|

市場調査レポート

商品コード

1687251

石油・ガスCAPEXの展望- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Oil and Gas CAPEX Outlook - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

価格

| 石油・ガスCAPEXの展望- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 215 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

概要

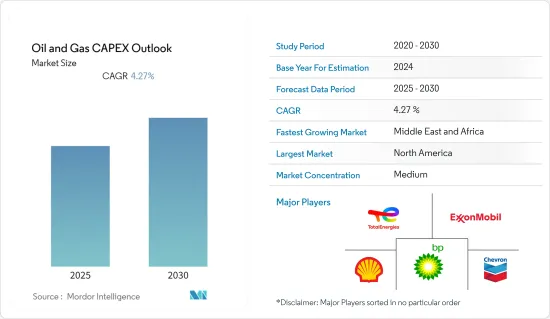

石油・ガスCAPEX市場は予測期間中にCAGR 4.27%を記録する見込み。

市場は2020年にCOVID-19の影響を受けました。現在、市場はパンデミック前のレベルに達しています。

主要ハイライト

- 中期的には、エネルギー需要の急増、陸上埋蔵量の枯渇、各国政府による海洋資源探査への取り組みに起因する、オフショア石油・ガス活動への投資の増加が、今後数年間の石油・ガス設備投資市場の成長を牽引すると予想されます。

- 他方、原油・天然ガス価格の不安定さと世界レベルでの経済成長の鈍化が、予測期間中の石油・ガス設備投資を抑制すると予想されます。

- 北海、メキシコ湾、セネガルやモーリシャスなどの新興諸国では、オフショア、深海、超深海での探鉱がいくつか行われており、資本支出を増加させる十分な機会を提供しています。

- 北米は、予測期間中、国営石油会社や新規投資とともに、世界的に統合されたメジャーの操業により、CAPEXで最も高い利益を記録しました。

石油・ガスCAPEX市場動向

上流部門が市場を独占

- 石油・ガス上流産業への投資は、COVID-19の封鎖解除に伴う石油・ガス需要の増加を受けて回復に転じています。需要の増加は2022年の原油価格を回復させました。例えば、2020年の原油価格は1バレル当たり約41.96米ドルであったが、2022年には110米ドル以上に達し、石油・ガス産業への投資が急増しました。

- 石油・ガスCAPEX市場は、プロジェクトコストの削減とポートフォリオの最適化の動向による収益性の高さ、利益率の低い油田の売却、利益率の高い成長機会への投資の重視などの要因により、大きな成長が見込まれています。

- 上流部門は最大の部門であり、CAPEXが最も高い部門となる可能性が高いです。世界の国有企業が、エネルギー安全保障を高め、海外エネルギー源への依存を減らすために、国内の石油・ガスプロジェクトを優先しているからです。

- 国際エネルギー機関(IEA)によると、世界の石油・ガス、低炭素燃料への投資は2022年に約1兆7,300億米ドルに達し、前年比6.7%以上の増加となりました。

- いくつかの石油・ガス大手は、2023年以降の資本支出を平均以上に増加させると発表しました。例えば、2022年12月、シェブロン・コーポレーションは、連結子会社に対する140億米ドル(CAPEX)と持分関連会社に対する30億米ドル(関連会社CAPEX)の2023年有機設備投資予算を発表しました。

- Chevron Corporationは、2023年に約115億米ドルの上流設備・探鉱支出予算を計画しています。上流設備投資には、パーミアン盆地での開発活動に40億米ドル以上、その他のシェールとタイト資産に約20億米ドルが含まれます。上流設備投資の20%以上がメキシコ湾プロジェクトに充てられます。

- Oil and Natural Gas Corporation(ONGC)は、2022~25年度の向こう3年間で、約38億米ドルの設備投資による探鉱活動の拡大を計画しています。探鉱費に関しては、これは過去3会計年度(2019~22年度)に費やされた25億米ドルの150%に相当します。

- したがって、原油・天然ガスの世界の旺盛な需要を満たすためには、探査・生産活動により多くの投資が必要であり、これが石油・ガス産業のCAPEXを促進しています。

市場を独占する北米

- 北米は、石油・ガス産業における設備投資の面で最大の市場の一つであり、米国がトップで、カナダ、メキシコがこれに続きます。米国は世界の主要な原油・天然ガス生産国であり、今後数年間は世界の石油需要の約60%を米国が賄うと予想されています。

- 米国はこれまでも常に最先端を走ってきたが、予測期間中もこの地域の石油・ガスCAPEX市場を独占すると予想されます。同国の石油・ガスプロジェクトは、予測期間中の北米における総投資額の約70%を占めます。同国の上流プロジェクト総数のうち、80%以上が新設プロジェクトと推定され、予測期間中は拡大プロジェクトが残りの20%を占めると予想されます。

- 米国エネルギー情報局(EIA)によると、同国の原油生産量は2021年に1,124万mbpdを記録します。2019年の原油生産量は大幅に減少しました。同年、原油生産量は1,225万mbpdと史上最高を記録しました。米国は世界のどの国よりも多くの原油を生産しています。

- 2022年2月現在、同国には、計画中または発表済みの段階にある石油化学プラントのCAPEX計画が約600億米ドルあります。これらのプロジェクトは、予測期間中、米国の下流部門における固定資産のCAPEX市場を促進すると考えられます。

- さらに、2021~2023年にかけて、カナダの大手石油・ガス事業者であるエンブリッジ社は、同国に総額160億米ドルを投資する見込みです。また、Tervitaは、2020年の3,300万米ドルに対し、2021年には約6,000万米ドルの設備投資を発表しました。したがって、CAPEXは予測期間中にさらに増加すると予想されます。

- したがって、建設中、提案中、計画中の石油・ガスプロジェクトがそれなりにあることから、石油・ガスCAPEX市場は予測期間中に大幅な成長が見込まれます。

石油・ガスCAPEX産業概要

世界の石油・ガスCAPEX市場は適度にセグメント化されています。主要参入企業(順不同)には、BP PLC、Exxon Mobil Corporation、TotalEnergies SE、Chevron Corporation、Shell PLCなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 2028年までの原油生産量と消費量の予測

- 2028年までの天然ガス生産量と消費量の予測

- 2028年までのパイプライン設置容量(キロメートル)の歴史的推移と予測

- タイトオイル、オイルサンド、深海産原油の歴史的生産量と予測(kb/dベース、2030年まで)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 天然ガス需要の増加とガスインフラの開発

- 海洋石油・ガス探査活動の増加

- 抑制要因

- よりクリーンな代替燃料の採用

- 原油価格の高い変動性

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- セクター

- 上流

- 中流

- 下流

- 所在地

- オンショア

- オフショア

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- ロシア

- ノルウェー

- オランダ

- その他の欧州

- アジア太平洋

- 中国

- インド

- マレーシア

- インドネシア

- ASEAN諸国

- その他のアジア太平洋

- 南米

- ブラジル

- ベネズエラ

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- ナイジェリア

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BP plc

- Shell plc

- Chevron Corporation

- Total Energies SE

- Exxon Mobil Corporation

- Oil and Natural Gas Corporation(ONGC)

- China National Petroleum Corporation(CNPC)

- Cairn Oil & Gas, Vertical of Vedanta Limited

- Petroleo Brasileiro SA

- Equinor ASA

第7章 市場機会と今後の動向

- 新興市場における未開発の石油・ガスの可能性

目次

Product Code: 57110

The Oil and Gas CAPEX Market is expected to register a CAGR of 4.27% during the forecast period.

The market was impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

Key Highlights

- Over the medium term, the rising investments in offshore oil & gas activities owing to the surging energy demand, depleting onshore reserves, and efforts from governments across nations to explore their offshore resources are expected to drive the growth of the oil & gas capex market in the coming years.

- On the other hand, volatile crude oil and natural gas prices, coupled with slow economic growth at a global level, are expected to restrain the oil and gas CAPEX during the forecast period.

- Nevertheless, several offshore, deep, and ultra-deepwater explorations in the North Sea, Gulf of Mexico, and developing countries such as Senegal and Mauritiana, provide ample opportunity for increased capital expenditure.

- North America has recorded the highest gains in CAPEX, owing to operations of globally integrated majors, along with national oil companies and new investments during the forecast period.

CAPEX Oil and Gas Market Trends

Upstream Sector to Dominate the Market

- Investment in the upstream oil & gas industry had started recovering after the rise in oil & gas demand amid the opening of the COVID-19 lockdowns. An increase in demand recovered crude oil prices in 2022. For instance, in 2020, crude oil prices were about USD 41.96 per barrel, and in 2022 the prices reached more than USD 110 per barrel, which resulted in a surge in investment in the oil & gas industry.

- The oil and gas CAPEX market is expected to witness significant growth owing to factors, including strong profitability due to a trend toward reducing project costs and optimizing portfolios, which has led to divesting of low-margin fields, as well as a greater emphasis on investments in higher-margin growth opportunities.

- The upstream sector is likely to be the largest segment and the one with the highest CAPEX, as several state-owned companies worldwide are prioritizing domestic oil and gas projects to increase energy security and reduce their dependence upon foreign energy sources.

- According to Internation Energy Agency (IEA), The global oil & gas, low carbon fuel investments reached around USD 1.73 trillion in 2022, representing an increase of more than 6.7% compared to the previous year's value.

- Several oil and gas majors have announced more than average increases in capital expenditures for 2023 and beyond. For instance, in December 2022, Chevron Corporation announced 2023 organic capital expenditure budgets of USD 14 billion for its consolidated subsidiaries (CAPEX) and USD 3 billion for its equity affiliates (affiliate CAPEX).

- Chevron Corporation has planned an upstream capital and exploratory expenditure budget of approximately USD 11.5 billion for 2023. The upstream capex includes more than USD 4 billion for development activities in the Permian Basin and approximately USD 2 billion for other shale and tight assets. More than 20% of the upstream capex is dedicated to Gulf of Mexico projects.

- Over the next three fiscal years, during FY 2022-25, Oil and Natural Gas Corporation (ONGC) planned to increase its exploration activity with capital expenditures of approximately USD 3.8 billion. In terms of exploration expenditures, this represents 150 percent of the USD 2.5 billion spent during the previous three fiscal years (FY 2019-22).

- Hence, to meet the strong global demand for crude oil and natural gas, more investment is required for exploration and production activities, which promulgates the CAPEX in the oil and gas industry.

North America to Dominate the Market

- North America is one of the largest markets in terms of capital expenditure in the oil and gas industry, with the United States being the leader, followed by Canada and Mexico. The United States is a major crude oil and natural gas producer in the world, and the country is expected to cover around 60% of the world's oil demand in the coming years.

- The United States has always been at the forefront in the past and is also expected to dominate the region's oil and gas CAPEX market in the forecast period. The country oil and gas projects accounts for approximately 70% of the total investments in North America during the forecast period. Of the total number of upstream projects in the country, more than 80% are estimated to be the new build while the expansion projects are expected to account for the remaining 20% during the forecast period.

- According to United States Energy Information Administration (EIA), crude oil production in the country record 11.24 million mbpd in 2021. The crude oil production declined significantly in 2019. In the same year, oil production reached the highest point in history with 12.25 million mbpd. The United States produces more oil than any other country in the world.

- As of February 2022, the country has approximately USD 60 billion of CAPEX plans for petrochemical plants that are either under planned or announced stages. The projects are likely to propel the CAPEX market for fixed assets in the downstream sector of the United States during the forecast period.

- Furthermore, in between 2021-2023, a major Canadian oil and gas operator, Enbridge, is expected to invest a total of USD 16 billion in the country. Another company Tervita announced a capital investment of around USD 60 million in 2021 compared to 33 million in 2020. Therefore, the CAPEX is further expected to increase during the forecast period.

- Therefore, with a decent number of several oil & gas projects under construction, proposal, and planning stages, the oil and gas CAPEX market is expected to witness significant growth during the forecast period.

CAPEX Oil and Gas Industry Overview

The global oil and gas CAPEX market is moderately fragmented. Some of the key players (in no particular order) include BP PLC, Exxon Mobil Corporation, TotalEnergies SE, Chevron Corporation, and Shell PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Crude Oil Production and Consumption Forecast, till 2028

- 4.4 Natural Gas Production and Consumption Forecast, till 2028

- 4.5 Installed Pipeline Historic Capacity and Forecast in Kilometers, till 2028

- 4.6 Historic and Production Forecast of Tight Oil, Oil Sands, and Crude from Deepwater in kb/d, until 2030

- 4.7 Recent Trends and Developments

- 4.8 Government Policies and Regulations

- 4.9 Market Dynamics

- 4.9.1 Drivers

- 4.9.1.1 Increasing Demand for Natural Gas and Developing Gas Infrastructure

- 4.9.1.2 Increasing Offshore Oil & Gas Exploration Activities

- 4.9.2 Restraints

- 4.9.2.1 Adoption of Cleaner Alternatives

- 4.9.2.2 High Volatility of Crude Oil Prices

- 4.9.1 Drivers

- 4.10 Supply Chain Analysis

- 4.11 Porter's Five Forces Analysis

- 4.11.1 Bargaining Power of Suppliers

- 4.11.2 Bargaining Power of Consumers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes Products and Services

- 4.11.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Russia

- 5.3.2.4 Norway

- 5.3.2.5 Netherlands

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Malaysia

- 5.3.3.4 Indonesia

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Venezuela

- 5.3.4.3 Argentina

- 5.3.4.4 Colombia

- 5.3.4.5 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates (UAE)

- 5.3.5.3 Egypt

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BP plc

- 6.3.2 Shell plc

- 6.3.3 Chevron Corporation

- 6.3.4 Total Energies SE

- 6.3.5 Exxon Mobil Corporation

- 6.3.6 Oil and Natural Gas Corporation (ONGC)

- 6.3.7 China National Petroleum Corporation (CNPC)

- 6.3.8 Cairn Oil & Gas, Vertical of Vedanta Limited

- 6.3.9 Petroleo Brasileiro SA

- 6.3.10 Equinor ASA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Untapped Oil and Gas Potential in Emerging Markets