|

|

市場調査レポート

商品コード

1851112

半導体機器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Semiconductor Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 半導体機器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月26日

発行: Mordor Intelligence

ページ情報: 英文 146 Pages

納期: 2~3営業日

|

概要

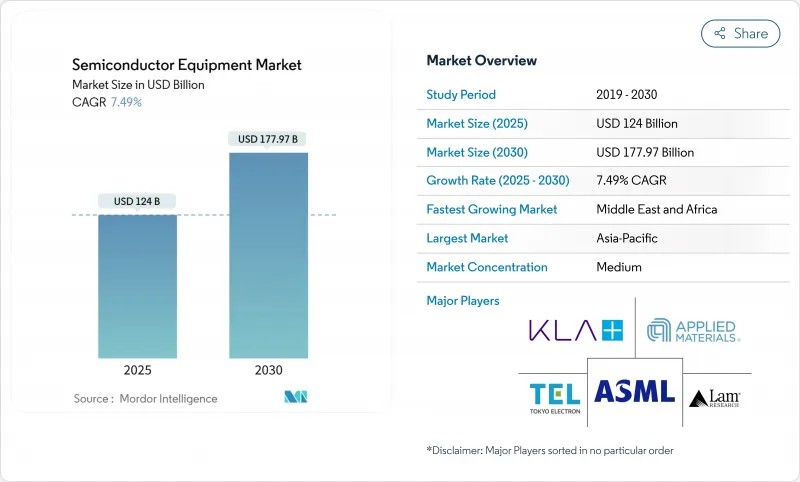

半導体機器市場規模は2025年に1,240億米ドルとなり、2030年にはCAGR 7.49%で1,779億7,000万米ドルに達すると予測されます。

堅調なファブ建設、記録的な設備受注残、相次ぐ政府のインセンティブがこの軌道を支えています。鋳造工場は2nm以下の生産能力を加速させており、一方、半導体組立・テストアウトソーシング(OSAT)企業は人工知能(AI)需要に対応するため先進パッケージラインを拡張しています。技術主権を達成しようとする地政学的な努力が資本支出パターンを形成しており、装置ベンダーは中国での輸出規制と北米、欧州、中東での補助金を原資とするビジネスチャンスとの両立を余儀なくされています。プロセスの幅広さ、ソフトウェア分析、サービスカバレッジを束ねた装置メーカーは、この分野の最大手投資家から複数年の購入を確約してもらっています。

世界の半導体機器市場の動向と洞察

先端家電とスマートフォンへの需要急増

スマートフォン、ウェアラブルデバイス、複合現実デバイスは、ロジック、メモリ、アナログコンテンツを追加し続けており、これらのデバイスはこれまで以上に微細なノードで製造する必要があるため、鋳造工場は28 nm~7 nmラインの生産能力を加速させています。電力バジェットを上げることなく高帯域幅機能を小型化する先進パッケージングが、2025年初頭の収益のかなりの部分を占め、バンプ装置、テスト装置、リソグラフィ装置のアップグレードの波を引き起こしました。チップを垂直に積み重ねる異種集積ラインは2桁の成長率で拡大し、フリップチップボンダやウエハーレベル検査装置の出荷を押し上げました。消費者向け製品のサイクルが厳しくなる中、レシピ切り替えの速いモジュール式成膜チャンバーを提供するツールメーカーが受注を獲得しています。インドと東南アジアでは、携帯電話のリフレッシュ率が高く、成熟したノードツールはフル稼働に近い状態で稼動しており、プレミアムデバイスの発売時でも回復力のある請求が達成可能であることを証明しています。

AI、IoT、エッジデバイスノードへの急速な投資

データセンター事業者は、より高いTOPS/Wを提供するチップを求めており、3nm以下で使用される極端紫外線(EUV)スキャナーや原子層堆積モジュールの調達を後押ししています。米国と欧州のAIアクセラレータ新興企業は、複数年のHBM購入と最先端リソグラフィへのアクセス保証を結びつける容量予約契約を締結し、需要リスクをチップ設計者から装置メーカーにシフトさせています。ファクトリーオートメーションやスマートシティの展開に向けたエッジAIデバイスが16 nm~12 nmの需要を加速し、組み込み不揮発性メモリに合わせた300 mmエッチシステムの新規受注に拍車をかけています。ツールサプライヤーはAIをその場プロセス監視アルゴリズムに導入し、レシピ開発サイクルを短縮し、チャンバーの稼働時間を向上させる。AIワークロードの増加とツールのスマート化という自己強化ループは、2030年以降も半導体機器市場を強化します。

極めて高いCAPEXと長い投資回収サイクル

先進ロジック工場1カ所のコストは今や200億米ドルをはるかに超えており、最先端ツールの顧客基盤はますます集中しています。減価償却期間が長いため、調達の精査は長期化し、ツールメーカーは発注前にマルチノード拡張性を実証する必要に迫られます。ベンダーは、アップグレード対応プラットフォーム、モジュール式真空ジオメトリー、工具の寿命にわたってコストを分散させるサブスクリプションベースのプロセス制御ソフトウェアで対応しています。一部のIDMは、能力拡張を延期することで、設置を延期し、収益認識をプロジェクトの後期にシフトさせています。とはいえ、ワットあたりの性能に対する絶え間ないニーズがロードマップを維持し、半導体機器市場への全体的な足かせを抑えています。

セグメント分析

2024年の半導体機器市場シェアの83.7%はウエハー前工程装置が占め、歩留まり向上におけるリソグラフィ、エッチング、成膜の中心的役割が浮き彫りになりました。このセグメントでは、High-NA EUVスキャナーが2030年まで21.1%のCAGRを記録しました。これは、2nmロジックと3D DRAM構造のパターニングに不可欠であるためで、台湾とニューヨークのファブからのマルチシステム受注はすでに数十億米ドルに達しています。

バックエンドの複雑さは、2µm以下のアライメント精度を持つ熱圧着ボンダーや、フロントエンドのリソグラフィ精度を活用したファンアウト・ウェハーレベル・パッケージングなどの技術革新を後押ししています。リソグラフィ光学系、配置ロボット、高周波テストモジュールを統合プラットフォームに組み込んだベンダーは、先進パッケージング予算のシェアを拡大し、リソグラフィグレードの投資をサプライチェーンのさらに下まで拡大しています。

ファブレスチップ企業がTSMC、Samsung Foundry、GlobalFoundriesに注文を集中させているため、2024年の半導体機器市場収益の52.2%を鋳造が占めています。アリゾナ、ドレスデン、高雄の各メガプロジェクトは、EUVスキャナー、マルチチャンバーエッチングスタック、原子層蒸着装置のクラスターを備え、迅速なレシピ交換が可能なように構成されています。厳格なアップタイムコミットメントにより、バンドルサービス契約が推進され、現在ではツール取得額の25~30%に相当し、装置サプライヤーに年金の流れを作り出しています。

OSATハウスは、CAGR12.2%で最も急成長している顧客カテゴリーに浮上し、AIアクセラレータや自動車用ドメインコントローラに必要な2.5次元および3次元パッケージアーキテクチャに後押しされています。新たな設備投資ラインには、シリコン貫通ビア用レーザードリル、高密度フリップチップボンダー、モールド・アンダーフィル・ディスペンスシステムなどがあります。統合デバイスメーカー(IDM)は、最先端のロジックを外注する一方で、パワー、アナログ、センサーラインに選択的に投資するファブライト戦略を追求しているため、かなりの規模を維持しているが、シェアは低下しています。

半導体機器市場は、装置タイプ(フロントエンド装置、バックエンド装置)、サプライチェーン参入企業(IDM、鋳造、OSAT)、ウエハーサイズ(300mm、200mm、<=150 Mm), Fab Technology Node(>=28Nm、16/14Nm、その他)、エンドユーザー産業(コンピューティングとデータセンター、通信(5G、RF)、その他)、地域(北米、南米、欧州、アジア太平洋、中東アフリカ)で区分されます。

地域分析

アジア太平洋は2024年に72.2%の半導体機器市場シェアを維持し、台湾、韓国、中国本土の緻密なエコシステムがその原動力となりました。台湾の鋳造クラスターだけでも稼働率が90%を超え、EUVと計測の受注を維持した。韓国は1ベータDRAMとゲートオールラウンド・ロジックへの支出を強化し、中国は輸出規制の圧力下でも自立を推進することで国内のエッチャーと成膜設備の稼働を高めました。

北米のルネッサンスはCHIPS法の助成金によるもので、アルバニー・ナノテックは世界初のHigh-NA EUV装置を納入し、国内リソグラフィ・エコシステムの礎を築いた。TSMCとインテルによるアリゾナ州での同時投資は、オレゴン州での装置組立からテキサス州での材料供給へと伸びる回廊を形成し、地域需要のバランスを取り戻しました。

欧州は、自動車用パワーデバイス、RFフロントエンド、先端センサーといった特殊技術に焦点を絞り、欧州チップ法を利用して2030年までに地域の生産能力を倍増させることを目標としています。ザクセン州の300mmデュアルラインはすでにロジック、アナログ、パワープロセッシングを兼ね備えています。

中東とアフリカは、CAGR 9.9%と最も速い成長を記録しました。これは、サウジアラビアの90億米ドルのファブ計画とUAEのフィージビリティ・スタディに後押しされたもので、トレーニング、改修、ロジスティクスにまたがるターンキーツールサポート契約を必要とします。南米は依然としてニッチです。ブラジルは、成熟したノード200mmツールに依存する自動車用および産業用チップに選択的に投資しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 先端家電とスマートフォンの需要急増

- AI、IoT、エッジデバイスノードへの急速な投資

- 政府補助金の波(CHIPS、EUチップス法、その他)がツールのCAPEXを押し上げる

- 新しいツールセットを必要とするGAAと高NA EUVへの移行

- グリーン・ファブ」改修ツールを推進する持続可能性の義務化

- 3D異種集積パッケージ需要急増

- 市場抑制要因

- 極めて高いCAPEXと長い投資回収サイクル

- 工具出荷を遅らせる特殊材料供給のボトルネック

- 中国向け工具の輸出規制

- 熟練したフィールドサービス・エンジニアの深刻な不足

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因の影響

第5章 市場規模と成長予測

- 機器別

- フロントエンド機器

- リソグラフィ装置

- エッチング装置

- 蒸着装置

- 計測/検査装置

- 洗浄装置

- フォトレジスト加工装置

- その他のフロントエンドタイプ

- バックエンド機器

- 試験装置

- 組立・包装機器

- フロントエンド機器

- サプライチェーン参入企業別

- IDM

- ファウンドリ

- OSAT

- ウエハーサイズ別

- 300 mm

- 200 mm

- <=150 mm

- ファブ技術ノード別

- >=28nm

- 16/14 nm

- 10/7 nm

- 5 nm以下

- エンドユーザー業界別

- コンピューティングとデータセンター

- 通信(5G、RF)

- 自動車およびモビリティ

- コンシューマーエレクトロニクス

- 産業用およびその他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Applied Materials Inc.

- ASML Holding NV

- Tokyo Electron Ltd.

- Lam Research Corp.

- KLA Corp.

- Screen Holdings Co. Ltd.

- Teradyne Inc.

- Hitachi High-Tech Corp.

- Veeco Instruments Inc.

- ASM International NV

- Canon Inc.

- Nikon Corp.

- Onto Innovation Inc.

- Nova Ltd.

- Advantest Corp.

- Hanmi Semiconductor Co. Ltd.

- Disco Corp.

- BESI(BE Semiconductor Industries)

- Kulicke & Soffa Industries Inc.

- FormFactor Inc.

- Plasma-Therm LLC

- SUSS MicroTec SE

- Kokusai Electric Corp.

- AMEC(Advanced Micro-Fabrication Equipment Inc.)

- Naura Technology Group Co. Ltd.