|

市場調査レポート

商品コード

1687800

中国のホームテキスタイル市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China Home Textiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のホームテキスタイル市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

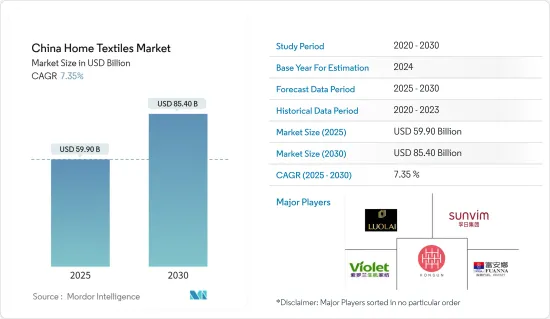

中国のホームテキスタイル市場規模は2025年に599億米ドルと推定・予測され、2030年には854億米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは7.35%です。

中国の膨大な人口と、年々増加する一人当たりの繊維・衣料品消費は、同市場に有利な世界的ビジネスチャンスをもたらしています。また、同国における住宅リフォーム・プロジェクトの増加も、ホームテキスタイル生産者にチャンスをもたらし、市場の成長を加速させています。中国の顧客は、家庭装飾品の品質とデザインをますます重視するようになっています。そのため、同市場は調査期間中に急成長を遂げており、予測期間中も成長が続くと予想されます。

広東省、上海、江蘇省南通、浙江省、山東省は中国の産業集積地です。いくつかの主要企業は、スマートホーム産業を開拓するためにテクノロジー企業と提携しています。市場の約45%を占めるアジア太平洋地域は、依然としてホームテキスタイルの最も強力な生産地であり消費地です。さらに、同地域では中国がホームテキスタイルの最大の製造・消費国です。

COVID-19の発生は中国の家庭用繊維産業を混乱させ、操業停止と広範囲での生産縮小状態に陥いりました。しかし、国がパンデミックを徐々に効果的にコントロールすることで、業界は多くの困難を克服し、2020年下半期に作業と生産を再開することを積極的に組織しました。

中国のホームテキスタイル市場の動向

輸出の増加が市場の収益増に貢献

米国をはじめとするいくつかの市場における製品の高い需要に起因する輸出量の増加は、調査期間中に中国のホームテキスタイル市場がより多くの収益を記録するのに役立っています。しかし、パンデミックの影響で、2020年の輸出総額は減収を記録し、中国家庭用繊維産業の輸出部門に深刻な課題をもたらしています。税関統計によると、2020年の中国の繊維製品輸出総額は372億米ドルで、前年比6.43%減少しました。北米とオセアニアへの輸出はそれぞれ2.11%と8.35%の成長率を記録したが、アジアと南米への輸出は2020年中にそれぞれ-10.70%と-12.93%と大幅に減少しました。

ベッドリネンとベッドスプレッドセグメントの成長

ベッドリネンおよびベッドスプレッド部門は、市場における製品需要の拡大により、より多くの収益を記録しています。公式統計によると、調査対象市場において、960社以上の寝具企業が2020年中に970億2,200万人民元の営業利益を達成し、年間利益が増加しました。同様に、寝具の輸出額は128億米ドルで、前年比2.44%減少し、タオルと毛布の輸出額は米国と中国の貿易の緊張とCOVID-19の流行により、それぞれ-13.77%、-12.44%と大幅に減少しました。しかし、カーペットとキッチンテキスタイルは2020年の下落動向に反して上昇しました。市場は2021年前半に回復の兆しを見せ、パンデミックの影響から状況が正常になり始めたため、予測期間の残りも続くと予想されます。

中国のホームテキスタイル産業の概要

本レポートでは、中国のホームテキスタイル市場で事業を展開している主要な国際的企業を取り上げています。市場シェアでは、現在市場を独占している大手企業は少数です。しかし、需要は主に消費者の所得によってもたらされています。Luolai Home Textile、Sunvim Group、Fu Anna、Hunan Mendale Hometextile Company Ltd.などの大手・主要企業は、大量仕入れ、幅広い製品、効果的なマーチャンダイジングとマーケティングで競争しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の洞察と力学

- 市場概要

- 市場促進要因

- 市場抑制要因/課題

- 市場機会

- 業界サプライチェーン/バリューチェーン分析

- ポーターのファイブフォース分析

- 消費者の購買行動と購買動向に関する洞察

- 業界の主要動向と技術革新に関する洞察

- 中国のホームテキスタイル市場の輸出入に関する洞察

- COVID-19が市場に与える影響

- 生地の種類(綿、絹、ポリエステルなど)に関する洞察

第5章 市場セグメンテーション

- 製品別

- ベッドリネン

- バスリネン

- キッチンリネン

- 椅子張り

- フロアカバー

- 流通チャネル別

- スーパーマーケット&ハイパーマーケット

- 専門店

- オンライン

- その他の流通チャネル

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Luolai Home Textile Co., Ltd.

- Hebei Ruichun Textile Co., Ltd.

- Sunvim Group

- Fu Anna

- Orient International Holding Shanghai Hometex Co., Ltd.

- Honsun Home Textile Co., Ltd.

- Hunan Mendale Hometextile Company Ltd.

- Beyond Home Textile

- Jiangsu Bermo Home Textile Technology Co.,Ltd.

- Violet Home Textile Co., Ltd.

- Shanghai Shuixing Home Textile Co., Ltd.

- その他の企業

第7章 市場の将来

第8章 免責事項

The China Home Textiles Market size is estimated at USD 59.90 billion in 2025, and is expected to reach USD 85.40 billion by 2030, at a CAGR of 7.35% during the forecast period (2025-2030).

China's huge population, coupled with its increasing textile and clothing consumption per capita year by year, is providing a lucrative global business opportunity for the market. The increasing home renovation projects in the country are also accelerating the growth of the market by creating opportunities for home textiles producers. Chinese customers are increasingly placing more emphasis on the quality and design of home decorations. Thus, the market has been experiencing rapid growth during the study period and is anticipated to continue the growth in the forecast period as well.

Guangdong Province, Shanghai, Nantong in Jiangsu Province, Zhejiang Province, and Shandong Province are the industrial cluster areas in China. Several key players are pairing up with technology companies to tap the smart home industry. Asia-Pacific region, which accounts for around 45% of the market remains as the most strong producer and consumer of home textiles. Moreover, within the region, China is the largest manufacturer and consumer of home textiles.

The COVID-19 outbreak disrupted the China home textile industry which operations fell into a state of shutdown and production reduction in a large area. However, with the country's gradual and effective control of the pandemic, the industry has overcome many difficulties and actively organized the resumption of work and production during the second half of the year 2020.

China Home Textile Market Trends

High Exports Has Helped the Market to Record More Revenues

The increasing export quantities owing to the high demand for the products in the US and several other markets have helped the China home textile market to record more revenues during the study period. However, due to the pandemic, the total export value recorded a drop in revenue during 2020 and has brought severe challenges to the export segment of the China home textile industry. According to customs statistics, in 2020, China's textile product exports totaled USD 37.2 billion, a year-on-year decrease of 6.43%. Exports to North America and Oceania recorded growth rates of 2.11% and 8.35% respectively, whereas exports to Asia and South America fell sharply, -10.70% and -12.93% respectively during 2020.

Growing Bed Linen and Bed Spread Segment

Bed linen and bedspread segments have been recording more revenues owing to the growing demand for the products in the market. According to the official statistics, in the market studied, more than 960 bedding enterprises have achieved operating income of CNY 97.022 billion during 2020 which resulted in increased profits for the year. Similarly, the export value of bedding valued at USD 12.8 billion, down 2.44% year-on-year, and the export value of towels and blankets dropped significantly, -13.77% and -12.44% respectively. owing to the COVID-19 pandemic and tension between the US and China trade. However, the carpets and kitchen textiles segments rose against the downtrend in 2020. The market showed signs of recovery in the first half of 2021, which is anticipated to continue for the rest of the forecast period as the situation started to get to normal from the pandemic effect.

China Home Textile Industry Overview

The report covers major international players operating in the Chinese home textile market. In terms of market share, few of the major players currently dominate the market. However, the demand is predominantly driven by consumer income. The large and key players including Luolai Home Textile Co., Ltd., Sunvim Group, Fu Anna, Hunan Mendale Hometextile Company Ltd., etc., competing through volume purchasing, breadth of products, and effective merchandising and marketing, whereas small and medium-sized players, are focusing on a market-specific segment and compete through depth of products and superior customer service.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints/Challenges

- 4.4 Market Opportunities

- 4.5 Industry Supply Chain/Value Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.7 Insights on Consumer Buying Behavior and Purchasing Trends

- 4.8 Insights on Key Trends and Technological Innovations in the Industry

- 4.9 Insights on Imports and Exports in China Home Textiles Market

- 4.10 Impact of COVID -19 on the Market

- 4.11 Insights on Fabric Type (Cotton, Silk, Polyester, etc)

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Bed Linen

- 5.1.2 Bath Linen

- 5.1.3 Kitchen Linen

- 5.1.4 Upholstery

- 5.1.5 Floor Covering

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets & Hypermarkets

- 5.2.2 Speciality Stores

- 5.2.3 Online

- 5.2.4 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Luolai Home Textile Co., Ltd.

- 6.2.2 Hebei Ruichun Textile Co., Ltd.

- 6.2.3 Sunvim Group

- 6.2.4 Fu Anna

- 6.2.5 Orient International Holding Shanghai Hometex Co., Ltd.

- 6.2.6 Honsun Home Textile Co., Ltd.

- 6.2.7 Hunan Mendale Hometextile Company Ltd.

- 6.2.8 Beyond Home Textile

- 6.2.9 Jiangsu Bermo Home Textile Technology Co.,Ltd.

- 6.2.10 Violet Home Textile Co., Ltd.

- 6.2.11 Shanghai Shuixing Home Textile Co., Ltd.

- 6.2.12 Other Companies*