|

市場調査レポート

商品コード

1687322

カーボンコンポジット:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Carbon Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| カーボンコンポジット:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

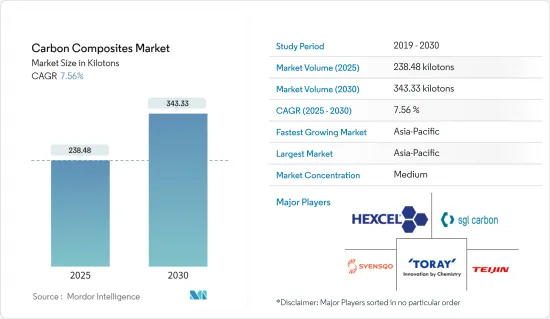

カーボンコンポジットの市場規模は、2025年に238.48キロトンと推定され、予測期間(2025~2030年)のCAGRは7.56%で、2030年には343.33キロトンに達すると予測されています。

COVID-19はカーボンコンポジット分野にマイナスの影響を与えました。世界のロックダウンと各国政府による厳しい規則により、ほとんどの生産拠点が閉鎖され、壊滅的な打撃を受けました。それでも、2021年以降事業は回復しており、今後数年で大幅な上昇が見込まれます。

主なハイライト

- 市場を牽引する主な要因は、航空宇宙・防衛産業からの需要増と風力エネルギー分野からの需要増です。

- しかし、他の複合材料に比べて製造コストが高く、代替品の存在が市場成長の妨げとなっています。

- しかしながら、3Dプリンティングにおけるカーボンコンポジットの採用拡大や燃料電池電気自動車(FCEV)の需要増加が市場機会となります。

- アジア太平洋地域が最も高い市場シェアを占めており、予測期間中は市場を独占すると予想されます。

カーボンコンポジット市場動向

航空宇宙・防衛用途が市場を席巻

- 航空宇宙・防衛分野が、主要エンドユーザーとしてカーボンコンポジット市場を独占しています。歴史的に、航空宇宙製造はアルミニウム、スチール、チタンなどの金属に依存しており、航空機の重量の約70%を占めていました。最近では、軽量化、耐性、断熱性、レーダー吸収特性により、カーボンコンポジットの使用が急増しています。

- ポリマーマトリックスに炭素繊維を入れたカーボンコンポジットは、錆や腐食に強く、メンテナンスコストを削減します。

- 優れた強度対重量比を持つこれらの素材は、航空機を軽量化し、燃料消費を抑え、より多くの乗客を乗せての長時間飛行を可能にします。

- 主な航空宇宙用途には、クリップ、クリート、ブラケット、リブ、ストラット、ストリンガー、主翼前縁、特殊部品などがあります。

- 航空宇宙分野では、主翼のトーションボックスや胴体パネルのような大型構造物への利用も検討されています。カーボン複合材料は、ミサイル防衛、地上防衛、軍用海洋用途にも使用されています。

- 例えばBoeing787ドリームライナーには、連続圧縮成形(CCM)工程で作られた複合材天井レールが採用されています。

- 航空宇宙産業は、迅速な技術の進歩と革新によって、航空機製造の急増を目の当たりにしています。Boeingの2023~2042年にかけての商業的展望では、国際交通と国内航空旅客数が回復し、大流行前の水準に戻りつつあることが強調されています。こうした要因から、ボーイングは2042年までに48,575機の新型民間ジェット機の世界需要を予測しています。

- 2023年、Boeingは528機の航空機を納入し、1,314件の新規受注を獲得しました。Boeingは、少なくとも375機の単通路機を納入するという修正目標を達成したもの、2022年には396機のナローボディ737ジェット機を納入し、当初目標の400~450機には届きませんでした。

- 一方、Airbusは、2023年に世界の87の顧客に735機の民間航空機を納入したと報告しており、前年比11%増となりました。また、Airbusの民間航空機部門は同年、2,319件の新規受注を獲得し、力強い前向きな市場展望を示しました。

- 2023年、NATO加盟31カ国は合計で1兆3,410億米ドルを支出し、世界の軍事費の55%を占めました。NATO加盟国は国内総生産(GDP)の2%の支出を目標に国防予算の増額を目指しているため、欧州の国防市場は大幅に成長すると予測されます。

- したがって、前述の要因から、航空宇宙・防衛分野が市場を独占すると予想されます。

アジア太平洋地域が市場を独占

- アジア太平洋地域は、世界のカーボンコンポジット市場で最も高いシェアを占めています。カーボンコンポジットの需要のほとんどは、航空宇宙・防衛、自動車、スポーツレジャーなどの用途によるものです。

- カーボンコンポジットは、その高い強度対重量比、耐腐食性、加工性の特徴により、自動車産業で多大な需要を目の当たりにしています。軽量でありながら強靭で、燃費の低減に貢献するという特徴から、さまざまな自動車用途で金属に取って代わりつつあります。

- 国際貿易局(ITA)によると、中国は世界第2位の民間航空宇宙市場です。Civil Aviation Administration of China(CAAC)は、航空部門は国内交通量を大流行前の約85%まで回復させる見込みであると見積もっています。

- 2023年4月、AirbusはTianjin FZ Investment Company Ltd.およびAviation Industry Corp of China Ltd.と、A320ファミリーの最終組立能力を拡大するための新たな協力協定に調印しました。この拡張には、Airbusの天津施設に2つ目の組立ラインを追加することが含まれます。この合意は、Airbusの世界生産ネットワーク全体で2026年までに月産75機を生産するという全体目標をサポートするものです。

- 中国汽車工業協会(CAAM)が発表した最新データによると、2023年の同国の自動車生産台数は3,016万台を超え、前年比11.6%増となりました。2023年に国内で販売された乗用車は3,009万台で、前年比12%増となりました。

- さらに、中国政府は2025年までに電気自動車の普及率が20%になると予測しています。このような大規模な投資は、同国の自動車セクターを推進し、市場にプラスの影響を与えると予測されます。

- 上記の要因はすべて、今後数年間のカーボンコンポジット市場を牽引すると予想されます。予測期間中、アジア太平洋が市場を独占すると予想されます。

カーボンコンポジット産業の概要

世界のカーボンコンポジット市場は、その性質上、部分的に断片化されています。主要企業(順不同)には、Toray Industries Inc.、Syensqo、Hexcel Corporation、Teijin Limited、SGL Carbon SEなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 航空宇宙・防衛産業からの需要増加

- 風力エネルギー分野からの需要増加

- 抑制要因

- 他のコンポジットに比べて高い製造コスト

- 代替品の存在

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- マトリックス別

- ハイブリッド

- 金属

- セラミック

- カーボン

- ポリマー

- 熱硬化性

- 熱可塑性

- プロセス別

- プリペグレイアッププロセス

- プルトルージョン・ワインディング

- ウェットラミネーション・インフュージョンプロセス

- プレス・射出プロセス

- その他

- 用途別

- 航空宇宙・防衛

- 自動車

- 風力タービン

- スポーツ・レジャー

- 土木工学

- 海洋

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Carbon Composites Inc.

- China Composites Group Corporation Ltd

- Epsilon Composite

- Hexcel Corporation

- Mitsubishi Chemical Corporation

- Nippon Carbon Co. Ltd

- Plasan

- Rockman

- SGL Carbon

- Syensqo

- Teijin Limited

- Toray Industries Inc.

第7章 市場機会と今後の動向

- 3Dプリンティングにおけるカーボンコンポジットの採用拡大

- 燃料電池電気自動車(FCEV)の需要増加

The Carbon Composites Market size is estimated at 238.48 kilotons in 2025, and is expected to reach 343.33 kilotons by 2030, at a CAGR of 7.56% during the forecast period (2025-2030).

COVID-19 had a negative impact on the carbon composites sector. Global lockdowns and severe rules enforced by governments resulted in a catastrophic setback as most production hubs were shut down. Nonetheless, the business has been recovering since 2021 and is expected to rise significantly in the coming years.

Key Highlights

- The major factors driving the market are increasing demand from the aerospace and defense industry and increasing demand from the wind energy sector.

- However, the high cost of manufacturing in comparison to other composites and the presence of substitutes are hindering the market growth.

- Nevertheless, the growing adoption of carbon composites in 3D printing and increasing demand from fuel cell electric vehicles (FCEVs) will be the market opportunities.

- The Asia-Pacific region accounts for the highest market share and is expected to dominate the market during the forecast period.

Carbon Composites Market Trends

Aerospace and defense applications to dominate the market

- The aerospace and defense sectors dominate the carbon composite market as its primary end-users. Historically, aerospace manufacturing relied on metals like aluminum, steel, and titanium, which made up about 70% of an aircraft's weight. Recently, the use of carbon composites has surged due to their weight reduction, resistance, insulation, and radar absorption properties.

- Carbon composites, made of carbon fibers in a polymer matrix, reduce maintenance costs by resisting rust and corrosion.

- With superior strength-to-weight ratios, these materials lighten aircraft, reducing fuel consumption and allowing longer flights with more passengers.

- Key aerospace applications include clips, cleats, brackets, ribs, struts, stringers, wing leading edges, and specialized parts.

- The aerospace sector is also exploring their use in larger structures like wing torsion boxes and fuselage panels. Carbon composites are used in missile defense, ground defense, and military marine applications.

- Industry leaders like Boeing use various carbon fiber-based composite parts in their aircraft, such as the Boeing 787 Dreamliner, which features composite ceiling rails made using continuous compression molding (CCM) processes.

- The aerospace industry is witnessing a surge in aircraft manufacturing, driven by swift technological advancements and innovations. Boeing's Commercial Outlook for 2023-2042 highlights a rebound in international traffic and domestic air travel, returning to pre-pandemic levels. Owing to these factors, Boeing forecasts global demand for 48,575 new commercial jets by 2042.

- In 2023, Boeing delivered 528 aircraft and secured 1,314 net new orders, a notable increase from 480 deliveries and 774 net new orders in 2022. While Boeing met its revised goal of delivering at least 375 single-aisle planes, it delivered 396 narrowbody 737 jets in 2022, falling short of its initial target of 400 to 450 jets.

- Airbus, on the other hand, reported delivering 735 commercial aircraft to 87 global customers in 2023, marking an 11% increase from the prior year. Airbus's "Commercial Aircraft" division also secured 2,319 gross new orders in the same year. Indicated a strong positive market outlook.

- In 2023, the 31 NATO members collectively spent USD 1,341 billion, constituting 55% of the global military expenditure. The European defense market is projected to grow substantially as NATO members have aimed to increase the defense budget by targeting spending of 2% of the Gross Domestic Product (GDP).

- Hence, due to the aforementioned factors, the aerospace and defense sector is expected to dominate the market studied.

Asia Pacific to dominate the market

- Asia-Pacific accounts for the highest share of the global carbon composites market. Most of the demand for carbon composites comes from applications in aerospace and defense, automotive, sports and leisure, etc.

- Carbon composites have been witnessing tremendous demand in the automotive industry owing to their high strength-to-weight ratios, corrosion resistivity, and workability features. They have been replacing metals in various automotive applications due to their lightweight but tough features, which contribute to lesser fuel consumption.

- According to the International Trade Administration (ITA), China is the world's second-largest civil aerospace market. The Civil Aviation Administration of China (CAAC) estimates that the aviation sector is expected to recover domestic traffic to approximately 85% of pre-pandemic levels.

- In April 2023, Airbus signed a new cooperation agreement with Tianjin FZ Investment Company Ltd. and Aviation Industry Corp of China Ltd. to expand the final assembly capacity of the A320 Family. This expansion includes adding a second assembly line at Airbus's Tianjin facility. The agreement supports Airbus's overall target of producing 75 aircraft per month by 2026 across its global production network.

- According to the latest data released by the China Association of Automobile Manufacturers (CAAM), car production in the country exceeded 30.16 million units in 2023, an 11.6% increase compared to the previous year. A total of 30.09 million passenger cars were sold in the country in 2023, a 12% increase compared to the previous year.

- Moreover, the Chinese government estimates a 20% penetration rate of electric vehicles by 2025. Such significant investments are projected to propel the country's automotive sector and positively impact the market studied.

- All the above-mentioned factors are expected to drive the market for carbon composites in the coming years. Asia-Pacific is expected to dominate the market studied during the forecast period.

Carbon Composites Industry Overview

The global carbon composites market is partially fragmented in nature. The major players (not in any particular order) include Toray Industries Inc., Syensqo, Hexcel Corporation, Teijin Limited, and SGL Carbon SE, among other companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Aerospace and Defense Industry

- 4.1.2 Increasing Demand from the Wind Energy Sector

- 4.2 Restraints

- 4.2.1 High Cost for Manufacturing in Comparison to Other Composites

- 4.2.2 Presence of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Matrix

- 5.1.1 Hybrid

- 5.1.2 Metal

- 5.1.3 Ceramics

- 5.1.4 Carbon

- 5.1.5 Polymer

- 5.1.5.1 Thermosetting

- 5.1.5.2 Thermoplastic

- 5.2 Process

- 5.2.1 Prepeg Layup Process

- 5.2.2 Pultrusion and Winding

- 5.2.3 Wet Lamination and Infusion Process

- 5.2.4 Press and Injection Processes

- 5.2.5 Other Processes

- 5.3 Application

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Wind Turbines

- 5.3.4 Sports and Leisure

- 5.3.5 Civil Engineering

- 5.3.6 Marine Applications

- 5.3.7 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Carbon Composites Inc.

- 6.4.2 China Composites Group Corporation Ltd

- 6.4.3 Epsilon Composite

- 6.4.4 Hexcel Corporation

- 6.4.5 Mitsubishi Chemical Corporation

- 6.4.6 Nippon Carbon Co. Ltd

- 6.4.7 Plasan

- 6.4.8 Rockman

- 6.4.9 SGL Carbon

- 6.4.10 Syensqo

- 6.4.11 Teijin Limited

- 6.4.12 Toray Industries Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Adoption of Carbon Composites in 3D-Printing

- 7.2 Increasing Demand from Fuel Cell Electric Vehicle (FCEV)