|

市場調査レポート

商品コード

1687371

粉末冶金:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Powder Metallurgy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 粉末冶金:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

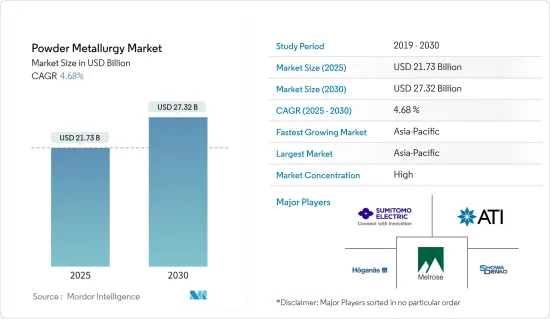

粉末冶金の市場規模は2025年に217億3,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.68%で、2030年には273億2,000万米ドルに達すると予測されます。

2020年にはCOVID-19が市場にマイナスの影響を与えました。しかし、現在、市場はパンデミック以前の水準に達したと推定されており、今後も安定した成長が見込まれます。

主なハイライト

- 粉末冶金は自動車OEMでますます使用されるようになっており、これが市場を牽引する主な要因のひとつとなっています。さらに、電気的・電磁的アプリケーションの導入が拡大していることも、市場の成長をもたらすと予想されます。

- 一方、原材料や工具のコスト上昇は市場の成長を鈍らせる可能性が高いです。

- 航空宇宙・防衛分野の急成長とともに、医療分野での粉末冶金の採用が増加していることは、市場に機会をもたらすと予想されます。

- 粉末冶金市場はアジア太平洋地域がリードしており、今後数年間で最も高い成長率が見込まれています。

粉末冶金市場動向

自動車用途が市場を独占

- 粉末冶金部品は、多孔質度を自在にコントロールでき、それ自体に潤滑性を持たせることができるため、ガスや液体をろ過することができます。このため、粉末冶金は複雑な曲げ、窪み、突起を持つ部品を作るのに非常に適した方法です。

- 金属と非金属、金属と金属の組み合わせなど、多様な組成の機械部品を開発できるこの柔軟性により、寸法精度の高い自動車部品の製造が可能になり、スクラップや材料の無駄をほとんど出さずに一貫した特性と寸法を確保できます。

- ベアリングとギアは、粉末冶金プロセスで製造される最も一般的な自動車部品です。このプロセスは、シャーシ、ステアリング、エキゾースト、トランスミッション、ショックアブソーバー部品、エンジン、バッテリー、シート、エアクリーナー、ブレーキディスクなど、自動車の多数の部品にも使用されています。

- 自動車部品は、鉄(鉄、鋼、合金鋼、ステンレス鋼)および非鉄(銅、青銅、アルミニウム合金、チタン合金)などの幅広い金属から作られています。粉末冶金の焦点は、ネットシェイプを改善し、熱処理を利用し、特殊な表面処理を施し、精度を向上させることです。

- 欧州自動車工業会(ACEA)の報告によると、2022年第1~3四半期には、世界で約5,000万台の乗用車が製造され、2021年同期比で9%近く増加しました。

- また、中国自動車製造協会によると、同国で製造された新エネルギー自動車の台数は、2021年12月から2022年12月にかけて96.9%増加しました。このように、電気自動車市場の拡大は、予測期間中の市場需要を増加させると予想されます。

- このような要因から、自動車分野における粉末冶金の需要は増加しています。

アジア太平洋が市場を独占する

- アジア太平洋は、最も重要な粉末冶金市場のひとつとなっており、経済が成長し、人々がより多くの資金を使えるようになったため、メーカーにとって最重要の投資先となっています。

- 中国、インド、日本などの国々の良好な経済動向は、近年粉末冶金製品とアプリケーションの需要を押し上げています。

- 中国汽車工業協会(CAAM)によると、中国は世界最大の自動車生産拠点です。2022年には、中国で2,700万台の自動車が生産される見込みで、これは2017年の2,600万台より3.4%多いです。

- さらに、2022年の最初の7ヵ月間で、同国は1,457万台の自動車を生産し、前年比31.5%の成長率を記録しました。

- また、インド自動車工業会(SIAM)によると、インドの自動車産業は、2020-21年度(2020年4月~2020年3月)の2,265万5,609台に対し、2021-22年度(2021年4月~2022年3月)は2,293万3,230台を生産するといいます。

- さらに、この地域では航空宇宙産業も大きく成長しています。例えば、ボーイング商業見通し2022-2041は、2041年までに8,485機、市場サービス額5,450億米ドルが中国で新たに納入されると予測しています。

- したがって、前述の要因から、予測期間中はアジア太平洋が市場を独占する可能性が高いです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車OEMによる粉末冶金への嗜好の高まり

- 電気・電磁波用途での採用拡大

- 抑制要因

- 原材料と金型コストの上昇

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ

- 鉄

- 非鉄

- 用途

- 自動車

- 産業機械

- 電気・電子

- 航空宇宙

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ATI

- Catalus Corporation

- fine-sinter Co., Ltd.

- H.C. Starck Tungsten GmbH

- Showa Denko Materials Co., Ltd.

- Hoganas AB

- Horizon Technology

- Melrose Industries PLC

- Miba AG

- Perry Tool & Research, Inc.

- Phoenix Sintered Metals, LLC

- Precision Sintered Parts

- Sandvik AB

- Sumitomo Electric Industries, Ltd.

第7章 市場機会と今後の動向

- 医療分野における粉末冶金技術の採用増加

- 航空宇宙・防衛分野の急成長

The Powder Metallurgy Market size is estimated at USD 21.73 billion in 2025, and is expected to reach USD 27.32 billion by 2030, at a CAGR of 4.68% during the forecast period (2025-2030).

In 2020, COVID-19 negatively impacted the market. However, the market has now been estimated to have reached pre-pandemic levels and is expected to grow steadily in the future.

Key Highlights

- Powder metallurgy is being used more and more by automotive OEMs, which is one of the main things driving the market. Moreover, the growing implementation of electrical and electromagnetic applications is also expected to provide market growth.

- On the other hand, rising costs of raw materials and tools are likely to slow the market's growth.

- The increasing adoption of powder metallurgy in the medical field along with the rapid growth in the aerospace and defense sector is expected to provide opportunities to the market.

- The Asia-Pacific region led the market for powder metallurgy, and it is expected to have the highest growth rate over the next few years.

Powder Metallurgy Market Trends

Automotive Applications to Dominate the Market

- Powder metal parts have great control over how porous they are and can lubricate themselves, which lets them filter gases and liquids.Because of this, powder metallurgy is a very good way to make parts that have complicated bends, depressions, and projections.

- This flexibility to develop mechanical parts with diverse compositions, such as metal-nonmetal and metal-metal combinations, enables the production of automotive parts with high dimensional accuracy and ensures consistent properties and dimensions with very little scrap and material waste.

- Bearings and gears are the most common vehicle parts made through the powder metallurgy process. The process is also used for a large number of parts in a vehicle, including the chassis, steering, exhaust, transmission, shock absorber parts, engine, battery, seats, air cleaners, brake discs, etc.

- Auto parts are made from a wide range of metals, such as ferrous (iron, steel, alloy steel, and stainless steel) and non-ferrous (copper, bronze, aluminum alloys, and titanium alloys).The focus of powder metallurgy is to improve the net shape, utilize heat treatment, provide special surface treatment, and improve precision.

- In the first three quarters of 2022, around 50 million passenger cars were manufactured worldwide, up nearly 9% compared to the same quarter in 2021, as per the report of the European Automobile Manufacturers' Association (ACEA).

- Also, the China Association of Automobile Manufacturing says that the number of New Energy Vehicles made in the country rose by 96.9% from December 2021 to December 2022.Thus, the expanding electric vehicle market is expected to increase market demand during the forecast period.

- Due to such factors, the demand for powder metallurgy in the automotive sector is increasing.

Asia-Pacific to Dominate the Market

- Asia-Pacific has become one of the most important powder metallurgy markets and a top destination for manufacturers because its economy is growing and people have more money to spend.

- The positive economic growth trends in countries such as China, India, and Japan have boosted the demand for powder metallurgy products and applications in recent years.

- China has the largest automotive production base in the world, according to the China Association of Automobile Manufacturers (CAAM). In 2022, 27 million vehicles were expected to be made in China, which is 3.4% more than the 26 million vehicles made in 2017.

- Further, in the first 7 months of 2022, the country produced 14.57 million units of cars, registering a growth rate of 31.5% year over year.

- Also, the Society of Indian Automobile Manufacturers (SIAM) said that India's automotive industry will make 22,933,230 vehicles in FY 2021-22 (April 2021-March 2022), compared to 22,655,609 units in FY 2020-21 (April 2020-March 2020).

- Furthermore, the aerospace industry is also growing significantly in the region. For instance, the Boeing Commercial Outlook 2022-2041 predicts that by 2041, 8,485 new deliveries with a market service value of USD 545 billion will take place in China.thus boosting market growth.

- Hence, due to the aforementioned factors, Asia-Pacific is likely to dominate the market during the forecast period.

Powder Metallurgy Industry Overview

The powder metallurgy market is consolidated in nature. Some of the major players in the market (not in any particular order) include Melrose Industries PLC, Sumitomo Electric Industries, Ltd., Hoganas AB, ATI, and Showa Denko Materials Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Preference for Powder Metallurgy by Automotive OEMs

- 4.1.2 Growing Implementation in Electrical and Electromagnetic Applications

- 4.2 Restraints

- 4.2.1 Increasing Raw Material and Tooling Costs

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Ferrous

- 5.1.2 Non-ferrous

- 5.2 Application

- 5.2.1 Automotive

- 5.2.2 Industrial Machinery

- 5.2.3 Electrical and Electronics

- 5.2.4 Aerospace

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ATI

- 6.4.2 Catalus Corporation

- 6.4.3 fine-sinter Co., Ltd.

- 6.4.4 H.C. Starck Tungsten GmbH

- 6.4.5 Showa Denko Materials Co., Ltd.

- 6.4.6 Hoganas AB

- 6.4.7 Horizon Technology

- 6.4.8 Melrose Industries PLC

- 6.4.9 Miba AG

- 6.4.10 Perry Tool & Research, Inc.

- 6.4.11 Phoenix Sintered Metals, LLC

- 6.4.12 Precision Sintered Parts

- 6.4.13 Sandvik AB

- 6.4.14 Sumitomo Electric Industries, Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Adoption of Powder Metallurgy Techniques in Medical Sector

- 7.2 Rapid Growth in Aerospace and Defense Sector