム統合へと移行しており、これにより小規模なSaaSベンダーが既存のメインフレームベンダーからシェアを奪うことが可能となっています。

世界の保険詐欺検知市場の動向と洞察

急増するデジタル身元の効果的管理の必要性

合成身元情報が急増し、保険会社はフロントエンド検証プロトコルの強化を迫られています。消費者は15~20のデジタル接点を通じて保険会社とやり取りしますが、それぞれが不正な身元情報の侵入経路となり得ます。LexisNexis Risk Solutionsは2025年2月にIDVerseを買収し、ツールキットを強化。身分証明書を99.7%の精度で検証するディープフェイク検出機能を追加しました。保険会社は現在、デバイスインテリジェンス、生体認証信号、行動分析を融合させ、異なるチャネルにまたがる単一の顧客をマッピングすることで、詐欺グループに悪用される抜け穴を塞いでいます。

大手保険会社におけるAIを活用した保険金請求自動化の急増

主要保険会社は、検知精度を損なうことなく手動審査を最大85%削減しました。フェアアイザック社は2024年第4四半期にプラットフォームの経常収益が31%増加したと報告しており、これは主に140のティア1金融機関におけるAI中心の導入が牽引したものです。自然言語処理とコンピュータビジョンが数秒で査定員のメモ、写真、動画フィードを分析し、支払いが実行される前に仕組まれた事故や水増し請求書を検知します。

高い誤検知率が査定員の生産性を低下させています

一部のAIモデルは正当な請求の30%以上を誤検知し、人間の審査担当者を圧倒し、決済サイクルを延長させています。保険会社は感度と特異性のバランスを取る必要がありますが、精度85%以上を維持しつつ誤検知率を15%未満に抑えることは依然として困難です。企業は、単純なルール、教師あり学習、ネットワーク分析をカスケード処理するアンサンブルモデルを多層化することで、不正検知率を低下させることなくノイズを低減しています。

セグメント分析

2025年時点で、保険詐欺検知市場の72.64%をソリューションが占めており、データ取り込み・リアルタイムスコアリング・ケース管理を統合したエンドツーエンドプラットフォームへの業界の継続的な依存を反映しています。しかしながら、保険会社がモデル調整、規制報告、第三者データオーケストレーションを外部委託する動きに伴い、サービス分野は19.05%のCAGRで拡大中です。この変化は、AIモデルが新たな不正パターンや地域ごとの規則変更を追跡するために継続的な調整を必要とする認識が高まっていることを示しています。ベンダーは現在、サブスクリプション契約にマネージドサービスを含めることで、社内データサイエンスチームに負担をかけずにアルゴリズムを最新の状態に保つことを保証しています。

マネージドサービス契約では通常、コンソーシアムデータのオンボーディング、モデルの説明可能性テスト、定期的なバイアス監査が対象となり、これら全てがプラットフォームの定着率向上に寄与します。クラウドネイティブの専門家は、8週間以内に不正検知エンジンを保険金請求・保険契約・請求管理システムに接続する統合ノウハウを提供します。大手保険会社はカスタム機能設計のためサービスチームを活用する一方、中堅企業は機能ギャップ解消のため既成テンプレートに依存しています。サービスに紐づく保険詐欺検知市場の規模は、従量制ソフトウェア販売から継続的な成果ベース契約への戦略的移行を反映しています。

2025年における保険詐欺検知市場規模の38.10%を占める支払・請求詐欺が最大分野であり、デジタル保険料徴収と自動支払いの急増が背景にあります。マネーロンダリング検知は最も急成長している応用分野であり、規制当局が保険会社に従来型銀行チャネルを超えた複数管轄区域にわたる資金の流れの監視を要請する中、20.78%のCAGRを記録しています。請求詐欺と個人情報盗難は、再利用された写真や改ざんされたメタデータを検知する画像フォレンジックモジュールに支えられ、着実な成長を続けています。

グラフ分析技術は、一見無関係な保険契約間における多層的な資金移動を可視化し、不正資金を流用するペーパーカンパニーネットワークを暴露します。AIエンジンは取引ごとに500以上の属性(デバイスフィンガープリント、地理的位置変動、暗号通貨ウォレットの痕跡など)を複合的に評価します。ブロックチェーン分析を導入した保険会社では、従来ルールと比較し調査サイクル時間が35%短縮されたと報告されています。デジタルウォレットとリアルタイム決済が普及する中、プラットフォームベンダーは、より広範な保険詐欺検知市場において、生命保険、健康保険、損害保険の各分野にまたがる複雑なスキームを阻止するため、製品横断的な相関分析を優先しています。

地域別分析

2025年にはアジア太平洋地域が33.25%のシェアで主導的立場にあり、モバイルファースト製品と、本人確認を効率化する国家デジタルIDフレームワークが基盤となっています。中国とインドでは、社会信用スコアと生体認証チェックを統合し、詐欺リスクのセグメンテーションを精緻化する詳細な行動データセットを生成しています。インドネシアとベトナムのスタートアップ企業は、接続が不安定な地方地域で必須となるオフライン対応のエッジコンピューティングモデルをカスタマイズしています。日本の保険会社はスマートホームデバイス向け組み込み保険の試験運用を開始し、センサーデータを活用して不正な水害請求を未然に防止しています。

アフリカはCAGR21.05%で最も急成長している地域です。モバイルマネー保険が流通を支配し、2024年には主要市場で身分詐称が400%増加しました。エッジに展開された機械学習モデルは、低電力デバイス上で0.3秒未満で不正を判定します。この革新技術は現在、欧州の地方保険会社へ逆輸出されています。地域規制当局は保険金請求データへのエンドツーエンド暗号化を義務付け、帯域幅制約の現実に対応した軽量暗号ライブラリの開発を現地ベンダーに促しています。

北米では厳格な規制監督と行動バイオメトリクスの先駆的導入が両立しています。保険会社は先進運転支援システムからのセンサーデータを統合し、組織的な事故を検知します。カナダのデータローカリゼーション政策はハイブリッド展開を促進し、米国保険会社はコンソーシアムリポジトリを活用して請求者の履歴を相互検証します。欧州はGDPR準拠AIに注力し、生データの交換なしに詐欺モデルを訓練するフェデレーテッドラーニングなどのプライバシー保護技術が主導しています。eIDAS 2.0に基づくデジタルIDウォレットは、まもなく欧州全域での保険金請求認証を可能にし、保険詐欺検知市場が国境を越えたワークフローを標準化する新たな手段を生み出します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ゼロ欠陥製造への需要の高まり

- ビジョンガイデッドロボティクスの普及拡大

- 電子機器の小型化に伴う3Dビジョンの需要拡大

- 食品および医薬品に対する厳格な品質基準

- デバイス内蔵型AI推論チップの急増

- サービスとしてのビジョン(Vision-as-a-Service)サブスクリプションモデルの台頭

- 市場抑制要因

- 熟練したマシンビジョン統合業者の不足

- 高解像度およびハイパースペクトルカメラの高コスト

- クラウド接続型ビジョンシステムにおけるサイバーセキュリティリスク

- イメージセンサー半導体のサプライチェーン変動性

- 業界エコシステム分析

- マクロ経済要因の影響

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- コンポーネント別

- ハードウェア

- ビジョンシステム

- カメラ

- 光学および照明システム

- フレームグラバー

- その他のハードウェア

- ソフトウェア

- ハードウェア

- 製品タイプ別

- PCベース

- スマートカメラベース

- イメージングタイプ別

- 2Dイメージング

- 3Dイメージング

- ハイパースペクトルおよびマルチスペクトルイメージング

- エンドユーザー業界別

- 自動車

- 電子機器および半導体

- 食品・飲料

- 医療・医薬品

- 物流および小売

- その他のエンドユーザー産業

- 展開モード別

- オンプレミス

- エッジ/組み込み

- クラウドベース

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- オランダ

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東

- 湾岸協力会議

- トルコ

- イスラエル

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- ケニア

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Cognex Corporation

- Keyence Corporation

- Omron Corporation

- Teledyne Technologies Incorporated

- Sony Group Corporation

- Atlas Copco AB(ISRA Vision)

- IDS Imaging Development Systems GmbH

- National Instruments Corporation

- MVTec Software GmbH

- Basler AG

- Allied Vision Technologies GmbH

- TKH Group NV(LMI Technologies)

- FLIR Systems Inc(Teledyne)

- Intel Corporation

- Qualcomm Technologies Inc

- Sick AG

- Panasonic Holdings Corporation

- Stemmer Imaging AG

- Zebra Technologies Corporation

- Hitachi Ltd.