C5樹脂:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

C5 Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687324

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

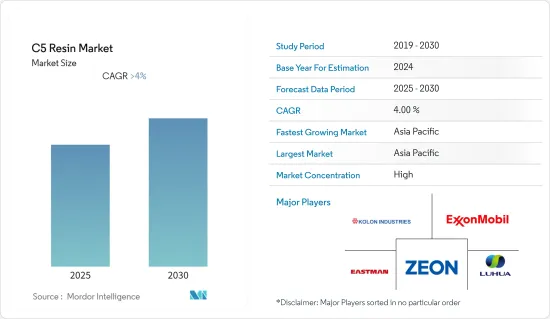

C5樹脂市場は予測期間中に4%を超えるCAGRで推移すると予想されます。

COVID-19の大流行は2021年の市場にマイナスの影響を与えました。塗料・コーティング、印刷インキ、ゴムコンパウンドなどの需要が減少しました。しかし、市場は今後数年で成長軌道を回復すると予想されます。

主なハイライト

- 短期的には、建設業界の力強い成長と包装業界からのホットメルト接着剤需要の急増が市場を牽引すると予想されます。

- 石油樹脂からロジン樹脂への置き換えが市場成長の妨げになると予想されます。

- アジア太平洋地域が市場を独占すると予想されます。最も需要が高いのは中国、次いでインドです。

C5樹脂市場の動向

接着剤・シーラント業界からの需要拡大

- 接着剤・シーラントはC5炭化水素樹脂の最大市場です。これらの樹脂は良好な接着性を持ち、ホットメルト接着剤や感圧接着剤のタックに使用されます。ほとんどのベースポリマー、ポリマー改質剤、酸化防止剤と相溶性があります。

- 自動車用接着剤は軽量で、ナットやボルト、リベット、溶接のような機械的ファスナーの強力な代替品です。この要因が、電気自動車産業からの接着剤需要を牽引しています。

- Global EV Outlookによると、2021年の世界のEV販売台数は675万台に達し、2020年比で108%の増加を記録しました。この台数には乗用車、小型トラック、小型商用車が含まれます。

- 世界の小型車販売台数に占めるEV(BEVとPHEV)のシェアは、2020年の4.2%に対して8.3%でした。BEVはEV総販売台数の71%を占め、PHEVは29%でした。2020年の世界の自動車市場は、COVID-19の影響により4.7%の成長にとどまりました。しかし現在、自動車市場は回復傾向にあります。このため、電気自動車やハイブリッド車の製造における接着剤やシーリング剤の使用が増加すると予想されます。

- 以上のような要因から、接着剤・シーラントセグメントからのC5樹脂の需要は予測期間中に伸びると予想されます。

市場を独占するアジア太平洋地域

- 世界的に見て、中国は塗料・コーティングの主要生産国です。同国はアジア太平洋で生産される塗料の半分以上を生産しており、10,000社以上の塗料会社が存在します。国内塗料市場の半分以上を地元メーカーが占めています。

- インドには現在、印刷インキ事業に従事するメーカーが550社以上あります。Huber Group、DIC India、Siegwerk、Sakata、Flint and Toyoは印刷インキ市場の大手企業であり、市場全体の約75%を占めています。

- インドの塗料業界の年間売上高は50,000カロールインドルピーと推定されています。国内最大手のAsian Paintsは国内で10の生産施設を、Berger Paintsは12の生産施設を運営しています。大手塗料メーカー4社は、インドの塗料・コーティング産業全体の生産高の60%以上を占めており、生産能力を大幅に増強しています。

- インドは、アジア太平洋地域(中国に次ぐ)で最大のゴム生産国・消費国のひとつです。天然ゴムの生産量は世界第6位で、生産能力は約90万トンです。さらに、同国の合成ゴム消費量は2025年末までに120万トンに達すると予測されています。様々な用途におけるゴム需要の高まりは、C5樹脂の生産を促進すると思われます。

- このように、アジア太平洋地域の様々な用途におけるC5樹脂の需要の増加は、予測期間中の市場を促進すると予想されます。

C5樹脂産業の概要

世界のC5樹脂市場は、上位5社で約50%を占める統合型市場です。この市場の主要企業には、Eastman Chemical Company、Kolon Industries Inc.、ExxonMobil Corporation、Zeon Corporation、Zibo Luhua Hongjin New Materialなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 包装業界からの接着剤・シーラント需要の増加

- 建設産業の拡大

- 抑制要因

- C5樹脂の代替

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 用途別

- 塗料・コーティング

- 接着剤・シーラント

- 印刷インキ

- ゴム配合

- その他の用途(紙サイズ剤、プラスチック改質剤)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Arakawa Chemical Industries Ltd

- Cray Valley

- DuPont

- Eastman Chemical Company

- Eneos Holdings Inc.

- Exxon Mobil Corporation

- Henan Anglxxon Chemical Co. Ltd

- Kolon Industries Inc.

- Lesco Chemical Limited

- Neville Chemical Company

- Puyang Ruisen Petroleum Resins Co. Ltd

- Seacon Corporation

- Shanghai Jinsen Hydrocarbon Resins Co. Limited

- Zibo Luhua Hongjin New Material Co. Ltd

- Zeon Corporation

第7章 市場機会と今後の動向

- 電気自動車市場の成長

目次

The C5 Resin Market is expected to register a CAGR of greater than 4% during the forecast period.

The COVID-19 pandemic negatively affected the market in 2021. There was a decline in the demand for paints and coatings, printing inks, rubber compounding, etc. However, the market is excepted to regain its growth trajectory in the coming years.

Key Highlights

- In the short term, the strong growth of the construction industry and rapid increase in demand for hot-melt adhesives from the packaging industry are expected to drive the market.

- The replacement of petroleum resins with rosin resins is expected to hinder the growth of the market.

- The Asia-Pacific region is expected to dominate the market. The highest demand may be from China, followed by India.

C5 Resin Market Trends

Growing Demand from Adhesives and Sealants Industry

- Adhesives and sealants are the largest markets for C5 hydrocarbon resins. These resins provide good adhesion and are used to tack in hot-melt and pressure-sensitive adhesives. They are compatible with most base polymers, polymer modifiers, and antioxidants.

- Automotive adhesives are lighter and are strong substitutes for mechanical fasteners like nuts and bolts, rivets, and welds. This factor drives the demand for adhesives from the electric vehicle industry.

- According to Global EV Outlook, EV sales worldwide reached 6.75 million units in 2021, recording an increase of 108 % compared to 2020. This volume includes passenger vehicles, light trucks, and light commercial vehicles.

- The global share of EVs (BEVs and PHEVs) in global light vehicle sales was 8.3 %, compared to 4.2 % in 2020. BEVs accounted for 71 % of the total EV sales, and PHEVs accounted for 29%. The global automotive market grew by only 4.7 % in 2020 due to the impact of COVID-19. However, currently, the automotive market is recovering. This is expected to increase the usage of adhesives and sealants in electric and hybrid vehicle manufacturing.

- Owing to the above-mentioned factors, the demand for C5 resins from the adhesives and sealants segment is expected to grow over the forecast period.

Asia-Pacific Region to Dominate the Market

- Globally, China is the leading producer of paints and coatings. The country produces more than half of all the coatings produced in Asia-Pacific and is home to over 10,000 paint companies. The local producers occupy more than half of the domestic paint market.

- India has over 550 manufacturers currently engaged in the printing inks business. Huber Group, DIC India, Siegwerk, Sakata, and Flint and Toyo are among the leading players in the printing inks market and comprise around 75% of the total market.

- The Indian paint industry is estimated to have an annual turnover of INR 50,000 crore. Asian Paints, the largest domestic player, operates ten production facilities in the country, while Berger Paints operates 12 production facilities. Four major paint producers account for more than 60% of the total output of the Indian paints and coatings industry and have added significant production capacities.

- India is one of the largest producers and consumers of rubber in the Asia-Pacific region (after China). The country is the sixth-largest producer of natural rubber globally and has a production capacity of approximately 900,000 tons. In addition, the country's consumption of synthetic rubber is projected to reach 1.2 million tons by the end of 2025. The rising demand for rubber across several applications is likely to propel the production of C5 resins.

- Thus, the growing demand for C5 resins in various applications in the Asia-Pacific region is expected to drive the market studied during the forecast period.

C5 Resin Industry Overview

The global C5 resin market is consolidated in nature, with the top five players occupying around 50%. Some of the major companies in this market include Eastman Chemical Company, Kolon Industries Inc., ExxonMobil Corporation, Zeon Corporation, and Zibo Luhua Hongjin New Material Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Adhesives and Sealants from the Packaging Industry

- 4.1.2 Expansion of the Construction Industry

- 4.2 Restraints

- 4.2.1 Replacement of C5 Resins

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Paints and Coatings

- 5.1.2 Adhesives and Sealants

- 5.1.3 Printing Inks

- 5.1.4 Rubber Compounding

- 5.1.5 Other Applications (Paper Sizing Agents, Plastic Modifiers)

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)** /Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arakawa Chemical Industries Ltd

- 6.4.2 Cray Valley

- 6.4.3 DuPont

- 6.4.4 Eastman Chemical Company

- 6.4.5 Eneos Holdings Inc.

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 Henan Anglxxon Chemical Co. Ltd

- 6.4.8 Kolon Industries Inc.

- 6.4.9 Lesco Chemical Limited

- 6.4.10 Neville Chemical Company

- 6.4.11 Puyang Ruisen Petroleum Resins Co. Ltd

- 6.4.12 Seacon Corporation

- 6.4.13 Shanghai Jinsen Hydrocarbon Resins Co. Limited

- 6.4.14 Zibo Luhua Hongjin New Material Co. Ltd

- 6.4.15 Zeon Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growth of the Electric Vehicle Market

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日