|

|

市場調査レポート

商品コード

1687463

電気自動車用パワーインバータ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Electric Vehicle Power Inverter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電気自動車用パワーインバータ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 159 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

電気自動車用パワーインバータの市場規模は、2025年に93億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは22.66%で、2030年には260億5,000万米ドルに達すると予測されます。

各国の政府は、電動モビリティプロジェクトに多額の予算を投じています。政府は、電気自動車用パワーインバーターメーカーに機会を提供しようとしています。政府はまた、自動車メーカーや顧客に電気自動車の生産と採用を奨励しています。電気自動車の需要の高まりは、パワーインバータなど電気自動車に使用される部品の売上を増加させるとも予想されます。

世界的に排ガス規制が厳しくなるにつれ、自動車メーカーは従来のエンジン車からハイブリッド車や電気自動車へと徐々に生産をシフトしています。加えて、各国政府は、電気自動車の販売成長を支援するため、電気自動車購入者に対する自動車税減税、ボーナス支給、保険料支払いなどのインセンティブを開始しました。特に欧州、北米、アジア太平洋地域、特に日本と中国における充電ステーション設備の増加が、電気自動車販売の伸びをさらに後押ししました。

いくつかのメーカーは、2025年以降の見通しを立てて、電気自動車に関連する発表を超えるハードルを引き上げました。大手OEMのうち10社以上が、2030年以降の電動化目標を宣言しました。重要なのは、一部のOEMが、電気自動車のみを生産するために製品ラインの再構成を計画していることです。例えば、ゼネラルモーターズは第1四半期に、電気自動車と自律走行車に対する支出を2025年までに200億米ドルに引き上げる計画を発表しました。同社は2023年末までに20の新型電気自動車を発売し、予測期間中に米国と中国で年間100万台以上の電気自動車を販売することを目指しました。

電気自動車用パワーインバータの市場動向

電気自動車の販売拡大

電気自動車は自動車産業にとって不可欠な存在となっており、汚染物質やその他の温室効果ガスの排出削減とともに、エネルギー効率の達成に向けた道筋を示しています。環境問題への関心の高まりと政府の積極的な取り組みが、市場の成長を促す主な要因となっています。

2023年、バッテリー電気自動車(BEV)とプラグイン・ハイブリッド車(PHEV)の世界販売台数は35%急増し、1,400万台に達しました。そのうち1,000万台が純粋な電気自動車であるBEVで、400万台がPHEVでした。小型乗用車用電気自動車(EV)の普及を加速させ、従来の内燃機関を搭載した自動車を段階的に廃止していこうという動きは、世界中で活発化しています。平均燃料価格の上昇は、欧州の電気自動車新規登録台数が他の地域よりも高い割合を占めていることを反映しています。したがって、燃料価格の上昇に起因する電気自動車の大量導入は、世界的にビジネスを拡大すると予想されます。

充電インフラ整備への政府投資が世界的に増加していることは、電気自動車の販売を促進すると思われます。例えば、

- 英国政府は、電気自動車の需要増に合わせて、公共の電気自動車充電ステーションの数を100倍以上に拡大し、2030年までに30万カ所に達することを目指しています。

- BPは2023年2月、米国全土の電気自動車(EV)充電ポイントに2030年までに10億米ドルを投入する意向を明らかにしました。これは、BPが総合エネルギー企業へと進化する上で、大きな前進となりました。

さらに、バッテリーに関連する高コストのため、自動車の性能向上とともに、インバーターやその他のパワーエレクトロニクスの改良が必要となりました。

例えば、顧客の嗜好が電気自動車にシフトしていることは、将来の脱炭素化の明白な兆候であり、同時に充電ステーションにとっても決定的なことです。しかし、電気自動車の普及は、消費者の行動、インフラ、特定の地域クラスターなど、さまざまな属性に左右されます。電気自動車の販売台数の増加は、比例して充電ステーションの需要に拍車をかけると予想されます。市場の有力企業は消費者心理を的確に把握しており、全国で急速充電技術を提供することで消費者心理に応えることに注力しています。

この変化は、ICエンジン車の販売不振にはつながらなかったもの、現在と将来において電気自動車の有望な市場を作り出しました。こうした動向を受けて、一部の自動車メーカーは、電気自動車やパワーインバータのような関連部品の研究開発費を増加させました。その一方で、市場シェアを獲得するために新製品の投入に力を入れ始めた自動車メーカーもあり、最終的に市場の需要を押し上げました。

アジア太平洋が電気自動車用パワーインバータ市場を牽引

アジア太平洋地域の電気自動車市場は、環境意識、政府の取り組み、電気自動車(EV)技術の進歩が相まって、近年大幅な成長を遂げています。大気質への関心が高まり、温室効果ガス排出削減へのコミットメントが高まる中、この地域の国々は電気自動車の採用を促進するための支援政策やインセンティブを実施しています。

- 2023年4月には、インドネシアのION Mobility社やベトナムのVinFast社など、東南アジアの新興企業数社が多額の資金を調達し、電気自動車の新モデルを発売しました。

アジア太平洋地域の主要企業である中国は、電気自動車の最大市場として台頭してきました。手厚い補助金やインセンティブ、包括的な充電インフラの整備など、中国政府の強力な支援が、同国における電気自動車の急成長を後押ししています。さらに、電気モビリティの世界的リーダーを目指す中国の動きは、電気自動車製造の技術革新と投資に拍車をかけています。

- 2023年7月には、中国のEV大手BYDが2023年上半期の電気自動車販売台数でテスラを抜いて世界首位となり、世界のEV市場で中国勢が力をつけていることが浮き彫りになりました。

日本や韓国といった国も、アジア太平洋の電気自動車市場で極めて重要な役割を果たしています。有名自動車メーカーの本拠地である日本は、技術の進歩と持続可能な輸送への強いコミットメントによって、電気自動車の導入が着実に増加しています。韓国では、政府の奨励策と研究開発への投資が電気自動車市場の成長に寄与しており、バッテリー技術の強化と充電インフラの拡大に重点が置かれています。

- 日本政府は2023年3月に電気自動車補助金制度を改正し、対象となる電気自動車に対する補助金を延長・増額して電気自動車の普及をさらに促進しました。

- 2023年2月、LGエナジー・ソリューションとホンダは米国にバッテリーセル生産工場を設立する合弁事業を発表し、北米で高まるEV需要に対応するとともに、アジア太平洋市場にも供給する可能性があります。

電動化の野心的な計画を持つインドは、アジア太平洋の電気自動車事情において徐々に重要なプレーヤーになりつつあります。FAME(Faster Adoption and Manufacturing of Hybrid and Electric Vehicles)計画などのインド政府のイニシアチブは、電気自動車の導入にインセンティブを与え、充電インフラの開発を支援することを目的としています。これは、消費者の意識の高まりと相まって、電気自動車用電源インバータ市場にとって好ましい環境を醸成しています。

2023年5月、インドのEV市場は販売急増に見舞われ、単年度の電気自動車販売台数としては最多を記録しました。

電気自動車用パワーインバータ業界の概要

電気自動車用パワーインバータ市場は、Continental AG、Robert Bosch GmbH、株式会社デンソー、三菱電機株式会社など数社が独占しています。各社は、競合他社より優位に立てるよう、新たな生産工場の開設や合弁事業によって事業を拡大しています。例えば

- 2024年6月NXPセミコンダクターズNVとゼット・エフ・フリードリヒスハーフェンAGは、NXPのGD316x HV絶縁ゲート・ドライバを活用した先進的なSiCベースの電気自動車用トラクション・インバータ・ソリューションで協業しました。これらのソリューションは、800VおよびSiCパワーデバイスの採用を促進し、EVの航続距離を延ばし、充電停止時間を減らし、OEMのコストを削減することを目的としています。

- 2024年1月ボルグワーナーはShaanxi Fast Auto Drive Groupと提携し、中国の電気商用車向け高電圧インバータ・ソリューションに注力。

- 2023年11月ダイヤモンド・ウェハー技術を使用した電気自動車用インバーターを開発し、テスラ3のユニットよりも大幅に小型化し、より効率的な電力を供給。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 電気自動車需要の増加が見込まれる

- 市場抑制要因

- インフラ整備の課題、運用面での課題

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 推進力タイプ別

- ハイブリッド電気自動車

- プラグインハイブリッド電気自動車

- バッテリー電気自動車

- 燃料電池電気自動車

- 車両タイプ別

- 乗用車

- 商用車

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Vitesco Technologies

- Robert Bosch GmbH

- DENSO Corporation

- Toyota Industries Corporation

- Hitachi Astemo Ltd

- Meidensha Corporation

- Aptiv PLC(Borgwarner Inc.)

- Mitsubishi Electric Corporation

- Marelli Corporation

- Valeo Group

- Lear Corporation

- Infineon Technologies AG

- Eaton Corporation

第7章 市場機会と今後の動向

- 双方向充電の統合

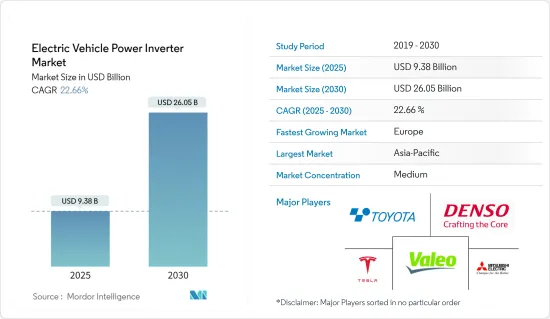

The Electric Vehicle Power Inverter Market size is estimated at USD 9.38 billion in 2025, and is expected to reach USD 26.05 billion by 2030, at a CAGR of 22.66% during the forecast period (2025-2030).

Governments in various countries are spending heavily on electric mobility projects. They are trying to provide opportunities for electric vehicle power inverter manufacturers. The governments are also encouraging automobile manufacturers and customers to produce and adopt electric vehicles. The rise in the demand for electric vehicles is also expected to increase the sales of the components used in electric vehicles, such as power inverters.

With growing stringent emission standards globally, automakers are gradually shifting their production from conventional engine vehicles to hybrid and electric vehicles. In addition, governments initiated incentives, such as a cut down in vehicle tax, bonus payments, and premiums, for buyers of electric vehicles in the respective countries to support electric vehicle sales growth. The increasing charging station facilities in the regions, especially in Europe, North America, and Asia-Pacific, particularly in Japan and China, further supported the growing electric vehicle sales.

Several manufacturers raised the bar to go beyond the announcements related to electric vehicles with an outlook beyond 2025. More than ten of the largest OEMs declared electrification targets for 2030 and beyond. Significantly, some OEMs plan to reconfigure their product lines to produce only electric vehicles. For instance, in the first trimester, General Motors announced its plans to raise its spending on electric and autonomous vehicles to USD 20 billion by 2025. The company launched 20 new electric models by the end of 2023 and aimed to sell more than 1 million electric cars a year in the United States and China over the forecast period.

EV Power Inverter Market Trends

Growing Sales of Electric Vehicles

Electric vehicles have become an integral part of the automotive industry, and they represent a pathway toward achieving energy efficiency, along with reduced emissions of pollutants and other greenhouse gases. The increasing environmental concerns, coupled with favorable government initiatives, are some of the major factors driving the market's growth.

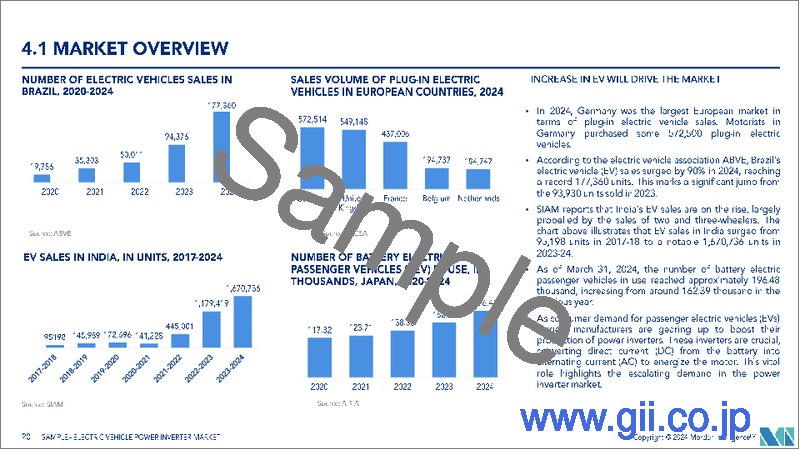

In 2023, global sales of battery electric vehicles (BEVs) and plug-in hybrids (PHEVs) surged by 35%, reaching 14 million units. Among these, 10 million were pure electric BEVs, while 4 million were PHEVs. The movement to accelerate the adoption of light-duty passenger electric cars (EVs) and phase out traditional vehicles with internal combustion engines is gaining traction around the world. The increase in average fuel prices reflects the fact that Europe holds a higher share of new electric car registrations than other parts of the world. Hence, mass adoption of electric vehicles, owing to rising fuel prices, is expected to increase business globally.

Rising government investment in the development of charging infrastructure worldwide is likely to promote the sale of electric vehicles. For instance,

- The UK government aims to expand the quantity of public electric vehicle charging stations by over a hundredfold, reaching 300,000 by 2030, to match the rising demand for electric vehicles.

- In February 2023, BP revealed intentions to inject USD 1 billion by 2030 into electric vehicle (EV) charge points across the United States. It marked a significant stride in the company's evolution toward becoming an integrated energy company.

Moreover, the high cost associated with batteries necessitated the improvement of inverters and other power electronics, along with improving the performance of vehicles.

For instance, shifting customer preference toward electric vehicles is an evident sign of future decarbonization and is simultaneously decisive for charging stations. However, the penetration of EVs is subjected to various attributes, including consumer behavior, infrastructure, and certain regional clusters. The increase in electric vehicle sales is anticipated to proportionally fuel the demand for charging stations. Prominent players in the market have pinpointed consumer sentiment and thus are focusing on catering to it by offering fast-charging technologies across the country.

Though the change did not result in a slump in IC engine vehicle sales, it created a promising market for electric vehicles in the present and future. The above trend propelled some of the automakers to increase their expenditure on R&D in electric vehicles and associated components, like power inverters. While others, on the other hand, started focusing on launching new products to capture the market share, eventually pushing the demand in the market.

Asia-Pacific is leading the Electric Vehicle Power Inverter Market

The Asia-Pacific electric vehicle market has witnessed substantial growth in recent years, driven by a combination of environmental awareness, government initiatives, and advancements in electric vehicle (EV) technology. With a rising concern for air quality and a commitment to reducing greenhouse gas emissions, countries in the region have implemented supportive policies and incentives to promote the adoption of electric vehicles.

- In April 2023, several startups in Southeast Asia, like Indonesia's ION Mobility and Vietnam's VinFast, raised significant funding and launched new electric vehicle models, indicating a growing interest in regional EV production.

China, as a major player in the Asia-Pacific region, has emerged as the largest market for electric vehicles. The Chinese government's robust support, including generous subsidies, incentives, and the establishment of a comprehensive charging infrastructure, has propelled the rapid growth of electric vehicles in the country. Additionally, China's push toward becoming a global leader in electric mobility has spurred innovation and investment in electric vehicle manufacturing.

- In July 2023, Chinese EV giant BYD overtook Tesla as the world's leading electric vehicle seller in the first half of 2023, highlighting the growing strength of Chinese players in the global EV market.

Countries like Japan and South Korea have also played pivotal roles in the Asia-Pacific electric vehicle market. Japan, home to renowned automakers, has seen a steady increase in electric vehicle adoption, driven by technological advancements and a strong commitment to sustainable transportation. In South Korea, government incentives and investments in research and development have contributed to the growth of the electric vehicle market, with a focus on enhancing battery technology and expanding charging infrastructure.

- In March 2023, the Japanese government revised its EV subsidy program, extending it and increasing benefits for eligible electric vehicles to further promote EV adoption.

- In February 2023, LG Energy Solution and Honda announced a joint venture to establish a battery cell production plant in the United States, catering to the growing demand for EVs in North America and potentially supplying the Asia-Pacific market as well.

India, with its ambitious plans for electrification, is gradually becoming a significant player in the Asia-Pacific electric vehicle landscape. The Indian government's initiatives, such as the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme, aim to incentivize electric vehicle adoption and support the development of charging infrastructure. This, coupled with increasing consumer awareness, is fostering a positive environment for the electric vehicle power inverter market.

In May 2023, the Indian EV market experienced a surge in sales, registering the highest number of electric vehicles sold in a single year, driven by rising fuel prices and increasing awareness of environmental benefits.

EV Power Inverter Industry Overview

A few players, such as Continental AG, Robert Bosch GmbH, DENSO Corporation, and Mitsubishi Electric Corporation, dominate the electric vehicle power inverter market. Companies are expanding their business by opening new production plants and making joint ventures so that they can gain an edge over their competitors. For instance,

- June 2024: NXP Semiconductors NV and ZF Friedrichshafen AG collaborated on advanced SiC-based traction inverter solutions for EVs, utilizing NXP's GD316x HV isolated gate drivers. These solutions aim to expedite the adoption of 800-V and SiC power devices, enhancing EV range, reducing charging stops, and lowering costs for OEMs.

- January 2024: BorgWarner, in partnership with Shaanxi Fast Auto Drive Group, is focusing on high-voltage inverter solutions for electric commercial vehicles in China.

- November 2023: Diamond Foundry Inc. developed an electric car inverter using diamond wafer technology, which was significantly smaller than Tesla 3's unit and delivered more efficient power.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Demand for Electric Vehicles Is Expected to Increase the Demand

- 4.2 Market Restraints

- 4.2.1 Infrastructure Challenges May Possess Operational Challenges

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Propulsion Type

- 5.1.1 Hybrid Electric Vehicles

- 5.1.2 Plug-in Hybrid Electric Vehicle

- 5.1.3 Battery Electric Vehicle

- 5.1.4 Fuel Cell Electric Vehicle

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Vitesco Technologies

- 6.2.2 Robert Bosch GmbH

- 6.2.3 DENSO Corporation

- 6.2.4 Toyota Industries Corporation

- 6.2.5 Hitachi Astemo Ltd

- 6.2.6 Meidensha Corporation

- 6.2.7 Aptiv PLC (Borgwarner Inc.)

- 6.2.8 Mitsubishi Electric Corporation

- 6.2.9 Marelli Corporation

- 6.2.10 Valeo Group

- 6.2.11 Lear Corporation

- 6.2.12 Infineon Technologies AG

- 6.2.13 Eaton Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration of Bidirectional Charging