|

市場調査レポート

商品コード

1910455

塗料およびコーティング用樹脂:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Resins In Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 塗料およびコーティング用樹脂:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

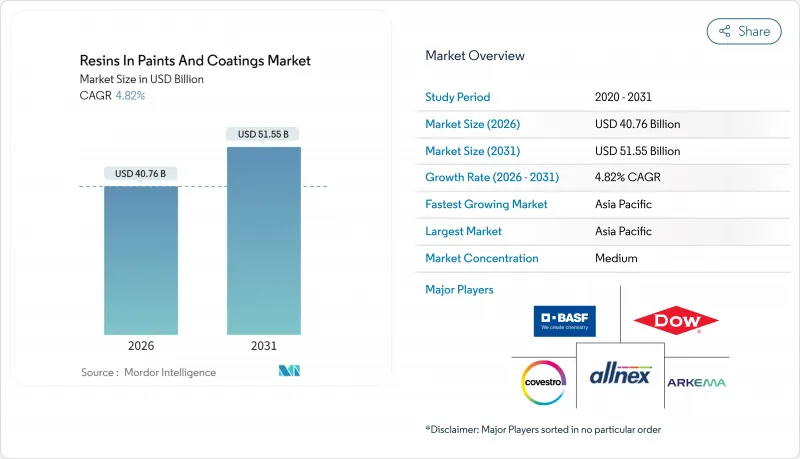

塗料およびコーティング用樹脂市場の規模は、2026年には407億6,000万米ドルと推定されており、2025年の388億9,000万米ドルから成長が見込まれます。

2031年までの予測では515億5,000万米ドルに達し、2026年から2031年にかけてCAGR4.82%で拡大する見通しです。

表面上の成長率は控えめに見えますが、政策主導による溶剤系化学物質からの移行が、調合業者に水性アクリル、ポリウレタン分散体、その他のバイオ循環技術を中心とした製品ポートフォリオの再構築を迫っています。三大陸の政府が2024年から2025年にかけて揮発性有機化合物(VOC)の上限値を強化したことで、移行スケジュールが加速しています。アジア太平洋地域はインフラ投資により、引き続き価値創造を主導しております。しかしながら、北米および欧州では、プレミアムで低VOCの樹脂を好む複数年にわたる改修プログラムが進行中です。既存企業が再生可能原料の統合、地域分散プラントの建設、製品開発サイクルを短縮するデジタル調合プラットフォームの導入を進める中、競合の激化が進んでおります。

塗料およびコーティング用樹脂の世界市場動向と洞察

アジア太平洋地域における建設ブーム

公共セクターのインフラ計画は、建築用・保護用塗料にとって依然として最大の需要源です。インドの国家インフラ計画だけでも、2025年までに累計1兆4,000億米ドルの資本支出を目標としており、エポキシ樹脂やポリウレタン樹脂を多用する橋梁・港湾・鉄道用塗料の需要を複数年にわたり牽引します。シンガポール建設庁は、2025年以降の新規公共住宅プロジェクト全てにグリーンマークプラチナ性能を義務付け、工場塗装パネルへの水性アクリルまたはポリウレタン化学品の採用を事実上要求しています。フィリピンは2024年、「Build Better More」プログラムに1兆1,000億ペソ(約200億米ドル)を配分し、工業用塗料を多用する空港、道路、エネルギー資産を含んでいます。地域全体では、国有開発事業者が低VOC仕様を入札書類に組み込む動きが加速し、分散技術の導入が進んでいます。これを受け樹脂メーカーはインドネシアとベトナムに分散反応装置の設置を発表し、リードタイム短縮と輸送時の排出量削減を目指しています。こうした動きは世界の企業の生産量のヘッジとなる一方、地域の調合メーカーが供給を現地化することを可能にします。

VOC排出規制の強化

高溶剤樹脂の適合期間は急速に縮小しています。2025年1月、米国環境保護庁(EPA)はエアゾール塗料のVOC含有量を重量比25%に制限(従来のカテゴリー上限45%から引き下げ)し、バインダー選定の即時転換を迫りました。ジョージア州はこれに続き、2025年7月施行の規則391-3-1-.02(7)(c)において、建築用フラット塗料のVOC含有量を50グラム/リットルに制限しました。欧州ではさらに基準が引き上げられ、欧州委員会が2024年10月に公表したエコラベル基準案では、内装用塗料に対し30グラム/リットルの上限を課しています。この基準を達成可能なのは、高固形分アクリル系またはハイブリッド系システムのみです。中国はGB 18582-2024規格においてEUの閾値を反映し、世界最大の建設市場がもはやVOC規制の緩い避難場所とはなり得ないことを示しました。特にアクリル系およびポリウレタン系分散液など、即座にスケールアップ可能な水性製品群を保有する樹脂サプライヤーは、配合メーカーが急激な規制強化に対応する中でシェアを拡大しています。

原料価格の変動性

プロピレン、ベンゼン、エチレンの価格変動は依然として大きな逆風です。ICISケミカルビジネスによれば、アジアの契約プロピレン価格は、3件の予期せぬクラッカー停止を受けて、2024年第2四半期に前期比25%上昇しました。欧州でも同様の逼迫によりエチレン誘導体のマージンがマイナスに転じ、中小エポキシメーカーはプラントの稼働停止を余儀なくされました。上流石油化学部門を統合していない樹脂メーカーは、価格に敏感な建築用樹脂分野において、60~90日間の価格転嫁遅延に直面しています。部分的な対策も現れており、コベストロ社は廃食用油由来のバイオ循環型ポリオールを公表。2024年までに化石原料との価格差を解消し、ナフサ価格変動への依存度を低減しました。しかしながら、バイオ原料の採用が拡大するまでは、商品価格との連動性がマージンを制限し続けるでしょう。

セグメント分析

アクリル樹脂は、低VOC水性システムへの適合性に優れることから、2025年の塗料・コーティング市場における樹脂シェアの30.02%を占めました。5.28%のCAGRと相まって、規制当局が排出上限を強化する中、価値移行の基盤を築いています。エポキシ樹脂は船舶や風力タービン産業など高応力用途に用いられ、ヘキシオン社は2024年報告書でタービンOEMからの堅調な受注を報告しています。ポリウレタン分散液はEVバッテリーの使用事例で需要を拡大。粉末塗料の主力であるポリエステルは、低温硬化型ポリエステル・エポキシハイブリッドの採用拡大により利益率の圧縮に直面しています。アルキド樹脂は、溶剤系建築用塗料の基幹として長年使用されてきましたが、乾燥時間が長くVOC(揮発性有機化合物)が高いため、主流の壁用塗料ラインでは衰退しつつあります。一方、高級木質仕上げ材ではニッチな地位を維持しています。スカンジナビア諸国では、ISO 14040に基づくライフサイクルアセスメントが公共調達で義務化され、環境宣言が認証された樹脂へのシェア移行が進んでいます。

アクリル樹脂の優れた分散性は、モジュール式住宅向け工場塗装パネルラインの基盤ともなっています。プレハブ現場では厳しいタクトタイムに対応するため、速乾性で単工程塗装が可能な塗料が好まれ、水性アクリルが自然な選択肢となっています。エポキシ樹脂ベンダーは焼成曲線を短縮するナノ改質システムで対応し、ポリウレタンベンダーは強制空気式オーブンを不要とする湿気硬化型を推進しています。塗料・コーティング市場における樹脂全般で、供給業者のイノベーションはCO2削減原料に収束しつつあります。BASFが2026年までに再生可能プロピレンをアクリルバリューチェーンに統合すると表明したことがその証左です。この原料戦略は、バイオ含有率20%以上の材料に価格プレミアムを付与する欧州公共調達規則と整合しています。

地域別分析

2025年時点で、アジア太平洋地域は塗料およびコーティング用樹脂市場の44.12%を占め、5.33%のCAGRで最も急速に成長しています。これは中国の建設業回復とインドのメガプロジェクト計画に牽引されています。中国では2024年、地方自治体が融資規制を緩和したことで住宅着工件数が回復し、融資実行額の増加につながりました。インドの国家インフラ計画は橋梁・鉄道向け保護塗料樹脂の消費を牽引し、インドネシアのIKNヌサンタラ首都圏開発やフィリピンの「Build Better More」プログラムが地域ベースライン需要を押し上げています。日本の耐震改修補助金制度や韓国のグリーンニューディール政策は公共調達における低VOC塗料を義務付け、現地加工業者経由でのアクリル・ポリウレタン分散液の使用を促進しています。

北米の成長は、2024年に4,850億米ドルに達した住宅改修支出に支えられており、省エネ外装やサイディング交換が支出の主軸となっています。米国環境保護庁(EPA)の2025年VOC規制は水性塗料の採用を加速させ、シャーウィン・ウィリアムズ社は低臭気エマルジョン塗料のプレミアム価格設定が利益率向上に寄与すると表明しています。カナダの炭素価格は2024年に1トン当たり80カナダドルに達し、冷却負荷削減のための高アルベド屋根塗料を含む改修パッケージを建物所有者に促しています。

欧州では「改修の波」と「産業排出指令」を牽引役として、低溶剤・粉末化学を優先する中程度の単一桁成長を遂げています。北欧自治体では入札時に製品固有の環境製品宣言を要求する動きが広がり、完全に監査済みの分散型製品ラインを有するサプライヤーが優位性を得ています。南米、中東・アフリカはコーティング樹脂市場規模において比較的小さなシェアを占めますが、ブラジル、サウジアラビア、アラブ首長国連邦における石油・ガス、鉱業、スタジアム建設に関連した局所的な成長が見込まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- アジア太平洋地域における建設ブーム

- 強化される(VOC)排出規制

- 2024年以降の自動車生産回復

- OECD諸国における住宅改修ブーム

- 現場での3Dプリント修理用樹脂

- 市場抑制要因

- 原料価格の変動性

- 粉末専用システムへの移行

- マイクロプラスチック段階的廃止規則

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- エポキシ樹脂

- アクリル

- ポリウレタン

- ポリエステル

- ポリプロピレン

- アルキド樹脂

- その他のタイプ

- エンドユーザー業界別

- 産業

- 建築

- 自動車

- 包装

- その他のエンドユーザー

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア/ランキング分析

- 企業プロファイル

- Allnex GmbH

- Arkema

- BASF SE

- Covestro AG

- Dow

- Evonik Industries AG

- Hexion

- Huntsman International LLC

- Kangnam Chemical

- KANSAI HELIOS

- Mitsubishi Shoji Chemical Corporation

- Mitsui Chemicals Inc.

- Olin Corporation.

- Reichhold LLC 2

- Solvay

- Synthomer plc

- Uniform Synthetics

- Vil Resins

- Wanhua