|

市場調査レポート

商品コード

1687237

欧州のテレメディシン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Telemedicine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のテレメディシン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

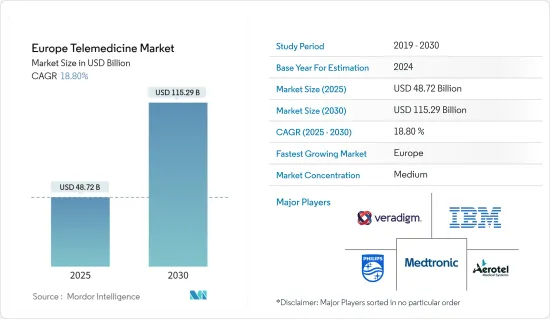

欧州のテレメディシン市場規模は2025年に487億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは18.8%で、2030年には1,152億9,000万米ドルに達すると予測されます。

欧州のテレメディシン市場は、同大陸のヘルスケア部門を変革する重要な要因に後押しされ、大幅な成長を遂げています。これらの力は、ヘルスケアの提供方法を再構築し、欧州のヘルスケアシステムにおける極めて重要な課題に対処しています。

メガ動向とマクロ促進要因:ヘルスケアのデジタル化、コスト効率の高いソリューションへのニーズ、患者中心のケアモデルへのシフトが、欧州のテレメディシン市場を牽引しています。これらの動向は、他の特定の成長促進要因と絡み合って、欧州におけるテレメディシンの拡大に拍車をかけています。

ヘルスケア費用の上昇:欧州全体でヘルスケア支出が増加していることが、テレメディシンの普及を後押ししています。政府がヘルスケア水準の向上のために支出を増やす中、費用対効果の高いソリューションへの需要が高まっています。例えば、フランス、デンマーク、オーストリア、オランダ、ノルウェーなどの国では、GDPの8~10%をヘルスケアに充てています。テレメディシンは、慢性疾患管理に関連するコストの軽減、患者の移動時間の短縮、入院期間の短縮に役立ち、高騰するヘルスケア費用に対する現実的な解決策を提供します。

技術革新:COVID-19の大流行によって加速した急速なデジタル変革は、欧州のヘルスケア提供に大きな影響を与えています。欧州連合(EU)と加盟国は、デジタルヘルスを推進するイニシアチブの先頭に立っています。例えば、EU4Healthプログラムは、ヘルスケアのデジタル進化を支援するために51億ユーロを割り当てています。一方、デジタルヘルス新興企業への投資も急増しており、欧州全域で600社を超える企業が資金提供を受けて活動しています。このイノベーションの波は、テレメディシンのアクセシビリティ、効率性、ヘルスケアシステム内での統合性を高めています。

遠隔患者モニタリングの増加:遠隔患者モニタリング(RPM)は、疾病管理を改善する貴重なツールとして台頭してきました。MicroPort CRMのBluetooth対応ペースメーカーAlizea(TM)やBorea(TM)のような製品は、RPMの成長に拍車をかけている技術的進歩の一例です。英国では、Smith+NephewとHumaが整形外科手術用のRPMサービスを開始し、術前ケアと転帰を最適化しています。こうしたイノベーションは、ケアの質を向上させるとともに、ヘルスケアシステムへの負担を軽減します。

慢性疾患の負担増:慢性疾患は欧州のヘルスケアシステムにとって大きな課題であり、テレメディシンはこの負担を軽減するソリューションを提供します。欧州では15歳以上の人口の3分の1が慢性疾患を抱えています。テレメディシンは、特に欧州で5,900万人の成人が罹患している糖尿病のような病気について、継続的なモニタリングとケアへのアクセスを容易にします。この技術は、早期診断と個別ケアを可能にし、欧州全域の慢性疾患の管理にとって貴重なものとなっています。

サマリーをまとめると、欧州のテレメディシン市場は、経済的圧力の高まり、技術の進歩、ヘルスケア需要の変化、慢性疾患負担が原動力となっています。このような力によってヘルスケアの状況が再構築される中、テレメディシンは高品質で利用しやすいヘルスケアを提供する上で重要な役割を果たし続けるでしょう。

欧州のテレメディシン市場動向

ソフトウェア:欧州のテレメディシン市場のイノベーションを牽引

セグメントの概要ソフトウェア・ソリューションは、欧州のテレメディシン市場の中核であり、デジタル・プラットフォームを通じて遠隔診察や診断を可能にします。この分野は、患者と医療者のコミュニケーションを合理化し、より広範なヘルスケアシステムに統合する能力によって、市場の約45%を占めています。

成長の原動力:ソフトウェア分野は、慢性疾患の増加や人工知能(AI)およびデータ分析の技術進歩といったメガ動向から恩恵を受ける。COVID-19の大流行をきっかけに、欧州全域で遠隔診察が大幅に増加しました。フランスでは、毎週の遠隔相談件数が2020年初頭の4万件から、パンデミックのピーク時には100万件近くに急増しました。AIを搭載したツールとリアルタイム分析がテレメディシンソフトウェアを変革し、個別化ケアと予測診断を提供しています。

競合情勢:各社が市場の覇権を争う中、幅広い機能を提供する包括的なソフトウェア・プラットフォームの開発が優先課題となっています。HealthHeroによるFernarzt.comの買収のようなコラボレーションや買収により、各社はサービスの提供を拡大しています。大手企業は、ユーザーエクスペリエンスの最適化、データセキュリティの確保、AI主導の機能の統合に注力しています。この動向が、欧州のテレメディシンソフトウェア市場の今後の成長を後押ししています。

ドイツ欧州におけるテレメディシン導入の先導役

地域のダイナミクス:ドイツは、強固なヘルスケア・インフラと先進的な医療政策に後押しされ、欧州内で急成長するテレメディシン市場として浮上しています。同市場は、ヘルスケアのデジタル化と地方におけるケアギャップへの対応に注力しているため、他の欧州諸国を上回る2桁成長が見込まれています。

マーケットカタリスト:ドイツの高齢化と慢性疾患の増加により、テレメディシンサービスの需要が高まっています。2019年のデジタルヘルスケア法(DVG)は、デジタルヘルスを主流のケアに統合する道を開いた。COVID-19危機はテレメディシンの採用をさらに加速させ、ドイツの患者と医療提供者はバーチャルケアサービスを急速に受け入れました。

競合戦略:ドイツのテレメディシン市場を狙う企業は、ローカライゼーションと厳格なヘルスケア規制への準拠に注力しています。市場参入には現地のヘルスケアプロバイダーとの協力が不可欠であり、ドイツ語のプラットフォームへの投資がユーザー参入のカギを握る。市場は、国内の新興企業と国際的なプレーヤーとの競争が激化し、イノベーションが促進され、統合が進むと予想されます。

欧州のテレメディシン産業の概要

市場の優位性:世界プレーヤーと専門企業が主要企業

欧州のテレメディシン市場は、世界なヘルスケアコングロマリットと専門のテレメディシンプロバイダーが混在しています。この適度に統合された市場では、Koninklijke Philips NV、Medtronic PLC、Teladoc Health Inc.などの大手企業が、強力な技術的専門知識、広範なヘルスケア・ポートフォリオ、豊富なリソースを背景に優位を占めています。

市場のリーダー技術革新と包括的ソリューション

主要企業は、技術革新と包括的なサービス提供へのコミットメントを通じて、他社との差別化を図っています。Koninklijke Philips NVは統合型テレメディシンプラットフォームを開発し、Medtronic PLCは慢性疾患の遠隔モニタリングを提供しています。Teladoc Health Inc.は、InTouch Technologiesの買収後、バーチャル・ケア・サービスの広範なスイートを提供しています。これらの大手企業は、遠隔心臓病学、遠隔放射線学、遠隔病理学など、複数の専門分野にまたがるテレメディシンソリューションを提供し、欧州の多様な医療ニーズに応えています。

将来の成功のための戦略統合と規制遵守

今後、テレメディシン企業はAIや機械学習技術を自社のプラットフォームに統合し、診断を強化し、個別化されたケアを提供する必要があります。既存のヘルスケア・インフラとのシームレスな統合を保証するソリューションが競争優位性を確保する可能性が高いです。GDPRなど、欧州で進化する規制の枠組みを順守することも、信頼構築とコンプライアンス維持に不可欠です。サイバーセキュリティを優先し、患者の転帰を改善しながら費用対効果を示す企業は、欧州全域で市場シェアを獲得し、政府の支援を確保する上で有利な立場にあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 遠隔患者モニタリングの増加

- 慢性疾患の負担増

- 市場抑制要因

- 法律と償還の問題

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- テレホスピタル

- テレホーム

- mヘルス(モバイルヘルス)

- コンポーネント別

- 製品別

- ハードウェア

- ソフトウェア

- その他の製品

- サービス別

- テレパソロジー

- テレカーディオロジー

- 遠隔放射線学

- 遠隔皮膚科学

- 精神医学

- その他のサービス

- 製品別

- 提供モード別

- オンプレミス

- クラウドベース

- 地域別

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

第6章 競合情勢

- 企業プロファイル

- Aerotel Medical Systems(1998)Ltd

- Veradigm LLC

- AMD Global Telemedicine

- OTH.IO

- International Business Machinery Corporation(IBM)

- Teladoc Health Inc.

- Resideo Technologies Inc.

- Koninklijke Philips NV

- Medtronic PLC

- SHL Telemedicine

第7章 市場機会と今後の動向

The Europe Telemedicine Market size is estimated at USD 48.72 billion in 2025, and is expected to reach USD 115.29 billion by 2030, at a CAGR of 18.8% during the forecast period (2025-2030).

The Europe Telemedicine Market is undergoing substantial growth, driven by critical factors transforming the healthcare sector across the continent. These forces are reshaping how healthcare is delivered and addressing pivotal challenges within European healthcare systems.

Megatrends and Macro Growth Drivers: Digital healthcare transformation, the need for cost-efficient solutions, and the shift towards patient-centered care models are driving the European Telemedicine Market. These trends are intertwined with other specific growth drivers, fueling the expansion of telemedicine in Europe.

Rising Healthcare Costs: Rising healthcare expenditures across Europe are propelling telemedicine adoption. As governments increase spending to enhance healthcare standards, there is a growing demand for cost-effective solutions. For example, countries like France, Denmark, Austria, the Netherlands, and Norway allocate 8-10% of their GDP to healthcare. Telemedicine helps mitigate costs linked to chronic disease management, reduce patient travel, and shorten hospital stays, offering a practical solution to escalating healthcare expenses.

Technological Innovations: The rapid digital transformation, accelerated by the COVID-19 pandemic, is significantly impacting healthcare delivery in Europe. The European Union and member states are spearheading initiatives to promote digital health. For instance, the EU4Health program allocates €5.1 billion to support healthcare's digital evolution. Meanwhile, investments in digital health startups are surging, with over 600 funded companies active across Europe. This innovation wave enhances telemedicine's accessibility, efficiency, and integration within healthcare systems.

Increasing Remote Patient Monitoring: Remote patient monitoring (RPM) has emerged as a valuable tool in improving disease management. Products like MicroPort CRM's Bluetooth-enabled Alizea(TM) and Borea(TM) pacemakers exemplify the technological advancements fueling RPM growth. In the UK, Smith+Nephew and Huma launched an RPM service for orthopedic surgeries, optimizing preoperative care and outcomes. These innovations improve care quality while reducing strain on healthcare systems.

Growing Burden of Chronic Diseases: Chronic diseases represent a significant challenge for healthcare systems in Europe, with telemedicine offering solutions to mitigate this burden. One-third of the European population over 15 lives with a chronic condition. Telemedicine facilitates continuous monitoring and access to care, especially for diseases like diabetes, which affects 59 million adults in Europe. The technology enables early diagnosis and personalized care, making it invaluable for managing chronic conditions across the continent.

In summary, the Europe Telemedicine Market is driven by rising economic pressures, technological advances, changing healthcare demands, and the chronic disease burden. As these forces reshape the healthcare landscape, telemedicine will continue playing a crucial role in delivering high-quality, accessible healthcare.

Europe Telemedicine Market Trends

Software: Driving Innovation in Europe's Telemedicine Market

Segment Overview: Software solutions are at the core of the European telemedicine market, enabling remote consultations and diagnoses via digital platforms. This segment accounts for roughly 45% of the market, driven by its ability to streamline patient-provider communication and integrate into broader healthcare systems.

Growth Drivers: The software segment benefits from megatrends like the rise in chronic diseases and technological advancements in artificial intelligence (AI) and data analytics. The COVID-19 pandemic triggered a significant increase in teleconsultations across Europe. In France, weekly teleconsultations skyrocketed from 40,000 in early 2020 to nearly 1 million at the pandemic's peak. AI-powered tools and real-time analytics are transforming telemedicine software, offering personalized care and predictive diagnostics.

Competitive Landscape: As companies vie for market dominance, developing comprehensive software platforms that offer broad functionality is a priority. Collaborations and acquisitions, like HealthHero's acquisition of Fernarzt.com, are enabling companies to expand their service offerings. Leading players focus on optimizing user experience, ensuring data security, and integrating AI-driven features. This trend is driving the future growth of Europe's telemedicine software market.

Germany: Spearheading Telemedicine Adoption in Europe

Regional Dynamics: Germany has emerged as a fast-growing telemedicine market within Europe, driven by robust healthcare infrastructure and progressive health policies. The market is expected to experience double-digit growth, outpacing other European countries due to Germany's focus on healthcare digitization and addressing care gaps in rural regions.

Market Catalysts: Germany's aging population and rising incidence of chronic diseases contribute to the growing demand for telemedicine services. The Digital Healthcare Act (DVG) of 2019 paved the way for integrating digital health into mainstream care. The COVID-19 crisis further accelerated telemedicine adoption, with German patients and healthcare providers rapidly embracing virtual care services.

Competitive Strategies: Companies eyeing the German telemedicine market are focusing on localization and compliance with stringent healthcare regulations. Collaborations with local healthcare providers are crucial for market entry, and investments in German-language platforms are key for user engagement. The market is expected to see increased competition between domestic startups and international players, fostering innovation and driving consolidation.

Europe Telemedicine Industry Overview

Market Dominance: Global Players and Specialized Companies Lead

The Europe Telemedicine Market is a mix of global healthcare conglomerates and specialized telemedicine providers. This moderately consolidated market sees major players like Koninklijke Philips NV, Medtronic PLC, and Teladoc Health Inc. dominate due to their strong technological expertise, broad healthcare portfolios, and significant resources.

Market Leaders: Technological Innovation and Comprehensive Solutions

Leading companies distinguish themselves through their commitment to innovation and comprehensive service offerings. Koninklijke Philips NV has developed integrated telehealth platforms, while Medtronic PLC offers remote monitoring for chronic diseases. Teladoc Health Inc., following its acquisition of InTouch Technologies, now offers an extensive suite of virtual care services. These leaders provide telemedicine solutions across multiple specialties, including telecardiology, teleradiology, and telepathology, catering to Europe's diverse healthcare needs.

Strategies for Future Success: Integration and Regulatory Compliance

Looking ahead, telemedicine companies must integrate AI and machine learning technologies into their platforms to enhance diagnostics and deliver personalized care. Solutions that ensure seamless integration with existing healthcare infrastructure will likely secure a competitive edge. Adherence to Europe's evolving regulatory frameworks, such as GDPR, is also critical for building trust and maintaining compliance. Firms that prioritize cybersecurity and demonstrate cost-effectiveness while improving patient outcomes are better positioned to capture market share and secure government support across Europe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Remote Patient Monitoring

- 4.2.2 Growing Burden of Chronic Diseases

- 4.3 Market Restraints

- 4.3.1 Legal and Reimbursement Issues

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value -USD)

- 5.1 By Type

- 5.1.1 Telehospitals

- 5.1.2 Telehomes

- 5.1.3 mHealth (Mobile Health)

- 5.2 By Component

- 5.2.1 By Products

- 5.2.1.1 Hardware

- 5.2.1.2 Software

- 5.2.1.3 Other Products

- 5.2.2 By Services

- 5.2.2.1 Telepathology

- 5.2.2.2 Telecardiology

- 5.2.2.3 Teleradiology

- 5.2.2.4 Teledermatology

- 5.2.2.5 Telepsychiatry

- 5.2.2.6 Other Services

- 5.2.1 By Products

- 5.3 By Mode of Delivery

- 5.3.1 On-premise Delivery

- 5.3.2 Cloud-based Delivery

- 5.4 Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aerotel Medical Systems (1998) Ltd

- 6.1.2 Veradigm LLC

- 6.1.3 AMD Global Telemedicine

- 6.1.4 OTH.IO

- 6.1.5 International Business Machinery Corporation (IBM)

- 6.1.6 Teladoc Health Inc.

- 6.1.7 Resideo Technologies Inc.

- 6.1.8 Koninklijke Philips NV

- 6.1.9 Medtronic PLC

- 6.1.10 SHL Telemedicine