|

市場調査レポート

商品コード

1850229

ヘルスケアサイバーセキュリティ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Healthcare Cyber Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヘルスケアサイバーセキュリティ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

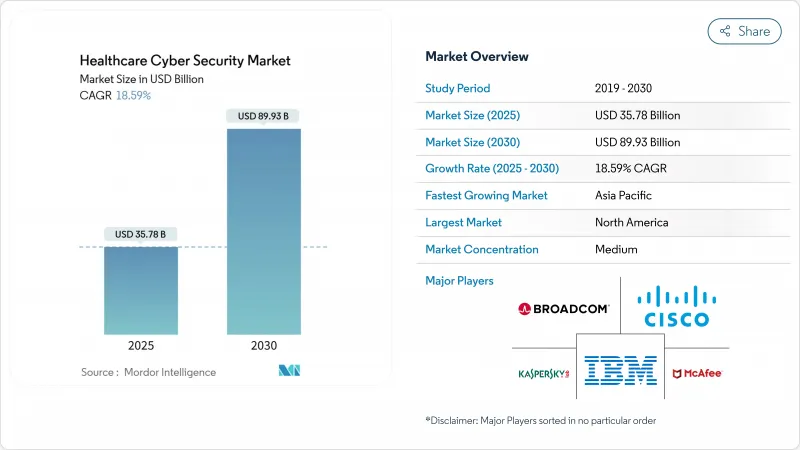

ヘルスケアのサイバーセキュリティ市場は、2025年に357億8,000万米ドルに達し、2030年には899億3,000万米ドルに拡大し、2025年から2030年にかけて18.59%のCAGRで進展すると予測されています。

支出の急増は、記録的な侵入の波から電子的に保護された医療情報を守ろうとする業界全体の奔走を反映しています。ヘルスケアプロバイダーは2024年に677件の重大な侵害を報告し、1億8,240万件の患者記録が流出しました。連邦政府の監督強化、特にすべての新しい接続医療機器に対する食品医薬品局(FDA)の第524B条の要件は、製造業者と医療提供者にライフサイクル・セキュリティ・プログラムの予算を義務付ける。機器規則と並行して、市民権局のHIPAA施行強化や保健社会福祉省の自主的なサイバーセキュリティ・パフォーマンス目標によって、取締役会はサイバーリスクを企業のトップ3の課題にまで押し上げました。政府からの資金提供は、この勢いを増幅させている:ワシントンの2025年統合サイバー予算は、民間機関に130億米ドルを計上し、その一部はレガシー・システムを近代化する病院に充てられます。同時に、米国病院協会が2024年に国家行為者が米国の施設を標的にしたという警告を発したことで、ゼロトラストのフレームワークとリアルタイム監視ソリューションの導入が加速しています。

世界のヘルスケアサイバーセキュリティ市場の動向と洞察

増加するサイバー攻撃の頻度と高度化

セキュリティ研究者は、ロシア、中国、北朝鮮、イランに関連する敵対勢力が2024年に毎日病院のインフラを調査し、推定2億5,900万件の医療記録に触れる侵害に至ったことを確認しました。医療記録は、保険金詐欺、恐喝、スパイ活動を可能にするため、不正市場で高値で取引されています。この二重の有用性が、執拗な偵察、ランサムウェア、サプライチェーン攻撃の原動力となっています。人工知能ツールは現在、スピアフィッシングや音声ディープフェイク詐欺を自動化し、ユーザーベースの防御を侵食しています。プロバイダーは、クラウドのワークロードや接続されたデバイスの継続的な監視、多要素認証、最小権限ポリシーを優先することで対応します。

規制強化とコンプライアンス負担

セクション524Bは、2023年3月以降にFDAに提出されるすべての新しい医療機器に、ソフトウェア部品表、安全な開発証明、および協調的な脆弱性開示の計画を含めることを義務付けています。市販前クリアランスを超えて、製造業者は製品の商業的寿命の間、欠陥にパッチを当てなければならないです。したがって、これらの機器を統合する病院は、ファームウェア、セキュリティ勧告、およびパッチの状況をリアルタイムで追跡できる統合リスク管理プラットフォームの予算を確保する必要があります。同時に、HHSサイバーセキュリティ・パフォーマンス目標は、不変バックアップや特権アクセス制御などの基本的なセーフガードを概説しており、多くの理事会はこれを事実上の標準として扱っています。Cybersecurity and Infrastructure Security Agencyが推奨するIdentity, Credential, and Access Managementのフレームワークは、パスワード中心のモデルをリスクベースの証明書主導の認証に置き換えるものです。

小規模医療機関における予算の制約

小規模な病院では、営業利益率が2%を下回ることが多く、レイヤード・セキュリティ・ツールや24時間365日の監視を行うための十分な資金がありません。最近の閉鎖に関する調査によると、身代金要求やダウンタイムによって流動性が損なわれると、サイバーインシデントが恒久的な閉鎖の引き金になることがあります。ヘルスケア・セクター調整協議会は、サイバーセキュリティをメディケアの許容経費に分類することを推奨しているが、払い戻し方針はまだ検討中です。持続可能な資金が出現するまでは、サブスクリプション・ベースのマネージド検知・対応サービスの採用がリスク削減の主な手段です。

セグメント分析

組織が広大な臨床エコシステム内の特権クレデンシャルの管理に重点を置いているため、2024年のヘルスケア・サイバーセキュリティ市場規模の26.2%をアイデンティティ・アクセス管理ツールが占めています。しかし、需要はセキュリティ情報・イベント管理プラットフォームに移行しつつあり、2030年までのCAGRは19.1%と予測されています。この変化は、継続的なログの相関と行動分析が、境界管理のみよりも迅速に侵害を封じ込めるというコンセンサスを反映しています。予測期間中、サイバーセキュリティのロードマップでは、単体のアンチウイルスから、SIEM、SOAR、ユーザー・エンティティ分析を統合した統合検出スタックへと予算が再配分されることが示されています。

リスク・コンプライアンス・スイートは、HIPAA、GDPR、デバイスの市販後サーベイランス監査のための文書化を合理化するため、引き続き堅調です。暗号化およびデータ損失防止モジュールは、特にプロバイダーが複数のクラウドテナント間で放射線画像や検査データを共有する必要がある場合、ゼロトラストアーキテクチャ内で支持を集めています。機械学習によって構築された新しい行動分析ソリューションは、「その他のソリューション」のバケットに位置し、精密医療のワークロードを実験している研究機関で頻繁に試験的に導入されています。

ネットワーク・セキュリティは、2024年のヘルスケア・サイバーセキュリティ市場シェアの34.3%を維持した。これは、病院が引き続き手術室、製薬オートメーション、画像保存システムを接続するVLANをセグメント化しているためです。クラウド・ワークロードへの軸足は、それにもかかわらず優先順位を再形成しています。クラウド・セキュリティ・ツールは、EHRインスタンスのハイパースケール・プロバイダーへの移行に後押しされ、CAGR 18.9%の伸びが見込まれています。

エンドポイントプロテクションは、ベッドサイドの輸液ポンプから臨床医のスマートフォンに至るまで、急増するデバイスの異機種混在に直面しています。アプリケーションのセキュリティは、社内の開発チームがサードパーティのAPIを統合した患者向けポータルを構築するにつれて上昇し、ランタイム保護とソフトウェア構成の分析が必要となります。14,000を超えるヘルスケアIPアドレスがデバイスのテレメトリを公衆インターネットに公開しているため、かつては後回しにされていた医療デバイスとIoMTのセキュリティは、今や取締役会レベルの問題になっています。

ヘルスケアサイバーセキュリティ市場は、ソリューションタイプ別(アイデンティティ・アクセス管理、リスク・コンプライアンス管理など)、セキュリティタイプ別(ネットワークセキュリティ、エンドポイントセキュリティなど)、導入形態別(オンプレミス、クラウド)、エンドユーザー別(病院、クリニックなど)、組織規模別(大企業、中小企業)、地域別に分類されます。市場予測は金額(米ドル)で提供されます。

地域別分析

北米は、世界で最も厳しいPHI規制、成熟した保険制度、一人当たりの高い医療IT予算を背景に、2024年に34.5%のヘルスケアサイバーセキュリティ市場シェアを維持。2025年の民間サイバー配分を含む連邦政府の資金援助が、電子カルテの近代化とクラウド導入を支えています。米国はまた、1億人に影響を与えた2024年のチェンジ・ヘルスケア事件という既知の最大規模の情報漏えいに見舞われ、ゼロ信頼ロードマップと第三者リスク監査が確固たるものとなりました。カナダの汎カナダ人工知能戦略とメキシコの社会セキュリティデジタル化イニシアチブは、SIEMとエンドポイント検出ツールに対する地域需要をさらに拡大します。

アジア太平洋はCAGR 19.7%で最も急成長している地域です。日本、韓国、インドでは、国家的なeヘルス義務化により、クラウドでホストされる患者レジストリと安全なIDプラットフォームが統合され、データマスキングと暗号化アズ・ア・サービスの現地での需要に拍車がかかっています。中国の「健康な中国2030」青写真では、サイバーセキュリティがスマート病院を実現する6つの柱の1つに指定され、国境を越えたデータフロー規制に対応する国内のファイアウォールや脆弱性管理ベンダーへの注文が増加しています。オーストラリアの連邦予算は、農村部の遠隔医療への補助金を柱としており、2022年から2024年にかけてデジタルヘルスの勧誘要請が92%急増します。

欧州のプライバシー中心体制は、GDPRの罰金によって取締役会レベルの説明責任が明確になるにつれて、着実な成長を保証します。ドイツは病院のデジタル化に30億ユーロを割り当て、少なくとも15%をITセキュリティ強化に充て、IDオーケストレーションと安全な電子メールゲートウェイの調達を促進します。フランスは、地域の医療機関間で脅威インテリジェンスの共有を義務付けるサイバーセキュリティの付属文書を盛り込んだeヘルス戦略「MaSante 2025」を実施します。英国のNHS「Data Saves Lives」プログラムでは、ISO 27001認証取得を条件に、レガシーなページングと画像処理プラットフォームの近代化に資金を向ける。

中東とアフリカでは、湾岸協力会議諸国がスマートシティ病院を建設し、国家サイバーセキュリティ当局のヘルスケア・セクター・コントロールへの準拠を求めており、導入が加速しています。南アフリカとケニアでは、クラウドベースの予防接種レジストリを試験的に導入しており、患者データの特定を解除するトークン化スキームも導入されています。南米では、ブラジルのオープンヘルスイニシアチブとアルゼンチンの電子処方箋展開が着実な拡大を示しており、いずれも暗号化キー管理と安全なAPIゲートウェイを必要としています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- サイバー攻撃の頻度と巧妙化の高まり

- 規制義務とコンプライアンスの負担

- クラウドベースのEHRと遠隔医療の急速な導入

- 小規模プロバイダーのセキュリティ浸透率が低い

- 価値に基づくケアモデルに結びついた医療機器のセキュリティ

- IoMT環境向けゼロトラストフレームワーク

- 市場抑制要因

- 小規模プロバイダーの予算制約

- サイバーセキュリティの専門人材の不足

- レガシーシステムの相互運用性の課題

- FDA規制対象機器のベンダー責任の曖昧さ

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 市場におけるマクロ経済要因の評価

第5章 市場規模と成長予測

- ソリューションタイプ別

- アイデンティティとアクセス管理

- リスクとコンプライアンス管理

- ウイルス対策とマルウェア対策

- セキュリティ情報およびイベント管理(SIEM)

- 侵入検知/防止(IDS/IPS)

- 暗号化とデータ損失防止

- その他の解決策

- セキュリティの種類別

- ネットワークセキュリティ

- エンドポイントセキュリティ

- アプリケーションセキュリティ

- クラウドセキュリティ

- 医療機器/IoMTセキュリティ

- 展開モード別

- オンプレミス

- クラウド

- エンドユーザー別

- 病院と診療所

- 製薬会社およびバイオテクノロジー企業

- 医療保険会社

- 診断検査室

- その他のエンドユーザー

- 企業規模別

- 大企業

- 中小企業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Cisco Systems Inc.

- IBM Corporation

- AO Kaspersky Lab

- McAfee LLC

- Broadcom Inc.(Symantec)

- Trend Micro Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies Ltd.

- Fortinet Inc.

- CrowdStrike Holdings Inc.

- FireEye Inc.(Trellix)

- Imperva Inc.

- Claroty Ltd.(Medigate)

- Cynerio Ltd.

- Sophos Group plc

- Proofpoint Inc.

- Rapid7 Inc.

- CynergisTek Inc.

- Clearwater Compliance LLC

- Sensato Cybersecurity Solutions

- SecureLink Inc.