|

市場調査レポート

商品コード

1687356

北米のチョコレート:市場シェア分析、産業動向、成長予測(2025~2030年)North America Chocolate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のチョコレート:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

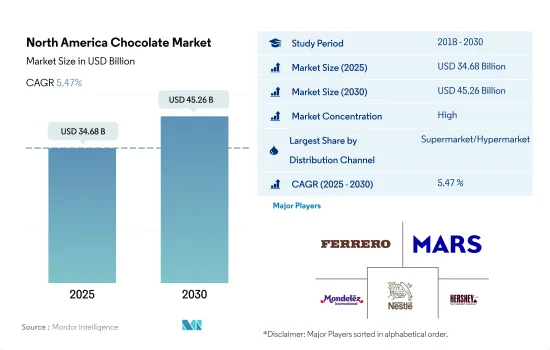

北米のチョコレート市場規模は2025年に346億8,000万米ドルと推定・予測され、2030年には452億6,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは5.47%で成長すると予測されます。

北米の流通はスーパーマーケット/ハイパーマーケットとその他のセグメントが支配的で、2023年の市場シェアはこれらを合わせて70%近くを占める

- 北米の流通チャネル全体がチョコレート市場の成長に重要な役割を果たしています。全体的な流通セグメントでは、小売業者は消費者の関心を引きつけるために多種多様なチョコレート製品を提供しています。さらに、小売業者はチョコレートを多種多様なフレーバー、テクスチャー、パッケージなどにセグメント化しています。2023年、金額ベースでは、流通チャネル全体のシェアは2022年比で5.16%の成長を記録しました。

- 金額ベースでは、スーパーマーケットとハイパーマーケットが北米の主要小売業者と考えられています。これらの小売業者は、様々な価格帯(低価格、中価格、高価格)でチョコレートを販売しています。2023年のダークチョコレートの平均販売価格は3.12米ドルでした。この地域の消費者の購買力を促進するため、それぞれの側面から、消費者は主にこれらの小売店に向かっています。

- コンビニエンスストアは2番目に大きな小売業者であり、2022年には小売チャネルの重要な一部となりました。これらのコンビニエンスストアは、消費者により大きな利便性を提供することができます。2023年には、Becker'sがオンタリオ州で45店舗を所有していることが確認されました。

- オンライン小売部門は、2023年に北米で最も急成長する小売企業に浮上しました。インターネット・ユーザーの普及に伴い、オンライン食料品店への需要は、この地域の小売セグメントにとって重要な要素となっています。2021年末までに、米国のインターネットユーザー総数は8,950万人で、総人口の75.7%を占めました。

- 予測期間中(2026-2029年)、同市場は金額ベースで5.58%の成長が見込まれています。チョコレート産業を牽引する主な要因は、人口の間で高級チョコレートへの需要が高まっていることと関連しています。

調査期間中、米国が地域別金額でリードし、次いでカナダが2023年に金額で90%のシェアを占める。

- 北米のチョコレート部門は、2023年に2022年比5.16%の成長率を記録しました。フレーバーの多様化、可処分所得の増加、消費者の嗜好の変化が、この地域におけるチョコレート需要の拡大につながりました。

- 米国は、同国で最も高いチョコレート製品の消費量に支えられ、同地域で主要なシェアを占めています。2023年、米国のチョコレート消費量は約257億6,700万米ドルに達し、2021年から10.1%の伸びを示しました。シングルオリジンチョコレート、ハンドメイドチョコレート、ダークチョコレート、オーガニックチョコレートなどの高品質チョコレート製品への消費者のシフトは、同国のチョコレートセグメントを牽引する重要な要因です。

- 消費者は様々な種類のチョコレートを好むため、ノベルティチョコレート、砂糖不使用チョコレート、ギフトボックス、スナックサイズのチョコレートバーなどのカテゴリーはプレミアムとみなされ、米国で広く販売されています。2022年現在、同国の消費者の78%はチョコレートが自分を幸せにしてくれることに同意し、81%はチョコレートを生活の楽しみの一部と考えています。

- カナダは、この地域におけるチョコレート製品の売上高で第2位の国です。カナダにおけるチョコレートの販売額は、2022年と比較して2026年には26.6%成長すると予測されています。カナダ人は健康志向を強めており、チョコレートのような嗜好品であっても、より健康的な代替品を求めています。カカオ含有量が高く、添加物の含有量が少ないとされるダークチョコレートは、その潜在的な健康効果から人気を集めています。

北米のチョコレート市場動向

職人技が光るチョコレートへの需要の高まりと、クリスマスやハロウィンなどの特別な日の強い需要が、チョコレート市場の成長を可能にしています。

- チョコレートは北米の人々の間で、時代を超えて愛され続けています。2023年の金額シェアは44%で、チョコレートはこの地域で最も頻繁に消費される菓子類であり続けると予想されます。アメリカ人は毎年約28億ポンドのチョコレートを消費しており、2023年時点でアメリカ人の77%が少なくとも月に1回はチョコレートを消費しています。

- チョコレートに対する消費者の第一印象は、他の属性の中でも、パッケージと風味に左右されます。米国では、ほとんどの消費者(90%)がチョコレートを好んで食べています。これは、チョコレートが50%以上のアメリカ人の一般的な好みの味だからです。

- チョコレートの価格は、1ポンドあたり3.1米ドルから24米ドルまでと幅広いです。アメリカ人の約半数(47%)は、2023年に食料品店で月に数回、5~10米ドル相当のチョコレートを購入しています。

- 北米では、チョコレートの消費は一般的に健康(身体的・精神的)の観点から見られており、さまざまな意見があります。チョコレートは多くの人が楽しんでいる人気のあるお菓子であるが、その健康上の利点と潜在的な欠点に関する考察があります。

北米のチョコレート産業概要

北米のチョコレート市場はかなり統合されており、上位5社で68.27%を占めています。この市場の主要企業は以下の通りです。Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA and The Hershey Company(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子類

- ダークチョコレート

- ミルクチョコレートとホワイトチョコレート

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット/ハイパーマーケット

- その他

- 国

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Albanese Confectionery Group Inc.

- Askinosie Chocolate

- Chocoladefabriken Lindt & Sprungli AG

- Ezaki Glico Co. Ltd

- Ferrero International SA

- Guittard Chocolate Company

- Lake Champlain Chocolates

- Mars Incorporated

- Mast Brothers & Co.

- Mondelez International Inc.

- Nestle SA

- The Hershey Company

- Theo Chocolate Inc.

- Vosges Haut-Chocolat LLC

- YIldIz Holding AS

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The North America Chocolate Market size is estimated at 34.68 billion USD in 2025, and is expected to reach 45.26 billion USD by 2030, growing at a CAGR of 5.47% during the forecast period (2025-2030).

The North American distribution network is dominated by supermarkets/hypermarkets and other segments, which together make up almost 70% of the market share in 2023

- The overall distribution channel in North America is playing a vital role in the growth of the chocolate market. Under the overall distribution segment, the retailers offer a wide variety of chocolate products to drag the consumer focus. In addition, the retailers have segmented the chocolates into a wide variety of flavors, textures, packaging, etc. In 2023, by value, the overall share of the distribution channel registered a growth of 5.16% compared to 2022.

- By value, supermarkets and hypermarkets were considered the major retailers in North America. These retailers sell chocolates in varied price ranges (low, medium, and high). The average selling price of dark chocolate was USD 3.12 in 2023. Due to the respective aspect, consumers are majorly trending toward these retailing units as it is promoting the consumer buying power in this region.

- Convenience stores were the second largest retailers and became an important part of the retailing channel in 2022. These stores have the capability of offering a greater convenience experience to their consumers. In 2023, it was observed that Becker's owed 45 stores in Ontario.

- The online retailing segment emerged to be the fastest-growing retailer in North America in 2023. With the growing penetration of internet users, the demand for online grocery has become a crucial part of the region's retailing segment. By the end of 2021, the total number of internet users in the United States was 89.5 million, or 75.7% of the total population.

- During the forecast period (2026-2029), it is expected that the market will grow by 5.58% by value. The major factor that will be driving the chocolate industry is linked to the growing demand for premium chocolates among the population.

The United States leads the regional value during the study period, followed by Canada together held a share of 90% by value in 2023

- The chocolate segment in North America registered a growth rate of 5.16% in 2023 compared to 2022. The diversification of flavors, increasing disposable income, and changing consumer preferences have led to the growing demand for chocolate in the region.

- The United States holds the major share in the region, supported by the highest consumption of chocolate products in the country. In 2023, the consumption of chocolates in the United States reached around USD 25,767 million, which represented a 10.1% growth from 2021. The consumer's shift toward high-quality chocolate products, such as single-origin chocolates, handmade chocolates, dark chocolates, organic chocolates, and other chocolate products, is a significant factor driving the chocolate segment in the country.

- As consumers prefer various types of chocolates, categories such as novelty chocolates, sugar-free chocolates, gift boxes, and snack-size chocolate bars are considered premium and are widely sold in the United States. As of 2022, 78% of the consumers in the country agreed that chocolate makes them happy, and 81% of the consumers see chocolates as a fun part of life.

- Canada is the second-leading country for the sales of chocolate products in the region. The sales value of chocolates in Canada is anticipated to grow by 26.6% in 2026 compared to 2022. Canadians are becoming more health-conscious and are seeking healthier alternatives, even when it comes to indulgent treats like chocolate. Dark chocolate, which is perceived as being higher in cocoa content and containing fewer additives, has gained popularity for its potential health benefits.

North America Chocolate Market Trends

The increasing demand for artisanal chocolates, coupled with strong demand during special occasions like Christmas and Halloween, allows the chocolate market to grow

- Chocolate remains a timeless treat among North Americans. With a 44% value share in 2023, chocolate is expected to continue to be the most frequently consumed confectionery in the region. Americans consume approximately 2.8 billion pounds of chocolate every year, with 77% of Americans consuming chocolate at least once a month as of 2023.

- Packaging and flavor remain consumers' first impression of chocolate, among other attributes, which determines the likelihood of purchasing. In the United States, chocolate is the favorite candy category among most consumers (90%). This is because chocolate is the general favorite flavor of over 50% of Americans.

- The economic parameter remains the most important and crucial factor influencing consumers' chocolate-buying behavior.;= The prices of chocolates range from as low as USD 3.1/pound to USD 24/ pound. About half (47%) of Americans purchased USD 5-10 worth of chocolate a few times a month from their grocery stores in 2023.

- In North America, the consumption of chocolate is generally viewed from a health (physical and mental) perspective with a mix of opinions. While chocolate is a popular treat enjoyed by many, there are considerations regarding its health benefits and potential drawbacks.

North America Chocolate Industry Overview

The North America Chocolate Market is fairly consolidated, with the top five companies occupying 68.27%. The major players in this market are Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA and The Hershey Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Dark Chocolate

- 5.1.2 Milk and White Chocolate

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Albanese Confectionery Group Inc.

- 6.4.2 Askinosie Chocolate

- 6.4.3 Chocoladefabriken Lindt & Sprungli AG

- 6.4.4 Ezaki Glico Co. Ltd

- 6.4.5 Ferrero International SA

- 6.4.6 Guittard Chocolate Company

- 6.4.7 Lake Champlain Chocolates

- 6.4.8 Mars Incorporated

- 6.4.9 Mast Brothers & Co.

- 6.4.10 Mondelez International Inc.

- 6.4.11 Nestle SA

- 6.4.12 The Hershey Company

- 6.4.13 Theo Chocolate Inc.

- 6.4.14 Vosges Haut-Chocolat LLC

- 6.4.15 YIldIz Holding AS

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms