|

市場調査レポート

商品コード

1850232

光伝達網:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Optical Transport Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 光伝達網:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月19日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

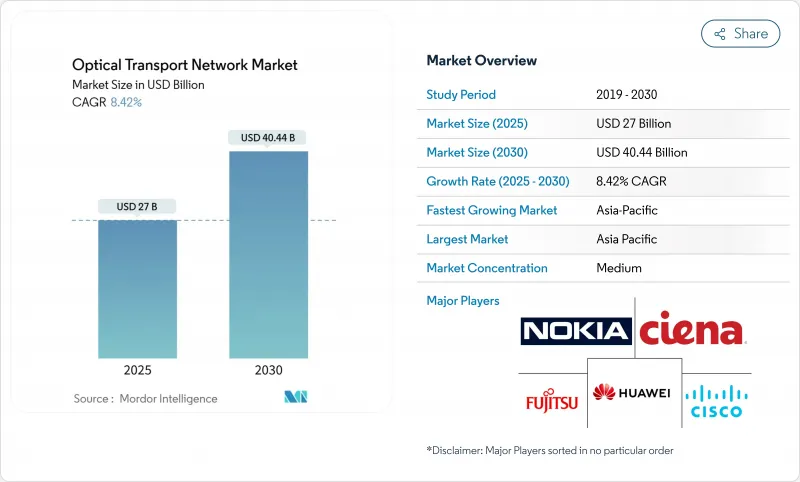

光伝達網市場の2025年の市場規模は270億米ドル、2030年には404億4,000万米ドルに達する見込みで、CAGRは8.42%です。

データセンター間インターコネクト帯域幅の増加、400ZR/ZR+コヒーレントプラグケーブルの商用化、政府資金によるファイバー導入が、この拡大を後押ししています。ハイパースケーラだけでも、2025年に2,150億米ドルをデジタルインフラに投入すると見られており、大容量DWDM(dense-wavelength-division multiplexing)システムの需要が高まっています。シリコンフォトニクスのコストカーブは、6インチリン化インジウムウエハーへの移行後に低下しており、オープンラインアーキテクチャは通信事業者の資本支出を削減しています。これらを総合すると、光伝達網市場は、人工知能クラスタ、クラウド相互接続、ブロードバンドインクルージョンに不可欠なバックボーンとして位置づけられます。

世界の光伝達網市場動向と洞察

DCI向け400ZR/ZR+の急速な普及

標準化された400ZRおよびZR+プラグケーブルの商用化により、事業者はコヒーレント光学系をルーターに直接プラグインできるようになり、スタンドアロンのトランスポンダーが不要になり、設備コストを削減できるようになりました。コヒーレントの産業用温度対応100G ZR QSFP28-DCOは、わずか5.5Wの消費電力で出荷され、エッジロケーションでのコヒーレントリンクを実現します。通信事業者はIP-光コンバージェンスによって総所有コストを20-39%削減しており、ハイパースケーラはすでにネットワーク・ファブリックを再設計し、この節約を活用しています。Cienaの1.6Tコヒーレントライトと新しい448Gb/秒PAM4オプティクスは、2030年までに予想されるDCIスループットの6倍増に応えています。短期的には、ハイパースケーラ・キャンパスクラスターがバースト的でレイテンシに敏感なトラフィックを生成する北米とアジア太平洋地域で、ほとんどの利益が実現するでしょう。

ハイパースケーラのAIクラスタトラフィックブーム

機械学習トレーニングクラスターに関連する帯域幅は、従来のワークロードよりもはるかに高速に拡張されています。AIファブリック用の光ファイバートランシーバーの収益は、2028年まで30%のペースで増加すると予測されており、非AI導入の9%ペースを上回っています。ルーメンテクノロジーズ(Lumen Technologies)は、2024年に80億米ドルの新規ファイバ契約に調印しました。これにはマイクロソフト(Microsoft)との大型受注が含まれ、AI主導の光需要規模を裏付けています。コヒレント(Coherent)の300ポート光回路スイッチとグーグルのTPUv4ポッドでの類似技術の導入は、波長選択的、再構成可能ファブリックへのアーキテクチャシフトを示しています。このドライバは、特に北米とEUのハイパースケールキャンパスの拡大に伴う中期的な成長を支えています。

ティア2通信事業者の設備投資凍結(2024~25年)

ノキアは、欧州とアジアの顧客がアップグレードを延期したため、光ネットワーク収入が23%減少したとしています。Cienaの光収入も26億4,000万米ドルに落ち込んだが、これは欧州の予算が逼迫し、ユーザ1人当たりの平均収入が低いことを反映しています。Ekinopsは、光トランスポートの売上高が41%減少したことを明らかにし、警戒感が広がっていることを強調しました。この抑制は、光導入を進めるキャッシュリッチなハイパースケーラーと、近代化を延期する従来のキャリアとの間のギャップを広げます。

セグメント分析

DWDMは、2024年の光伝達網市場で62%のシェアを維持し、長距離およびメトロ接続のバックボーンとしての地位を確認しました。事業者がAIクラスタと5Gバックホールからのトラフィックをより少ない波長に集約し、スペクトル効率を高めるため、800G対応DWDMリンクは2030年までCAGR 14.5%で成長します。

継続的なDSPの革新がこのシフトを支えています。CienaのWaveLogic 6は1波長あたり1.6Tbをプッシュし、NokiaのPSE-6は800Gの速度でリーチを拡大します。これらのブレークスルーにより、光伝達網市場はフレキシブル・グリッド・オペレーションに向けて動き続けており、一方Infineraの83.6Tbpsフィールドテストは、上限がまだ上昇していることを示しています。DWDMとパケット光機能のコンバージェンスは、今やキャリアとクラウドの両方の環境において調達の決定を導き、統合プラットフォームをデフォルトの選択肢として組み込んでいます。

日本の402Tbpsのフィールド記録が明らかにしたように、次の地平線はC+Lバンドの拡張と、これまで使われていなかった波長ウィンドウを含めることです。チャイナ・ブロードネットのファーウェイ・ベースの400G OTN展開は、高密度スイッチングの動向を強調し、C+L統合はラックあたりの容量を100Tbit/sに引き上げます。このような動きにより、光伝達網市場は、データ転送速度がチャネルあたり1Tbを超えても、将来性を維持することができます。

2024年の光伝達網市場規模の54%をコンポーネントが占め、コヒレントトランシーバ、ROADM、光回線スイッチがリードしています。標準化されたプラグケーブルの売上は、400ZR仕様に基づくマルチベンダーの相互運用性によって、2024年には6億米ドルから倍増すると予測されています。

エッジROADMユニットは、CAGR 13.2%で成長します。これは、ネットワークのディスアグリゲーションによってキャリアやハイパースケーラがアグリゲーションサイトに直接波長選択スイッチングを挿入できるようになるためです。同時に、ネットワーク設計と統合サービスは、顧客がアプリケーションレベルの要件を光パスのプロビジョニングに変換するのを支援する、インテントベースの自動化に軸足を移しています。

マネージド・ネットワーク・サービスは、機器とライフサイクル管理をバンドルした帯域アズ・ア・サービス・モデルの下で復活しつつあります。光プラットフォームコンポーネント、特に無色ー無指向性ーコンテンションレス(CDC)アーキテクチャの迅速な展開は、柔軟なスペクトル割り当てを解放しています。こうしてサービスプロバイダーは、運用モデルをボックス中心の調達から成果重視の契約へとシフトさせ、ソフトウェア・オーケストレーションを中心に社内のスキルセットを再編成します。

光伝達網市場レポートは、技術別(WDM、DWDM、その他)、製品別(サービスとコンポーネント)、エンドユーザー別(ITおよびテレコム事業者、クラウドおよびコロケーションデータセンター、ヘルスケア、その他)、用途別(長距離DWDM、メトロネットワーク、その他)、データレート/波長別(100~400Gビット/秒、400~800Gビット/秒、その他)、地域別に分類されています。

地域分析

アジア太平洋地域は2024年の売上高の35%を占め、CAGR 10.8%で拡大すると予測されます。中国当局は20以上の都市を10Gブロードバンドパイロットの対象に選定。China Mobileだけで2億7,200万ブロードバンド回線を提供しており、その3分の1がギガビット層です。日本ではNTTとインテルが政府出資の光半導体で提携し、韓国のK-Network 2030では4億8,100万米ドルが6G研究と低軌道衛星リンクに割り当てられました。ファイバーペアあたり18Tbit/sのALPHA海底ケーブルは、地域の相互接続性を強化します。

北米は成熟したインフラの上にあるが、424億5,000万米ドルのBEADプログラムがミドルマイル建設に資本を投入することで、新たな勢いを見せています。Lumenの80億米ドルのファイバー契約とZayoの40億米ドルの長距離拡張は、AI主導のエッジ・コンピュートがいかにルート需要を再構成しているかを明らかにしています。労働力不足は依然として深刻である:20万5,000人の追加技術者が必要とされ、通信事業者、ベンダー、ファイバーブロードバンド協会間のトレーニング提携に拍車をかけています。

欧州では、デジタル主権という野心的な目標と、事業者の厳しい資金繰りのバランスがとれています。欧州投資銀行によるドイチェ・グラスファーザーへの3億5,000万ユーロの融資は、農村部でのギガビット普及を目標としており、CEFデジタル計画は超大容量ネットワークに必要な2,000億ユーロの要件を概説しています。事業者のARPUは依然として低水準であるため、公的共同出資は依然として重要です。オレンジ・ポーランドの15万5,000世帯の建設は、混合金融への依存を浮き彫りにしています。英国と欧州本土を結ぶ48ペアの海底ケーブルが計画されており、特定のルートでは遅延が最大5.5ミリ秒短縮されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- DCI向け400 ZR/ZR+の急速な導入

- ハイパースケーラーAIクラスタートラフィックの急増

- 政府のファイバーバックホール刺激策(米国BEAD、EU CEF-2)

- オープンラインシステムによる設備投資の削減

- シリコンフォトニクスの価格変動

- 海底グリーンフィールドケーブル(>20 Tb/s)

- 市場抑制要因

- ティア2通信事業者の設備投資凍結(2024~25年)

- 米中によるコヒーレントDSPの輸出規制

- 光ファイバー敷設における熟練労働者の不足

- InPエピタキシーへのサプライチェーンの依存

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 技術別

- WDM

- DWDM

- Oバンドおよびその他の技術

- 提供別

- サービス

- ネットワークの保守とサポート

- ネットワーク設計と統合

- コンポーネント

- 光伝送装置

- 光スイッチ

- 光プラットフォーム/エッジROADM

- サービス

- エンドユーザー別

- ITおよび通信事業者

- クラウドおよびコロケーションデータセンター

- 政府と防衛

- ヘルスケア

- 銀行および金融サービス

- その他(公共料金、教育)

- 用途別

- 長距離DWDM

- データセンター相互接続(DCI)

- メトロネットワークス

- エンタープライズネットワーク

- データレート/波長別

- 100~400 Gbit/s

- 400~800 Gbit/s

- 800 Gbit超/s

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Nokia

- Ciena

- Cisco Systems

- Huawei

- Fujitsu

- ZTE

- Infinera

- Ericsson

- NEC

- Coriant(Infinera)

- ADVA Optical Networking

- Ribbon Communications

- Tejas Networks

- ECI Telecom(Ribbon)

- Juniper Networks

- Sterlite Technologies

- NativeWave

- Ciena-Photonera

- Padtec

- FiberHome