|

市場調査レポート

商品コード

1687227

除草剤- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 除草剤- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 331 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

除草剤市場規模は2025年に433億4,000万米ドルと予測され、2030年には587億5,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは6.27%で成長します。

土壌施用が世界の除草剤市場を独占

- 雑草は、農業システムにおける収量損失と品質低下の主要因です。雑草は、光、水、養分などの資源をめぐって作物と競合します。雑草はまた、破壊的な植物病原菌や、これらの病原菌を植物から植物へと移動させる昆虫の媒介物、あるいはその両方の貯蔵庫として機能することで、作物植物に害を与えることもあります。除草剤の使用は最も効果的な雑草管理手段であり、他の雑草管理手段よりも安価で、信頼性が高く、労力と時間を節約できます。様々な大きさの草本雑草、樹木、灌木を防除するために、いくつかの除草剤散布技術を用いることができます。

- 土壌散布が世界の除草剤市場を独占し、2022年には48.4%の市場シェアを占めました。出穂前除草剤は土壌処理を通じて散布することができます。雑草の発生を早期に抑えることで、作物は作期中に力強いスタートを切ることができます。有効成分や散布時期が異なる土壌活性除草剤は、厄介な抵抗性雑草に対処し、除草剤抵抗性の発達を遅らせるのに役立ちます。

- 葉面散布は、2022年の世界の除草剤市場額の30.3%を占めました。ポスト・エマージェンス除草剤はこの方法で散布することができます。ポスト・イマージェンス除草剤が効果を発揮するには、葉の表面から移動して標的部位に到達しなければならないです。葉面散布法に続く化学的散布法は、2022年の世界の除草剤市場の19.6%を占めました。

- 農業セグメントでは、除草剤の使用は作物の生産性を最適化し、全体的な収益性を高めています。除草剤の使用量は、予測期間(2023~2029年)にCAGR 5.1%を記録すると予想されます。

雑草による作物損失の増加が除草剤需要を押し上げると予想される

- 雑草は、さまざまな作付体系における生産に対する主要な生物学的制約です。雑草による作物の収量損失は、雑草の発生時期、雑草密度、雑草タイプ、作物タイプなど、いくつかの要因に左右されます。雑草は、管理せずに放置すると100%の収量損失をもたらす可能性があります。除草剤は、世界的に雑草防除に不可欠な要素です。

- 2022年、南米は世界の除草剤市場の35.5%(金額ベース)を占めました。南米の除草剤市場は、アルゼンチン、ブラジル、チリ、その他の南米諸国を含む様々な国で成長を遂げています。これらの国々は広大な農地を持つ主要な農業生産国であるため、除草剤の使用は雑草の個体数を管理し、最適な作物収量を確保するために極めて重要です。南米の除草剤市場は、予測期間中(2023~2029年)にCAGR 5.2%を記録すると予測されています。

- 北米は、2022年の除草剤世界市場の31.6%(金額ベース)を占めました。北米は多様な気候のため、地域全体で幅広い種類の作物を栽培することができます。北米では穀物、豆類、果物、野菜、観賞用植物が栽培されています。プライムタイムの農業従事者はほとんどがモノカルチャー、つまり、非常に広い面積で主要収入源となる単一の作物を栽培することを実践しており、雑草の蔓延の増加や収量の減少につながっています。ジョングラス、バーニヤードグラス、パーマーアマランサス、プリックリーシッドがこの地域で見られる主要雑草です。

- 世界の除草剤市場は、予測期間中(2023~2029年)にCAGR 5.1%を記録すると予測されます。農作物損失の増加、農作物を保護する必要性、雑草防除に対する意識の高まり、農業製品に対する需要の高まりが市場の成長を促進しています。

世界の除草剤市場動向

雑草が異なる環境に適応し、耐性を発達させる能力が高いため、除草剤の散布率が高くなっています。

- 除草剤の1ヘクタール当たりの世界平均消費量は、過去期間中に44.4%増加し、2017年の1.8kg/haから2022年には2.6kg/haとなりました。雑草の適応性と急速な繁殖により、雑草は作物との競合が高くなり、収量ロスの増加につながるため、化学除草剤の散布を増やす必要性が前年同期比で高まっています。したがって、雑草を防除して農業生産性の低下を防ぐために、除草剤の散布を増やす必要性が高まっている

- 除草剤は、殺菌剤や殺虫剤に比べて最も使用されている化学農薬です。2022年の1ヘクタール当たりの消費量は、全地域の中で南米が5.3kgと最も多かったが、これは大豆、トウモロコシ、サトウキビといった作物の生産が盛んで、大規模な商業耕作や高密度の作付けが多いためです。集約的な農法は雑草圧を高めるため、雑草の個体数を管理し、作物の収量を効果的に守るために除草剤が必要となります。2022年の1ヘクタール当たりの平均消費量はそれぞれ1.8kgと1.7kgで、南米に北米と欧州が続きます。

- 除草剤耐性雑草の増加と蔓延は、世界中の農業従事者にとって深刻な問題となっており、これらの耐性雑草集団と闘うために除草剤の使用量の増加や複数の除草剤の散布につながっています。例えば、パーマー・アマランサスやコモン・ウォーター・ヘンプはグリホサート、ウマノスズクサやジャイアント・ブタクサは複数の除草剤に耐性があり、コキアはアセト乳酸合成酵素阻害型除草剤に耐性があります。

- 雑草がさまざまな環境に適応し、抵抗性を発達させる能力が高いなどの要因により、除草剤散布の必要性が急激に高まっています。

2,4-Dとグリホサートは、広葉雑草の選択的防除に世界的に広く使用されている除草剤です。

- メトリブジンはトリアジン系に属する除草剤です。価格は1トン当たり1万6,600米ドル。農作物におけるさまざまな雑草の防除に広く使用されています。メトリブジンは葉緑体の光化学系II(PSII)タンパク質複合体を特異的に標的とし、植物が光合成中に光エネルギーを化学エネルギーに変換する能力を阻害します。その結果、有毒な製品別が蓄積され、最終的には対象となる雑草が枯死します。

- アトラジンは、トウモロコシや稲作におけるエキノクロア、エルシン属、アマランサスビリジスなどの広葉雑草やイネ科雑草の防除に広く使用されている除草剤です。除草剤は2022年に1万3,500米ドルと評価されました。インドは世界最大のアトラジン技術輸入国であり、中国は最大の輸出国です。

- パラコートは広く使用されている除草剤で、ビピリジリウム化合物の一種に属します。パラコートは即効性があり、非選択的であるため、作物が出穂する前に雑草を防除するため、一般にプレプラント除草剤またはプリエマージェンス除草剤として使用されます。綿花、トウモロコシ、大豆、サトウキビなど幅広い作物に有効です。パラコートの2022年の価格は7,000米ドルでした。

- ペンディメタリンはジニトロアニリン系の除草剤です。農作物のさまざまな一年生草や広葉雑草の防除に広く使用されています。2022年の価格はトン当たり3,300米ドルでした。ペンディメタリンは雑草の初期発育を阻害することで、雑草の成長初期段階における作物との競合を軽減します。

- 2,4-Dとグリホサートは、広葉雑草の選択的防除に世界的に広く使用されている除草剤です。2022年の価格はそれぞれ2,300米ドル、1,100米ドルでした。

除草剤産業概要

除草剤市場はかなり統合されており、上位5社で69.12%を占めています。この市場の主要企業は、 BASF SE、Bayer AG、Corteva Agriscience、Nufarm Ltd、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- チリ

- 中国

- フランス

- ドイツ

- インド

- インドネシア

- イタリア

- 日本

- メキシコ

- ミャンマー

- オランダ

- パキスタン

- フィリピン

- ロシア

- 南アフリカ

- スペイン

- タイ

- ウクライナ

- 英国

- 米国

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- アプリケーションモード

- 化学灌漑

- 葉面散布

- 燻蒸

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 地域

- アフリカ

- 国別

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他の欧州

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米地域

- 南米

- 国別

- アルゼンチン

- ブラジル

- チリ

- その他の南米諸国

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 56812

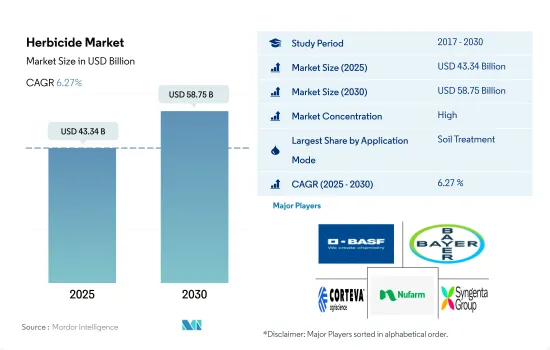

The Herbicide Market size is estimated at 43.34 billion USD in 2025, and is expected to reach 58.75 billion USD by 2030, growing at a CAGR of 6.27% during the forecast period (2025-2030).

Soil application dominates the global herbicide market

- Weeds are a major contributor to yield loss and reduced quality in an agricultural system. They compete with the crop for resources like light, water, and nutrients. Weeds can also harm crop plants by acting as reservoirs for destructive plant pathogens, the insect vectors that move these pathogens from plant to plant, or both. The use of herbicides is the most effective weed management tool, as it is cheaper, more reliable, and more labor- and time-saving than other weed control measures. Several herbicide application techniques can be used to control herbaceous weeds, trees, and bushes of various sizes.

- Soil application dominated the global herbicide market, accounting for a market share of 48.4% in 2022. Pre-emergence herbicides can be applied through soil treatment. By reducing weed pressures early on, crops can get off to a strong start during the cropping season. With different active ingredients and application timings, soil-active herbicides can help tackle troublesome resistant weeds and slow down the development of herbicide resistance.

- Foliar application accounted for 30.3% of the global herbicide market value in 2022. Post-emergence herbicides can be applied through this method. A post-emergence herbicide must move from the leaf surface and reach the target site to be effective. Following the foliar method, chemigation accounted for 19.6% of the global herbicide market in 2022.

- In the agricultural sector, herbicide usage optimizes crop productivity and enhances overall profitability. The usage of herbicides is expected to register a CAGR of 5.1% during the forecast period (2023-2029).

Rising crop losses due to the weeds are expected to boost the demand for herbicides

- Weeds are a major biotic constraint to production in different cropping systems. Yield losses in crops due to weeds depend on several factors, such as weed emergence time, weed density, type of weeds, and crop types. Weeds can result in 100% yield loss if left uncontrolled. Herbicides are an integral part of weed control globally.

- In 2022, South America accounted for a market share of 35.5%, by value, of the global herbicide market. The herbicide market in South America is experiencing growth in various countries, including Argentina, Brazil, Chile, and the rest of South American countries. As these countries are major agricultural producers with vast expanses of farmland, the use of herbicides is crucial to manage weed populations and ensure optimal crop yields. The South American herbicide market is projected to record a CAGR of 5.2% during the forecast period (2023-2029).

- North America accounted for 31.6%, by value, of the global herbicide market in 2022. North America's diverse climate allows for the cultivation of a wide range of crop types across the region. North Americans cultivate grains, legumes, fruits, vegetables, and ornamental plants. Primetime farmers mostly practice monoculture, i.e., cultivating a single crop for their primary income in a very large area, leading to an increase in weed infestation and reduced yields. Johnsongrass, barnyard grass, Palmer amaranth, and prickly sid are major weeds found in the region.

- The global herbicide market is projected to register a CAGR of 5.1% during the forecast period (2023-2029). The rising crop losses, the need to protect crops, increasing awareness of weed control, and rising demand for agriculture products are driving the market's growth.

Global Herbicide Market Trends

The high ability of weeds to adapt to different environments and develop resistance is leading to higher herbicide application rates

- The global average per-hectare consumption of herbicides increased by 44.4% during the historical period, from 1.8 kg/ha in 2017 to 2.6 kg/ha in 2022. The need for increased application of chemical herbicides is growing Y-o-Y as the adaptability and rapid reproduction of weeds make them highly competitive with crops, leading to higher yield losses. Hence, there is a growing need for more herbicide applications to control weeds and prevent reduced agricultural productivity.

- Herbicides are the most applied chemical pesticides compared to fungicides and insecticides. Among all the regions, South America had the highest per-hectare consumption in 2022, accounting for 5.3 kg, attributed to its extensive production of crops such as soybeans, corn, and sugarcane, which often involves large-scale commercial farming and high-density planting. Intensive agricultural practices contribute to higher weed pressure, necessitating herbicides to manage weed populations and protect crop yields effectively. South America was followed by North America and Europe, with an average per hectare consumption of 1.8 kg and 1.7 kg, respectively, in 2022.

- The rising prevalence and spread of herbicide-resistant weeds have become a growing issue for farmers across the globe, leading to the escalated usage of herbicides or the application of multiple herbicides to combat these resistant weed populations. For instance, palmer amaranth and common water hemp are resistant to glyphosate, horseweed and giant ragweed are resistant to multiple herbicides, and kochia is resistant to acetolactate synthase-inhibiting herbicides.

- The need for herbicide application is increasing drastically due to factors like the high ability of weeds to adapt to different environments and develop resistance.

2,4-D and glyphosate are widely used herbicides globally for selective control of broadleaf weeds

- Metribuzin is a herbicide belonging to the chemical class of triazines. It was priced at USD 16.6 thousand per metric ton. It is widely used to control various weed species in crops. Metribuzin specifically targets the photosystem II (PSII) protein complex in chloroplasts, disrupting the plants' ability to convert light energy into chemical energy during photosynthesis. This leads to the accumulation of toxic by-products and, ultimately, the death of the targeted weeds.

- Atrazine is an herbicide widely used to control broadleaf and grassy weeds like Echinochloa, Elusine spp., and Amaranthus viridis in maize and rice crops. The herbicide was valued at USD 13.5 thousand in 2022. India is the largest importer of atrazine technical worldwide, while China is the largest exporter.

- Paraquat is a widely used herbicide belonging to the chemical class of bipyridylium compounds. Due to its rapid action and non-selective nature, paraquat is commonly used as a pre-plant or pre-emergence herbicide to control weeds before crops emerge. It is effective in a wide range of crops, including cotton, corn, soybeans, and sugarcane. Paraquat was priced at USD 7.0 thousand in 2022.

- Pendimethalin is a herbicide belonging to the chemical class of dinitroanilines. It is widely used to control various annual grasses and broadleaf weeds in agricultural crops. It was priced at USD 3.3 thousand per metric ton in 2022. By disrupting early weed development, pendimethalin helps reduce weed competition with crops during their early growth stages.

- 2,4-D and glyphosate are widely used herbicides globally for selective control of broadleaf weeds. They were priced at USD 2.3 thousand and USD 1.1 thousand, respectively, in 2022.

Herbicide Industry Overview

The Herbicide Market is fairly consolidated, with the top five companies occupying 69.12%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 Chile

- 4.3.6 China

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Myanmar

- 4.3.15 Netherlands

- 4.3.16 Pakistan

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Ukraine

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms