|

市場調査レポート

商品コード

1852056

スチレン系ブロック共重合体(SBC):市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Styrenic Block Copolymers (SBCs) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スチレン系ブロック共重合体(SBC):市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年08月13日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

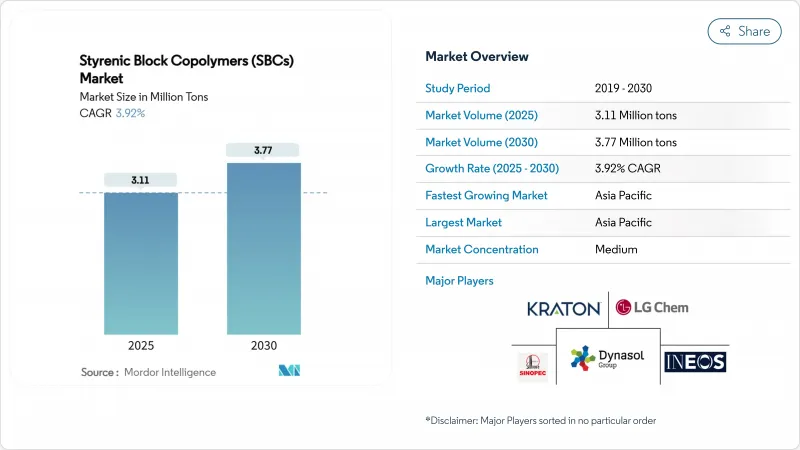

スチレン系ブロック共重合体の市場規模は2025年に311万トンと推計され、予測期間(2025~2030年)のCAGRは3.92%で、2030年には377万トンに達すると予測されます。

需要基盤は成熟しているもの、スチレン系ブロック共重合体市場は、アスファルト改質膜や防水膜から高付加価値の誘電体フィルムに至るまで、その幅広い用途から恩恵を受け続けています。多角化によって生産者は単一セクターの循環性から守られる一方、原料の統合とエンドユーザーへの地域的な近接性が競争上の優位性を左右するようになっています。アジア太平洋地域は、政府がポリマー改質アスファルトやポリマー改質メンブレンを使用する高速道路、鉄道、高層ビル建設に資本を投入しているため、依然として成長エンジンとなっています。同時に、水素添加グレードの特許切れが中堅サプライヤーに活路を開き、EV用キャパシタ向けのスルホン化ケミストリーのブレークスルーがスチレン系ブロック共重合体市場の将来のプレミアムニッチを示唆しています。

世界のスチレン系ブロック共重合体(SBC)市場の動向と洞察

アスファルト・リサイクル義務化が性能要件を後押し

EUと米国の立法機関は、道路建設基準にリサイクル含有量の最低基準を組み込んでおり、設計者は、タイヤ由来またはプラスチック由来のオイルがバージンアスファルトに取って代わられても機械的完全性を維持するポリマーシステムを好むようになっています。最近の試験で、SBS改質ミックスは、凍結融解サイクルと酸化ストレスの繰り返しの下で、改質されていないアスファルトよりも優れていることが確認されています。リサイクル原料のばらつきが配合の複雑さを増すため、スチレン系ブロック共重合体を高い不純物負荷に合わせて調整できるサプライヤーは、価格面でのプレミアムを享受しています。資金調達の仕組みは市場参入を加速させるが、地域的な回収網の格差や熱分解装置の認可サイクルの長さにより、短期的な供給は厳しいままです。その結果、スチレン系ブロック共重合体市場は、リサイクルの義務化が連邦法から自治体の調達へと連鎖する中で、トン数の増加を確保しています。

アジア太平洋地域のインフラ・ブームが防水需要を加速

中国、インド、ベトナム、インドネシアでは、記録的な公共投資が続いており、橋梁、地下鉄、集合住宅向けのポリマー改質膜の消費を刺激しています。SCGケミカルズのロンソン工場における7億米ドルの改修工事は、アスファルトや建築用メンブレンにおけるSBCの構造的需要を見込んで、総合メーカーがいかに柔軟なエタン原料に軸足を移しているかを示しています。地域の請負業者は、熱帯、砂漠、高山気候を横断する高速道路にSBS改質バインダーを指定することで、低温でのひび割れ抵抗性と高温でのわだち掘れ安定性を保証しています。建設拠点に近いため運賃が安く、納品までのリードタイムが短いという利点が、2024年のスチレン系ブロック共重合体市場におけるAPACのシェアを57%以上に押し上げます。労働力不足や許認可の遅れがプロジェクトのスケジュールを停滞させることもあるが、2030年までの生産能力増強を計画している生産者にとっては、複数年の政府予算が見通しを支えています。

コールドミックス技術が従来の用途に課題

カナダ、ドイツ、および米国のいくつかの州の政府機関は、アスファルト工場からの温室効果ガスの排出を削減する、周囲温度で硬化するエマルジョンベースのコールドミックス舗装を試験しています。初期段階の実地性能は、ポリマーを使用しないレシピが農村部や二次道路の仕様を満たすことができることを示唆しており、交通負荷が控えめな場所ではSBSの需要を侵食する可能性があります。とはいえ、交通量の多い都市部の幹線道路では、SBSによるわだち掘れ抵抗性が依然として必要とされています。導入の障壁には、請負業者の慣れ、未検証の長期耐久性、特殊乳化剤の供給制限などがあります。従って、特定のサブセグメントではコールドミックス代替材料が上昇に転じるもの、スチレン系ブロック共重合体市場は高性能舗装の中核を維持しています。

セグメント分析

スチレンーブタジエンースチレンは、2024年のスチレン系ブロック共重合体市場で72.12%の圧倒的なシェアを維持し、アスファルト、履物、感圧接着剤においてコストに見合った性能を発揮しています。このポリマーは、確立されたサプライチェーン、幅広い加工ノウハウ、配合の多様性により、大量生産用途での代替リスクを抑制しています。SEBSやSEPSのような水素添加タイプはトン数ベースでは少ないが、自動車メーカー、家電ブランド、電線・ケーブルメーカーがより高い耐熱性、耐紫外線性、耐油性の閾値を指定したため、2030年までのCAGRは最速の4.53%を記録しました。水素添加グレードのスチレン系ブロック共重合体市場規模は、特許関連ロイヤリティの崩壊と、グレード選択を加速させるクラウド対応CAEプラットフォームの商業化に後押しされ、予測期間中に約20万トン増加すると予測されます。

これと並行して、SISは溶剤型感圧接着剤、人工肛門ケア用品、医療用ドレープテープに特化した役割を維持した。メーカー各社は、ホットメルト加工時の酸化架橋を抑えるために水素添加SISを最適化し、衛生用途への適合を広げています。原料ミックスの柔軟性、特に高価格のブタジエンよりもイソプレンを選好する能力は、SISメーカーに原料変動に対するヘッジを与えています。これらの力学を総合すると、ポリマーの多様化がスチレン系ブロック共重合体市場をマクロ経済の循環性から保護すると同時に、長期的な革新ロードマップを支えることになります。

スチレン系ブロック共重合体レポートは、ポリマーの種類(スチレンーブタジエンースチレン(SBS)、スチレンーイソプレンースチレン(SIS)、水素添加SBC(HSBC))、用途(アスファルト改質、フットウェア、ポリマー改質、接着剤およびシーラント、その他)、地域(アジア太平洋、北米、欧州、南米、中東アフリカ)で区分されています。市場予測は数量(トン)で提供されます。

地域別分析

アジア太平洋地域のスチレン系ブロック共重合体市場における2024年のシェアは56.97%と圧倒的であるが、これは世界的な製造拠点としての地位とインフラストラクチャーのホットスポットとしての地位を併せ持っていることを反映しています。中国沿岸部、韓国、ASEANの製油所回廊内にある資本集約的なエチレン・プロピレンコンプレックスが競争力のある原料を供給する一方、国内の請負業者が複数年にわたる高速道路、港湾、地下鉄のプロジェクトを通じて安定した引取量を確保しています。ベトナムがエタン分解能力の改修を決定したことは、この地域の調達の柔軟性を強調するものであり、インドの急速な都市移動は防水膜の持続的需要を支えるものです。この地域の2030年までの予想CAGRは4.29%で世界平均を上回っているが、これは政策主導の工業化、エレクトロニクスの集積、自動車の電動化の加速によるもので、これらはすべて水素化SBCの普及を促進する触媒です。

北米は、州間高速道路の改修や空港滑走路の再舗装に数十億米ドルを充てる連邦政府のインフラ支出計画に支えられています。スチレン系ブロック共重合体市場は、INEOS Styrolutionが43万トンのSarnia工場を永久休止したため、国内のスチレン供給が減少しています。アスファルトのリサイクル義務化により、バインダーブレンドのポリマー濃度が高まる一方、この地域の新興エコシステムは、EVパワーエレクトロニクス向けのSBCベースの誘電体フィルムを後押ししています。しかし、シェールガス液やメキシコ湾岸のハリケーンに関連した原料の変動は、拡張計画を抑制する不確実性をもたらしています。

欧州はスチレン系ブロック共重合体市場において成熟しつつも技術的に洗練されており、持続可能性と循環性を優先しています。高いエネルギー関税と厳しい環境規制により、生産者は最適な稼働率で操業することを余儀なくされ、プラントの合理化につながるが、プロセス効率の向上も促されます。グリーンディールや拡大する生産者責任の枠組みなどの規制は、リサイクル可能なポリマーシステムやリサイクル適合ポリマーシステムへの需要を刺激し、SEBSやスルホン化SBCは食品接触用途や医療用チューブ用途で支持されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EUと米国におけるアスファルトリサイクル義務化

- APACインフラブーム(高速道路、防水材)

- パンデミックに牽引される使い捨て衛生フィルムの台頭

- クレイトンのHSBCグレードの特許切れにより新規参入が可能になる

- 次世代EVキャパシタ用スルホン化SBC

- 市場抑制要因

- 原油連鎖スチレンとブタジエン原料の変動性

- アスファルトフリーのコールドミックス道路技術

- 包装におけるSBCに代わるPOE/POPエラストマー

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- ポリマー種類別

- スチレンブタジエンースチレン(SBS)

- スチレンーイソプレンースチレン(SIS)

- 水素化SBC(HSBC)

- 用途別

- アスファルト改質(舗装と屋根材)

- フットウェア

- ポリマー改質

- 接着剤およびシーラント

- その他の用途(医療機器、電線・ケーブル)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- トルコ

- 北欧諸国

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- ナイジェリア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的な動き(M&A、JV、キャパシティ)

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- Asahi Kasei Corporation

- Avient Corporation

- Dynasol Group

- Eni S.p.A.

- INEOS

- Kraton Corporation

- Kuraray Co., Ltd.

- LCY

- LG Chem

- Sibur

- Sinopec

- TSRC

- ZEON Corporation