|

市場調査レポート

商品コード

1687703

GDPRサービス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)GDPR Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| GDPRサービス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

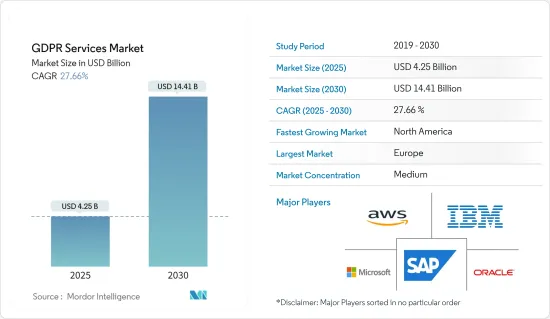

GDPRサービス市場規模は2025年に42億5,000万米ドルと推計され、予測期間(2025年~2030年)のCAGRは27.66%で、2030年には144億1,000万米ドルに達すると予測されます。

接続が増え、デジタル化が進んだ結果、企業は指数関数的な量のデータを生み出しています。場所やウェブサイトを訪れたり、あるいは電話をかけたりした人々は、データとしてデジタルの足跡を残し、企業が顧客と関わり、より良いユーザー体験を提供するために活用できる貴重な資源となります。組織運営や品質モニタリングにおいて、プライバシー、セキュリティ、真正性、合法性、信頼性、普遍性、拡張性といった特性に対する要求が高まっているため、GDPRサービス業界は発展の余地が大きいです。

主なハイライト

- アルゼンチンの情報公開庁は、個人データ保護法の改正に向けた協議プロセスを開始しました。この改革は、EU一般データ保護規則の規則に大きく基づいています。同様に、9月にはオーストラリア第2位の通信会社オプタスが重大なデータ漏洩に見舞われ、国会議員によるプライバシー法改正法案が昨年可決されました。

- 企業ユーザーを標的にしたソーシャルエンジニアリングによるサイバー攻撃は著しく増加しています。現在までにインターネット上で発見された、著しく広まったキャンペーンの中には、世界保健機関(WHO)や米国疾病管理センター(CDC)を装った詐欺メールがあります。CDCの公式ウェブアドレスに似たドメイン名で、パスワードを盗むことを目的とし、偽ワクチンに資金を提供するためにビットコインの「寄付」まで要求します。このような事例は、市場調査の需要を高めています。

- さらに、ここ数年、コネクテッド・デバイスが増加しています。シスコシステムズによると、M2M接続は昨年中に21億ユニットに達すると予想されています。クラウド・サービスは、データ転送の技術的進歩に伴い、より身近なものとなりつつあります。パブリック・クラウドが台頭してきたのです。この技術的進歩により、フィッシングメール、ボット、ランサムウェアの転送が高速化し、それらがもたらす脆弱性が指摘されています。

- パンデミックに対応するためにサイバーセキュリティ予算の変更が増加し、GDPRサービスの引き金となっています。Microsoft Corporationがパンデミック発生時に800人のビジネスリーダーを対象に行った調査によると、回答者の36%がサイバーセキュリティ予算を1~25%増加させることを提案し、約22%がパンデミック対策のために予算を25%以上増加させたと回答しています。パンデミックは、GDPRが個人の権利と社会の間で取るバランスに鋭い焦点をもたらしました。世界の当局は、データ保護とプライバシーに対処するためのガイドラインを変更しつつあります。

- その反面、欧州連合一般データ保護規則(GDPR)は、消去権、修正権、ポータビリティなどの新たな要件をクラウドサービスプロバイダーや顧客に突きつけており、技術的な観点だけでなく、実装や実施も難しい課題となっています。また、クラウドのサプライチェーン全体における個人データ保護に関する責任分担のモデルも新たな側面として登場します。一言で言えば、クラウドの顧客はGDPRの要件を満たさなければならないため、データ主体に対してある程度の説明責任を負うことになります。

一般データ保護規則(GDPR)サービス市場の動向

データ漏えいに伴うデータセキュリティとプライバシーの必要性

- SurfSharkによると、昨年第3四半期にデータ漏洩により全世界で約1,500万件のデータレコードが流出しました。前四半期と比較すると、この件数は37%増加しています。データ漏えいの件数を減らし、機密情報を保護するためのデータガバナンス、データマッピング、データ管理サービスの必要性が高まっているのは、規制に違反した場合に課される多額の罰金のせいでもあります。このようなデータ侵害の増加は、GDPRサービス市場を牽引すると思われます。

- データ漏洩は急激なコスト増と貴重な顧客情報の損失につながります。Identity Theft Resource Centerによると、米国の銀行・金融セクターにおけるデータ漏洩の被害者数は、2021年第3四半期には1億6,000万人に上り、2021年第1四半期と第2四半期を合わせた数字(1億2,100万人)から増加しています。サイバー攻撃者は、複数の金融サービス組織を標的に金銭的利益を得る攻撃を仕掛けるために、可能な限り最も分かりやすい道を追求しています。

- ここ数年、ヘルスケア分野はサイバー犯罪者の間で大きな関心を集める標的となっています。その貴重なデータの生成により、ヘルスケアは最近、サイバー攻撃に対して脆弱になっています。HIPAA Journalの報告書によると、ヘルスケア機関では2021年に500件以上のデータ漏洩が56件発生しています。さらに、同レポートによれば、暴露された、あるいは不許可で開示されたレコードの数は約24.5%増加し、データ漏洩により2021年12月時点で295万件のレコードが暴露された、あるいは不許可で開示されました。

- 法律事務所DLA Piperの報告書によると、GDPRの罰金は40%近く上昇し、GDPRの罰金総額は1億9,150万米ドルに上りました。また、データ保護当局は121,165件の情報漏えいの届け出を記録した(前年同期比19%増)。デジタル・トランスフォーメーションへの支出は、パンデミックの間に増加し、それがプライバシーの必要性を推進しました。世界中の企業向けにエンタープライズ・ソフトウェアを開発するインダストリアル・アンド・フィナンシャル・システムズ(IFS)が実施した調査によると、70%の企業がパンデミック中にデジタルトランスフォーメーションへの支出を増加または維持しています。

- エネルギーや石油など規制の厳しい業界では、データ漏えいのコストが高くなります。Leidosのデータによると、エネルギー部門の1レコードあたり237米ドルは、平均201米ドルを大幅に上回っています。石油・ガスの流通と生産における量、速度、位置、その他の重要な活動を監視する運用技術(OT)システムは、機密情報や専有情報を豊富に生み出すだけでなく、企業、施設、従業員の経済的健全性と物理的安全性にとっても不可欠です。

欧州が市場の主要シェアを占める見込み

- 欧州はGDPRの受け入れが進んでいるため、GDPRサービスが大きなシェアを占めると予想されています。同地域はデータ駆動型地域としての開発に努めており、GDPRの高い受容性により、組織全体でGDPRサービスの大幅な導入が見られます。この規制は、これらの国の企業にGDPRの遵守を義務付けています。

- EUの新しい個人情報保護法が施行されて以来、欧州の個人情報保護当局は約6万5,000件のデータ漏えいの届け出を受けています。また、欧州11カ国の規制当局はGDPRに対して6,300万米ドルの制裁金を課しました。リンクレーターズによると、データ保護当局へのデータ侵害の届出は大幅に増加しており、EU GDPRの初年度と比較して平均66%増加しています。

- 人工知能やその他の新たなテクノロジーを活用するためにデータの収集と共有を加速させる中で、政府、企業、その他の組織は、共通の目標に取り組みながらデータ所有者の権利を保護するための健全なデータ管理ツールを模索し、導入する必要性に直面しています。そのため政府は、さまざまなデータエコシステム関係者間で倫理的かつ公正なデータ共有を促進するための新たな手段を模索しています。

- この地域では、IoTに接続された自動車に対する需要が高まっています。これは、個人を追跡できる個人データで構成されます。さらに、家庭のエネルギー消費パターンに関する個人データを活用するスマートメーターもあります。この地域ではGDPRが施行され、コネクテッド・ソリューションを展開する様々なエンドユーザーを持つ企業にとって、ユーザーのデータを保護することが必要となっています。これにより、GDPRサービスの需要が高まると予想されます。

- 昨年2月、グーグル・アナリティクスは、オーストリアでの同様の判決に続き、フランスでも欧州連合の個人情報保護法に違反していると認定されました。フランスのデータ保護監視機関であるCNILは、無名の地元ウェブサイトによるグーグル・アナリティクスの使用がEUの一般データ保護規則(GDPR)、特に、本質的に同等のプライバシー保護を持たないいわゆる第三国へのEU域外への個人データ移転をカバーする第44条に違反していると述べた。

一般データ保護規則(GDPR)サービス業界の概要

GDPRサービス市場は、 IBM, Microsoft, AWSなどの主要企業により、適度に統合されています。このようなプレーヤーの市場浸透度は高いです。市場のプレーヤーは、市場での存在感と顧客基盤を拡大するために、戦略的ソリューションを提供する革新を進めています。これにより、新規契約の獲得や新市場の開拓が可能になります。市場の主な発展をいくつか紹介する:

- 2022年9月:アンリツA/Sは、世界なデータ保護とGDPRコンプライアンスを顧客に提供するため、SecuPiとの最新の協業を発表しました。この新しい提携から最初に恩恵を受けるのは、世界的に最も厳しいデータ保護要件を持つTier-1通信事業者です。アンリツはSecuPiと提携し、市場をリードする効率性と柔軟性でセキュリティとコンプライアンスの要件を満たします。この協業により、事業者はコスト削減、設置の容易さ、アンリツのサービス・アシュアランス技術との統合を実現できます。

- 2022年4月:企業のITスタック全体にプライバシーを簡単にエンコードするワンストップ・プライバシープラットフォームのトランセンドは、プライバシープログラムへの実用的な追加機能としてデータマッピングを発表しました。トランセンドのData Mappingは、自動化されたスキャン、データサイロの発見、高度なコンテンツの分類を通して、現代ビジネスにおける統一されたデータ管理を可能にします。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- GDPRサービス市場におけるCOVID-19の影響

第5章 市場力学

- 市場促進要因

- 市場抑制要因

第6章 市場セグメンテーション

- 導入タイプ別

- オンプレミス

- クラウド

- 提供別

- データ管理

- データ・ディスカバリーとマッピング

- データガバナンス

- API管理

- 組織規模別

- 大企業

- 中小企業

- エンドユーザー別

- 銀行、金融サービス、保険(BFSI)

- 通信・IT

- 小売・消費財

- ヘルスケア・ライフサイエンス

- 製造業

- その他エンドユーザー産業

- 地域

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- IBM Corporation

- Veritas Technologies LLC

- Amazon Web Services Inc.

- Microsoft Corporation

- Micro Focus International PLC

- Oracle Corporation

- SAP SE

- Capgemini SE

- SecureWorks Inc.

- Wipro Limited

- DXC Technology Company

- Accenture PLC

- Atos SE

- Tata Consultancy Services Limited

- Larsen & Toubro Infotech Limited

- Infosys Limited

第8章 投資分析

第9章 市場の将来

The GDPR Services Market size is estimated at USD 4.25 billion in 2025, and is expected to reach USD 14.41 billion by 2030, at a CAGR of 27.66% during the forecast period (2025-2030).

As a result of increased connection and ongoing digitization, businesses are producing an exponential amount of data. People who visit places and websites or even make phone calls leave a digital footprint as data, a valuable resource businesses can utilize to engage with customers and provide a better user experience. Because of the increased demand for characteristics such as privacy, security, authenticity, legality, trust, universality, and scalability in organizational operations and quality monitoring, the GDPR services industry has a lot of room to develop.

Key Highlights

- Argentina's Access to Public Information Agency has begun the consultation process to update its Personal Data Protection Law. The reforms are heavily based on the rules of the EU General Data Protection Regulation. Similarly, in September, Australia's second-largest telecommunications firm, Optus, had a significant data breach, prompting MPs to pass the Privacy Legislation Amendment Bill of the last year, which boosts fines to AUD 50 million when companies suffer repeated data breaches.

- Socially engineered cyber attacks targeting enterprise users are growing significantly. Among some of the significantly widespread campaigns spotted on the internet to date have been fraudulent emails indicated to be coming from the World Health Organization (WHO) and the US Center for Disease Control (CDC). The building domain names that look similar to the CDC's official web address aim at stealing passwords and even request bitcoin "donations" to fund a fake vaccine. Such instances have been increasing the demand for market studies.

- Further, there has been a rise in connected devices over the last few years. According to Cisco Systems, M2M connections are expected to reach 2.1 billion units in the last year. Cloud services are becoming more familiar with technological advancements in data transfers. The public cloud has been emerging. This technological advancement has resulted in the faster transfer of phishing emails, bots, and ransomware, indicating the vulnerabilities that they bring in.

- There has been a rise in the cybersecurity budget changes in response to the pandemic, triggering GDPR services. According to a survey by Microsoft Corporation of 800 business leaders during a pandemic, 36% of the respondents suggested an increase in the cybersecurity budget by 1-25%, and about 22% said that the budget increased by over 25% to combat the pandemic. The pandemic has brought a sharp focus to the balance that GDPR strikes between the rights of individuals and society. The global authorities are changing their guidelines to deal with data protection and privacy.

- On the flip side, the European Union General Data Protection Regulation (GDPR) confronts cloud service providers and customers with new requirements, such as the right to erasure, rectification, and portability, which is challenging to implement and implement not only from a technical perspective. Another new aspect appears with the model for shared responsibility regarding protecting personal data along the whole cloud supply chain. In a nutshell, the cloud customer remains accountable towards the data subject to an extent as they must fulfill the GDPR requirements.

General Data Protection Regulation (GDPR) Services Market Trends

Need for data security and privacy in the wake of a data breach

- According to SurfShark, Approximately 15 million data records were exposed globally due to data breaches in the third quarter of last year. Compared to the previous quarter, this amount had climbed by 37%. The rise in the need for data governance, data mapping, and data management services to mitigate the number of breaches and protect sensitive information has also been due to the significant fines levied for non-compliance with the regulation. Such a rise in data breaches would drive the GDPR service market.

- Data breaches lead to an exponential cost increase and loss of valuable customer information. According to Identity Theft Resource Center, the number of data breaches in the banking and financial sector of the United States the number of data compromise victims increased to 160 million in Q3 2021, which increased from Q1 and Q2 2021 combined (121 million). Cyber attackers pursue the most straightforward path possible to engineer a financial gain attack targeting several financial services organizations.

- Over the past few years, the healthcare sector has become a target of significant interest among cybercriminals. Due to its generation of valuable data, healthcare has recently become vulnerable to cyber-attacks. Per a HIPAA Journal report, healthcare institutions had 56 data breaches of 500 or more records in 2021. Moreover, the report also stated that the number of records exposed or impermissibly disclosed increased by approximately 24.5%, and data breaches left 2.95 million records exposed or impermissibly disclosed as of December 2021.

- According to a report from a law firm, DLA Piper, the GDPR fines rose by nearly 40%, and penalties under GDPR totaled USD 191.5 million. Also, allied data protection authorities recorded 121,165 breach notifications (19% more than the previous 12-month period). The spending on digital transformation increased during the pandemic, which has propelled a need for privacy. According to a survey conducted by Industrial and Financial Systems (IFS), a developer of enterprise software for companies worldwide, 70% of businesses have increased or maintained digital transformation spending during the pandemic.

- Costs of data breaches in heavily regulated industries, including energy and oil, have higher costs. The energy sector's USD 237 per record is significantly above the USD 201 average, according to Leidos data. The Operational Technology (OT) systems that oversee the volume, velocity, location, and other vital activities in the distribution and production of oil and gas not only produce a wealth of sensitive and proprietary information but are also essential to the economic health and physical safety of the company, its facilities, and its people.

Europe is Expected to Hold Major Share of the Market

- Europe is anticipated to witness a significant share of GDPR services due to the region's high acceptance of the GDPR. The region strives to develop as a data-driven region and exhibit significant adoption of GDPR services across organizations, owing to high acceptance of the GDPR. The regulation mandates the companies in these countries to comply with the GDPR.

- European privacy authorities have received nearly 65,000 data breach notifications since the EU's new privacy law was implemented. Also, regulators in 11 European countries imposed USD 63 million in GDPR fines. According to Linklaters, there has been a significant increase in data breach notifications to data protection authorities, with an average increase of 66% compared to the first year of the EU GDPR.

- In accelerating data collection and sharing to harness artificial intelligence and other emerging technologies, governments, businesses, and other organizations face the increasing need to explore and deploy sound data management tools to protect data owners' rights while addressing common goals. Therefore, governments are exploring new instruments to facilitate ethical and fair data sharing between different data ecosystem actors.

- The region is witnessing an increased demand for IoT-connected cars. This consists of individual data using which a person can be tracked. Then there is smart metering, whereby personal data on household energy consumption patterns is leveraged. With the GDPR being effect in the region, it has become necessary to secure the user's data for the companies with various end-users which deploy connected solutions. This is anticipated to drive the demand for GDPR services.

- In February last year, Google Analytics was found to violate European Union privacy legislation in France, following a similar ruling in Austria. The French data protection watchdog, the CNIL, stated that an unnamed local website's use of Google Analytics violates the EU's General Data Protection Regulation (GDPR) - specifically, Article 44, which covers personal data transfers outside the EU to so-called third countries that do not have essentially equivalent privacy protections.

General Data Protection Regulation (GDPR) Services Industry Overview

The GDPR Services Market is moderately consolidated, with some major players such as IBM, Microsoft, AWS, and others. The level of market penetration is high for such players. The players in the market are innovating in providing strategic solutions to increase their market presence and customer base. This enables them to secure new contracts and tap new markets. Some of the key developments in the market are:

- September 2022: Anritsu A/S has announced its latest collaboration with SecuPi to provide customers with global data protection and GDPR compliance. The first to benefit from this new alliance is a Tier-1 telecoms provider with some of the most demanding data protection requirements of any operator globally. Anritsu has teamed with SecuPi to fulfill security and compliance requirements with market-leading efficiency and flexibility. The collaboration will also provide operators with cost savings, ease of installation, and integration with Anritsu's Service Assurance technologies.

- April 2022: Transcend, the one-stop privacy platform that makes it simple to encode privacy across a company's IT stack has unveiled Data Mapping as an actionable addition to a privacy program. Transcend Data Mapping enables unified data management for modern businesses through automated scanning, data silo discovery, and advanced content classification-all in an easy-to-use and collaborative platform where users can easily assign system owners, delegate tasks, and generate compliance records.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/ Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact Of COVID-19 On the GDPR Services Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.2 Market Restraints

6 MARKET SEGMENTATION

- 6.1 By Type of Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Offering

- 6.2.1 Data Management

- 6.2.2 Data Discovery and Mapping

- 6.2.3 Data Governance

- 6.2.4 API Management

- 6.3 By Organization size

- 6.3.1 Large Enterprises

- 6.3.2 Small and Medium-sized Enterprises

- 6.4 By End User

- 6.4.1 Banking, Financial Services, and Insurance (BFSI)

- 6.4.2 Telecom and IT

- 6.4.3 Retail and Consumer Goods

- 6.4.4 Healthcare and Life Sciences

- 6.4.5 Manufacturing

- 6.4.6 Other End-user Industries

- 6.5 Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Veritas Technologies LLC

- 7.1.3 Amazon Web Services Inc.

- 7.1.4 Microsoft Corporation

- 7.1.5 Micro Focus International PLC

- 7.1.6 Oracle Corporation

- 7.1.7 SAP SE

- 7.1.8 Capgemini SE

- 7.1.9 SecureWorks Inc.

- 7.1.10 Wipro Limited

- 7.1.11 DXC Technology Company

- 7.1.12 Accenture PLC

- 7.1.13 Atos SE

- 7.1.14 Tata Consultancy Services Limited

- 7.1.15 Larsen & Toubro Infotech Limited

- 7.1.16 Infosys Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET