シールコート:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Seal Coat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687366

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

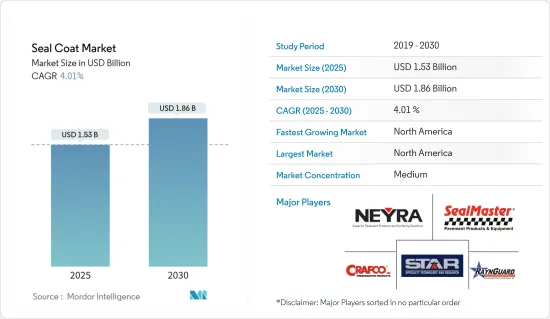

シールコートの市場規模は2025年に15億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.01%で、2030年には18億6,000万米ドルに達すると予測されています。

COVID-19のパンデミックが世界のシールコート市場の足かせとなりました。原材料の入手不能、労働者の不足、サプライチェーンの混乱により、建設業界は行き詰まりました。しかし、パンデミック後の建設業界の増加は、シールコートの消費を促進すると思われます。

主なハイライト

- 中期的には、商業建設活動の増加と、道路や車道の寿命を延ばすための舗装工事が、世界のシールコート市場を牽引する主な要因となっています。

- しかし、環境に関する厳しい規則や、がんの原因となる多環芳香族炭化水素(PAH)による健康リスク、多くの地域でコールタール系シールコートが禁止されていることなどが、今後数年間の市場の成長を鈍らせると予想されます。

- しかしながら、先進国や新興諸国における改修・補修活動の高まりは、業界に新たな成長機会をもたらす可能性があります。

- 北米が世界市場を独占しており、米国やカナダなどの国々でシールコートの消費が最も多くなっています。

シールコートの市場動向

舗装セグメントからの需要増加

- シールコーティングは、駐車場や私道の建設に使用されるアスファルトバインダーやその他の材料の影響を軽減し、寿命を延ばすために使用されます。

- さらに、シールコーティングは、水、油、紫外線(UV)ダメージなどの有害な侵入をブロックすることで、保護層を提供します。これらのコーティングにより、滑りにくい表面が実現され、深みのある黒色仕上げにより見た目も美しく、駐車場や車道に壮麗さが加わります。

- 車道や駐車場は、ガソリンや水などの過度の化学物質にさらされます。このような外部要素は、アスファルトの層を弱め、最終的には破損する可能性があります。シールコートを塗布することで、そのような化学物質や水、さらには紫外線に対するバリアとして機能します。また、車道や駐車場のひび割れや損傷の修理に費やす費用と時間を節約し、その寿命を延ばすことができます。

- 北米や欧州では、ほとんどすべての建物(小さなものから大きな住宅や高層ビルまで)に私道や駐車場があります。さらに、ショッピングセンター、学校、病院、ショッピングモール、シネコン、スタジアム、空港などにも私道や駐車場があります。これらの地域では、このような建物やその他の商業施設の建設が増加しており、将来的にシールコートの市場を牽引すると予想されています。

- また、全米アスファルト舗装協会(NAPA)によると、米国では駐車場の90%以上がアスファルト舗装です。したがって、駐車場の新設は、アスファルト舗装の保全に必須であるため、シールコートの需要に大きな影響を与えると思われます。

- 欧州では小売業が拡大しており、大陸各地に新しいモールが建設されています。ロシアのVegas Kuntsevo、スウェーデンのMall of Scandinavia、英国のWestfield Bradford、オーストリアのWeberzeile Ried、ベルギーのMall of Europe、ポーランドのLublin Mallなどが欧州で最近建設されたモールです。

- ドイツ連邦統計局(Statistisches Bundesamt)によると、ドイツの道路・高速道路建設業界の収益は2025年までに354億2,000万米ドルに達すると予測されており、シールコーティング市場の強化につながります。

- インドでは、2023~2024年にかけて、道路建設プロジェクトは12,349kmの距離をカバーすると予想され、前年比20%の大幅増となります。このうち9,642kmは車線の拡張が中心で、2,707kmは現在のインフラの補強に充てられます。

- 2023年3月、ドイツでは24,500戸の住宅建設が承認され、建築許可件数は10,300件減少しました。2022年3月と比較して29.6%の減少に相当します。これは駐車場や車道に影響を及ぼし、シールコーティング申請にも影響を及ぼしました。

- 国家統計局のデータによると、英国全土の建設活動の総額は2022年に260億米ドルを超える大幅な成長を示し、2020年に観測された生産高の大幅な落ち込みから回復しました。

- したがって、前述の要因はすべて舗装セグメントを促進し、予測期間中にシールコーティングの需要を高めると予想されます。

北米市場を独占する米国

- シールコートは、舗装、車道、道路、競馬場、その他の資本資産の寿命を延ばす物質であり、水、ごみ、化学物質の漏れ、紫外線、その他の要因による自然な老化プロセスから舗装を保護します。99%以上が他のプロジェクトで再利用できるため、米国のほとんどの舗装はアスファルトで作られています。

- 米国国勢調査局によると、米国の駐車場とガレージの業界売上高は、2024年までに112億7,000万米ドルに達すると予測され、シールコーティング市場を強化しています。

- 全米アスファルト舗装協会(NAPA)によると、約3,600のアスファルト混合物生産拠点が国内で操業しており、年間約4億2,000万トンのアスファルト舗装材を生産しています。毎年、航空業界は空港改善プログラムから40億米ドルの補助金と旅客施設使用料を受け取っており、これらは飛行場の滑走路、エプロン、誘導路に費やされています。

- 2022年、米国運輸省の連邦航空局(FAA)は、米国全土の空港ターミナルを改善するため、Bipartisan Infrastructure Lawから約10億米ドルの資金提供を受けると発表しました。この資金により、米国全土の85の空港ターミナルで、収容能力の拡大、エネルギー効率の向上、アクセシビリティの向上などの改善が進められる見込みです。

- さらにFAAは、ノースカロライナ州のアッシュビル・リージョナル空港(AVL)で新しい航空管制塔の建設が進行中であることを発表しました。エネルギー効率に優れたこの新しい管制塔は、拡張され近代化されたターミナルとともに、同地域における航空需要の増大に対応するものです。タワーの高さは127フィート(約127メートル)で、上部には3人の管制官用の440平方フィートの運転室が設置されます。

- さらに、米国国勢調査局(USCB)によると、同国はまた、さまざまな開発段階にある多数の商業建設プロジェクトに着手しています。

- 国内で進行中の商業プロジェクトには、ラスベガスのForbidden CityとAll Net Arena & Resort、ハワイのKo Olina Atlantis Resort、フロリダのMiami Herald Redevelopment、ワシントンDCのThe Wharf-Phase 2などがあります。このようなプロジェクトの開発には、車道や駐車場の新設が必要であり、今後数年間はシールコートの需要が増加します。

- さらに、国のアスファルト舗装支出の約35%は、住宅と非住宅建設セグメントで記録されています。また、米国の商業ビル建設への支出は、予測期間中、毎年4%以上成長すると推定されています。

- 同国では核家族化が進んでおり、アパートが主要な嗜好のひとつとなっているため、高層住宅やタウンシップの建設が進み、こうしたセグメントでは駐車スペース、歩道、車道が増加しています。

- したがって、これらの要因が北米におけるシールコートの需要を押し上げ、業界全体の成長を促進すると予想されます。

シールコート業界の概要

シールコート市場は非常に細分化されており、市場シェアは多くのプレーヤーに分かれています。主なプレーヤーとしては、Seal Master、RaynGuard、Neyra、Star Seal Inc.、Crafcoなどが挙げられます(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 舗装工事の増加

- 商業建設活動の増加

- その他

- 抑制要因

- 多くの地域におけるコールタール系シールコートの使用禁止

- その他

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ別

- アスファルト系

- コールタール系

- アクリル系

- その他

- 用途別

- 舗装

- 車道・駐車場

- 車道・歩道

- 競馬場・スポーツ

- 補修・改修

- 舗装

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ノルディック

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析

- 主要企業の戦略

- 企業プロファイル

- Asphalt Coatings Engineering Inc.

- Crafco Inc.

- Fahrner Asphalt Sealers LLC

- GemSeal Pavement Products

- Go Green Lehong New Material Technology(Shanghai)Co. Ltd

- GoldStar Asphalt Products

- GuardTop

- Neyra

- Raynguard

- SealMaster

- Star Seal Inc.

- Vance Brothers Inc.

- Western Colloid

- Wolf Paving

第7章 市場機会と今後の動向

- 改修・補修活動の活発化

目次

The Seal Coat Market size is estimated at USD 1.53 billion in 2025, and is expected to reach USD 1.86 billion by 2030, at a CAGR of 4.01% during the forecast period (2025-2030).

The COVID-19 pandemic hampered the global seal coat market. The construction industry came to a standstill due to the unavailability of raw materials, the shortage of laborers, and disruptions in the supply chain. However, the upsurge in the construction industry post-pandemic is likely to drive the consumption of seal coats.

Key Highlights

- Over the medium term, increasing commercial construction activities and pavement construction to extend the lifespan of roads and driveways are major factors driving the global seal coat market.

- However, strict rules about the environment, health risks caused by polycyclic aromatic hydrocarbons (PAHs), which can cause cancer, and a ban on coal tar-based seal coats in many regions are expected to slow the growth of the market over the next few years.

- Nevertheless, the rising refurbishment and repair activities in developed and developing countries may offer new growth opportunities for the industry.

- North America dominates the global market, with the largest consumption of seal coating in countries such as the United States and Canada.

Seal Coat Market Trends

Rising Demand from the Pavements Segment

- Seal coatings are used to reduce the effects of asphalt binders or other materials used in parking lots or driveway construction, thereby increasing their lifespan.

- Furthermore, seal coatings provide a layer of protection by blocking harmful intrusions such as water, oils, and ultraviolet (UV) ray damage. These coatings also result in a slip-resistant surface and are aesthetically pleasing owing to their deep black finish, which adds magnificence to the parking lot or driveway.

- Driveways or parking lots are exposed to excessive chemicals like gasoline and water. Such external elements can weaken and eventually destroy the layers of asphalt. Applying a seal coat acts as a barrier to such chemicals, water, and even UV rays. It also saves money and time spent repairing cracks and damage to the driveway or parking lot, extending its lifespan.

- In North America and Europe, almost every building (small to big housing or high-rise buildings) has driveways and parking lots. Additionally, shopping centers, schools, hospitals, malls, multiplexes, stadiums, airports, etc., have driveways and parking lots. Increasing construction of such buildings and other commercial institutions in these regions is expected to drive the market for seal coats in the future.

- Moreover, according to the National Asphalt Pavement Association (NAPA), more than 90% of parking areas in the United States are surfaced with asphalt pavement. Therefore, the new construction of parking areas will significantly impact the demand for seal coats, as they are mandatory for asphalt pavement preservation.

- Europe is expanding in retail, with the construction of new malls across the continent. The Vegas Kuntsevo in Russia, Mall of Scandinavia in Sweden, Westfield Bradford in the United Kingdom, Weberzeile Ried in Austria, Mall of Europe in Belgium, and Lublin Mall in Poland are some of the recent constructions in Europe.

- According to the Statistisches Bundesamt, the industry revenue for the construction of roads and motorways in Germany is projected to reach USD 35.42 billion by 2025, thus strengthening the seal coatings market.

- In India, from 2023 to 2024, road-building projects are expected to cover a distance of 12,349 km, representing a significant 20% rise compared to the previous year. The bulk of the work, amounting to 9,642 km, is focused on expanding lanes, whereas 2,707 km is dedicated to reinforcing current infrastructure.

- In March 2023, Germany saw the approval of construction for 24,500 dwellings, marking a decline of 10,300 building permits, equivalent to a 29.6% decrease compared to March 2022. This affected parking lots and driveways and subsequently affected seal coating applications.

- As per the data from the Office for National Statistics, the total value of construction activities across Great Britain witnessed a substantial growth of over USD 26 billion in 2022, rebounding from a significant downturn in output observed in 2020.

- Hence, all the aforementioned factors are expected to drive the pavements segment, enhancing the demand for seal coating during the forecast period.

The United States to Dominate the North American Market

- Seal coats are substances that extend the life of pavements, driveways, roadways, racetracks, and other capital assets by protecting the pavement from the natural aging process caused by water, debris, chemical leaks, ultraviolet rays, and other factors. Most pavements in the United States are made of asphalt because more than 99% can be reused in other projects.

- According to the US Census Bureau, the industry revenue of parking lots and garages in the United States is projected to reach USD 11.27 billion by 2024, strengthening the seal coating market.

- According to the National Asphalt Pavement Association (NAPA), about 3,600 asphalt mix production sites operate in the country, producing around 420 million metric tons of asphalt pavement material annually. Every year, the aviation industry receives grants and passenger facility charges of USD 4 billion from the Airport Improvement Program, which is spent on airfield runways, aprons, and taxiways.

- In 2022, the US Department of Transportation's Federal Aviation Administration (FAA) announced nearly USD 1 billion in funding from the Bipartisan Infrastructure Law to improve airport terminals across the United States. The funding is expected to advance improvements at 85 airport terminals throughout the United States to expand capacity, increase energy efficiency, and provide greater accessibility.

- Furthermore, the FAA announced that construction is underway on a new air traffic control tower at Asheville Regional Airport (AVL) in North Carolina. The new energy-efficient tower will help the airport meet the growing demand for air travel in the region alongside an expanded and modernized terminal. It will be 127 feet tall and topped by a 440-square-foot cab for three air traffic controllers.

- Furthermore, according to the United States Census Bureau (USCB), the country is also embarking on a significant number of commercial construction projects, all in various stages of development.

- Some commercial projects underway in the country include the Forbidden City and All Net Arena & Resort in Las Vegas, the Ko Olina Atlantis Resort in Hawaii, the Miami Herald Redevelopment in Florida, and The Wharf-Phase 2 in Washington DC. The development of all such projects will require the construction of new driveways and parking lots, increasing the demand for seal coats in the coming years.

- Furthermore, about 35% of the country's asphalt pavement expenditures are recorded in the residential and non-residential construction segments. Besides, the United States's expenditures on commercial building construction are estimated to grow by more than 4% annually over the forecast period.

- With the increased trend of nuclear families in the country, apartments have become one of the major preferences, leading to the construction of high-rise residential buildings and townships, thus increasing parking spaces, walkways, and driveways in such segments.

- Therefore, these factors are expected to boost the demand for seal coats in North America, propelling the overall industry's growth.

Seal Coat Industry Overview

The seal coat market is highly fragmented, as the market share is divided among many players. Some of the key players include (not in any particular order) Seal Master, RaynGuard, Neyra, Star Seal Inc., and Crafco.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increase in Pavement Construction

- 4.1.2 Growing Commercial Construction Activities

- 4.1.3 Others

- 4.2 Restraints

- 4.2.1 Ban on Coal Tar-based Seal Coats in Many Regions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Asphalt-based

- 5.1.2 Coal Tar-based

- 5.1.3 Acrylic-based

- 5.1.4 Other Product Types

- 5.2 Application

- 5.2.1 Pavements

- 5.2.1.1 Driveways and Parking Lots

- 5.2.1.2 Roadways and Walkways

- 5.2.1.3 Racetrack and Sports

- 5.2.2 Repair and Refurbishment

- 5.2.1 Pavements

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis ** / Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Asphalt Coatings Engineering Inc.

- 6.4.2 Crafco Inc.

- 6.4.3 Fahrner Asphalt Sealers LLC

- 6.4.4 GemSeal Pavement Products

- 6.4.5 Go Green Lehong New Material Technology (Shanghai) Co. Ltd

- 6.4.6 GoldStar Asphalt Products

- 6.4.7 GuardTop

- 6.4.8 Neyra

- 6.4.9 Raynguard

- 6.4.10 SealMaster

- 6.4.11 Star Seal Inc.

- 6.4.12 Vance Brothers Inc.

- 6.4.13 Western Colloid

- 6.4.14 Wolf Paving

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Refurbishment and Repairing Activities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日