|

市場調査レポート

商品コード

1851013

自律走行トラクター:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Autonomous Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自律走行トラクター:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月29日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

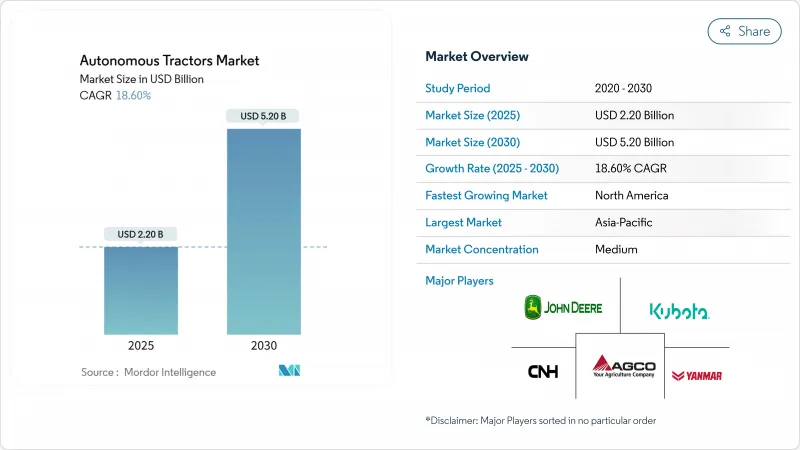

自律走行トラクター市場は2025年に22億米ドルに達し、CAGR18.6%を維持しながら2030年には52億米ドルに達すると予測されます。

この上昇の主な要因は、深刻な農業労働危機、精密農業の急速な普及、および接続された低炭素機械の投資回収期間を短縮する政府インセンティブの拡大にあります。大規模な商業栽培農家は、すでに20%の省力化を利益率の向上に結びつけており、24時間連続の圃場作業によって季節ごとの生産高を高めています。ソフトウェア中心の収益モデル、後付けキット、電動パワートレインは、対応可能な需要をさらに拡大し、自律走行トラクター市場がニッチな採用を超越した主流の成長段階に入りつつあることを示しています。

世界の自律走行トラクター市場の動向と洞察

農業労働者不足と賃金インフレの高まり

農村部の労働力減少が農家の平均年齢上昇と衝突し、空いた農業の役割の半分が満たされないままになっています。賃金インフレは、圃場のピーク時の負担を増大させる。特に収穫期には、自律走行式の穀物運搬車がオペレーターなしで24時間稼働するようになります。生産者は、重要な作業時間帯に30~40%の生産性向上を報告しており、自律走行トラクター市場が、裁量的な利便性を付加するのではなく、構造的なギャップを埋めていることを裏付けています。この緊急性は、自律性を長期的な農場存続に必要な中核インフラとして再定義しました。

精密農業とIoT接続の採用加速

クラウド農場管理プラットフォームは、すでに100万台以上の機械をリンクし、トラクターを、土壌、収穫量、資産情報をリアルタイムの意思決定システムに供給するローミング・データ・ハブに変えています。高度なセンサー・フュージョン、GPS、マシン・ビジョン、レーダーにより、センチメートル・レベルのガイダンス、可変レート入力配置、フルフィールド障害物回避が可能になります。

小規模農家には高い初期費用と不確実なROI

電動自律走行トラクター1台は8万8,000米ドルを超えることがあり、100ヘクタール未満の農場にとっては高額な出費となります。接続性のアップグレード、オンプレミスのデータ・インフラ、サービス加入がさらに負担を増やします。モデルによると、外部からの補助金で資本費用を相殺しない限り、採算の取れる展開は500ヘクタール以上で始まることが多く、多くの家族経営の農場は価格が下がるまで共同所有かレンタルサービスに頼ることになります。

セグメント分析

現在の需要の中心は31-100馬力以上のトラクターで、2024年の自律走行トラクター市場シェアの39.5%を占める。31~100馬力の中位レンジは、適度な耕作に十分な馬力と管理しやすい資本要件が調和した、極めて重要な橋渡し役となっています。モジュラー・アドオン、ビジョン・キット、テレマティックス、自動化の実施により、自律性の段階的なアップグレードが可能になります。販売店の報告によれば、生産者は、より大型の200馬力のフラッグシップ機を購入する前に、既存の75馬力のトラクターで半自律型レトロフィットを試しており、段階的な採用曲線を示しています。

しかし、スポットライトは、CAGR24.0%で最も急成長している100馬力以上に移りつつあります。これらの機械は、広大な農地での耕うん、播種、大規模農家での重耕運機などに適しています。30馬力までのコンパクトなユニットは、園芸、酪農、混作農家で、草刈りや散布などの反復作業を自動化するのに役立っています。1台の重いトラクターの代わりに複数の軽量ロボットを配備するフリート・コンセプトは、土壌の圧縮を低減し、圃場への参入障壁を減らし、小規模農家の精密技術を民主化します。

オペレーターが運転席に残るか、遠隔操作で機械を監視する半自律型構成は、2024年の市場シェア68.2%を占める。農家は即座の省力化を重視しながらも、手動によるフォールバックを保持しています。予測期間中、完全自律型ソリューションは他を凌駕し、CAGR 23.1%で拡大します。遠隔操舵補助、タスク別自律性、そして完全なフリート・オーケストレーションという段階的な経路は、自動車セクターの進化を反映しています。リアルタイム・キネマティックGPS、マルチカメラ認識、冗長安全層が、現在商業分野に入ってきているレベル4の機能を支えています。

生産者は、コンバインが介入なしに12時間連続で自律走行するのを示し、自信を深めています。規制当局は、技術を規定するのではなく、性能に基づくガイドラインを作成し、導入を容易にしています。保険会社は、事故リスクを低減する有効な自律走行システムに対して保険料の割引を提供し始めています。

地域別分析

アジア太平洋地域の2024年のシェアは46.3%に達し、首位を維持。農業の近代化に対する中国の数兆ドル規模の誓約は、設備補助金、AI研究ハブ、農村部での5G展開に資本を注入するものです。日本では、急速に高齢化が進む農家人口に対抗してスマート農業が推進され、オーストラリアでは、広大な乾燥地での農業経営に適した自律型ソリューションに助成金が向けられています。これらの一致した政策が、この地域全体の自律走行トラクター市場に深い機会プールを維持しています。

北米はCAGR 23.2%で最も急成長している地域です。高い人件費、豊富なベンチャー資本、活発なOEM研究開発パイプラインが商業化を加速します。米国は精密農業の接続プロジェクトで優位を占めているが、まだ27%の農場しか採用しておらず、大きな余地を残しています。農場ごとの最低ブロードバンド速度を義務付ける連邦プログラムは、自律に必要なデジタル基盤を加速させる。カナダはクリーンテクノロジー補助金を活用し、メキシコは機械化を推進することで自動化を南下させる。

欧州は、デジタル農業、低炭素農業に報いる共通農業政策改革に支えられ、着実な成長路線をたどっています。ドイツ、フランス、スペインは、定評ある機械メーカーと、電気駆動に有利な厳しい排出基準によって、導入をリードしています。東欧は、広大な連続農地がフリート規模の自律性に適しているため、上昇余地があります。補助金付きの炭素クレジット制度とエネルギー転換基金が財政的ハードルを下げ、自律走行トラクター市場の重要なセグメントとして欧州を確固たるものにしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 農業労働力不足と賃金インフレの深刻化

- 精密農業とIoT接続の導入加速

- スマート機器および低炭素機器に対する政府のインセンティブ

- 果樹園とブドウ園は狭小畝栽培に移行している自律走行トラクター

- レトロフィットの自律性を可能にするOEMオープンAPIエコシステム

- 電気自動車の自動運転ユニットの炭素クレジット収益化

- 市場抑制要因

- 小規模農場では初期費用が高く、ROIも不透明

- コネクテッドフリートにおけるデータプライバシーとサイバーセキュリティの懸念

- 地方における5G/エッジ接続の不安定さ

- 無人運転機械に対する責任規制の進化

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 馬力別

- 30HP未満

- 31~100HP

- 100HP以上

- オートメーションレベル別

- 半自律

- 完全自律

- ドライブタイプ別

- ディーゼル

- ハイブリッド

- バッテリー電気

- 用途別

- 耕作

- 播種

- 収穫

- 果樹園とブドウ園の運営

- コンポーネント別

- GPS/GNSS

- センサーとビジョンシステム

- LiDARおよびレーダーモジュール

- 制御およびナビゲーションソフトウェア

- 農場規模別

- 小規模(100ヘクタール未満)

- 中規模(100~500ヘクタール)

- 大規模(500ヘクタール以上)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Deere & Company

- AGCO Corporation(Fendt, Massey Ferguson)

- CNH Industrial(Case IH, New Holland)

- Kubota Corporation

- Mahindra & Mahindra

- Monarch Tractor

- AutoNext Automation

- YANMAR HOLDINGS CO., LTD.

- CLAAS KGaA mbH

- TYM Corporation

- SDF Group

- Kioti(daedong)

- ISEKI & Co., Ltd