|

市場調査レポート

商品コード

1939613

英国のペットフード:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)United Kingdom Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のペットフード:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

概要

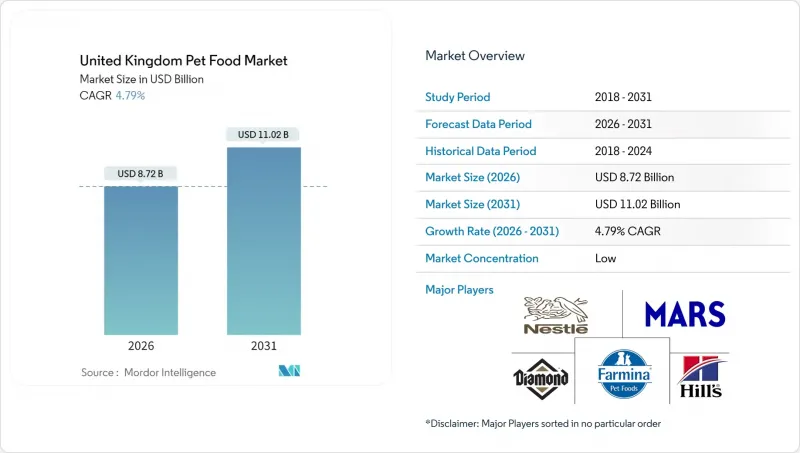

英国のペットフード市場は、2025年に83億2,000万米ドルと評価され、2026年の87億2,000万米ドルから2031年までに110億2,000万米ドルに達すると予測されております。

予測期間(2026年~2031年)におけるCAGRは4.79%と推計されております。

プレミアム志向の高まり、デジタルコマースの普及、単身世帯や高齢者世帯の増加といった人口動態の変化が市場の回復力を強化しています。企業は機能性製品のラインアップ拡充、サプライチェーンの統合、国内生産能力への投資を継続し、ブレグジット後の摩擦や為替変動の影響を相殺しています。サステナビリティへの注目が高まる中、代替タンパク質、再生原料、リサイクル可能な包装への関心が加速し、イノベーションとブランド差別化が促進されています。生活費高騰による消費抑制の影響はあるもの、飼い主がペットの健康効果を重視する傾向から、プレミアムカテゴリーは堅調に推移しております。

英国ペットフード市場の動向と洞察

ペットの人間化が進み、プレミアムフードの需要が高まっています

ペットオーナーは、人間用食品と同等のレシピ、透明性のある調達、機能性効果をますます求めるようになり、英国ペットフード市場全体の平均単価を押し上げています。オーガニック、グレインフリー、単一タンパク質、地元産ラインは、健康志向の消費者に支持されています。プレミアムブランドは、少量生産のストーリーや科学的に裏付けられた主張を活用し、価格プレミアムを正当化しています。定期購入モデルは、自動補充と個別対応の食事プラン提供により顧客維持を強化しています。原材料の品質を維持しつつ、明確な福祉基準を伝えるメーカーは、持続的な競争優位性を築いています。

単身世帯や高齢世帯における伴侶動物の飼育増加

単身世帯や退職者層が伴侶としてペットを飼育する傾向が強まっており、出生率が停滞する中でも販売数量の成長を支えています。こうした層は買い物回数を減らすため、分量調整済みパックや自動補充サービスを活用しています。高齢者は、加齢に伴うペットの関節・体重・認知機能の健康をサポートする食事を好む傾向にあり、獣医師推奨製品の需要を促進しています。都市部の単身飼主は利便性を重視するため、コンパクトな居住空間に適したイージーオープン缶や軽量パウチの展開が求められています。退職者の支出安定性は、経済的困難時におけるプレミアムカテゴリーの緩衝材となります。

生活費の圧迫により、消費者は経済的なブランドへ移行

インフレにより可処分所得が圧迫され、英国のペットフード市場では家庭内でのグレードダウンが進んでいます。スーパーマーケットが大量購入割引を交渉し、その節約分を消費者に還元するため、プライベートブランド商品のシェアが拡大しています。プレミアムブランドは価格に敏感なユーザーを維持するため、バリューラインの拡充や小型パックの導入を進めています。プレミアムからミドルクラスへの代替が進むことでキログラム当たりの収益は減速していますが、ペット飼育率の安定が全体の販売数量を支えています。おやつの購入頻度はより不定期になり、サブカテゴリー間で需要の変動が不均一化しています。

セグメント分析

2025年時点で、フードは英国ペットフード市場規模の71.62%という最大のシェアを維持し、家庭の購買サイクルの基盤であり続けています。ドライフードは利便性、価格、歯の健康効果から主流ですが、嗜好性や水分含有量を求める飼い主の間ではウェットタイプが支持を集めています。メーカーは両形態において原料リスクの分散とアレルギー懸念への対応のため、タンパク源の多様化を進めています。ペット用おやつは市場規模こそ小さいもの、訓練用・絆を深める習慣・機能性スナックとして「飼料」と「サプリメント」の境界が曖昧化する傾向から、5.55%という最も高いCAGRを記録しています。開発メーカーは関節・消化器・皮膚サポート成分を配合し、高価格帯での販売を実現しています。

治療用・強化型ソリューションへの需要拡大により、ペット用ニュートラシューティカルズ(栄養補助食品)とサプリメントが成長しています。飼い主様は獣医師の助言に基づき、オメガオイル、マルチビタミン、プロバイオティクス入りチュアブルなどを基本食に頻繁に追加し、ペット1頭あたりの平均支出を押し上げています。ペット用処方食は、臨床診断に基づく処方が必須であるため、高利益率の専門分野を占めています。販売数量は依然として限定的ですが、高齢化するペット数における肥満や慢性疾患の増加が着実な成長を支えています。治療食の英国ペットフード市場シェアは、診療所での推奨増加とECプラットフォームによる補充注文の簡素化により、拡大が見込まれます。

英国ペットフード市場レポートは、ペットフード製品別(フード、ペット用栄養補助食品/サプリメント、ペット用おやつ、ペット用医療食)、ペット別(猫、犬、その他のペット)、流通チャネル別(コンビニエンスストア、オンラインチャネル、専門店、スーパーマーケット/ハイパーマーケット、その他のチャネル)に分類されています。市場予測は金額(米ドル)および数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 レポート提供

第3章 エグゼクティブサマリー主要な調査結果

第4章 主要業界動向

- ペットの飼育数

- 猫

- 犬

- その他のペット

- ペット関連支出

- 消費者の動向

第5章 供給・生産の動向

- 貿易分析

- 原料動向

- バリューチェーン及び流通チャネル分析

- 規制の枠組み

- 市場促進要因

- ペットの人間化が進み、プレミアムフードへの需要が高まっています

- 単身世帯および高齢者世帯における伴侶動物の飼育増加

- 電子商取引の拡大による消費者直販ブランドの台頭

- 機能性成分への注力

- 昆虫やアップサイクルタンパク質を循環型経済で調達

- 獣医師推奨プログラムによる治療食の需要拡大

- 市場抑制要因

- 生活費の負担増により、消費者が低価格ブランドへ移行

- ブレグジット後の規制の相違による輸入コストの上昇

- 肉類由来のカーボンフットプリントに対する持続可能性への注目

- 小売業の統合が進み、中小ブランドの棚スペースが縮小

第6章 市場規模と成長予測(価値と数量)

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- ペット用ドライフード別

- キブル

- その他のドライペットフード

- ペット用ドライフード別

- ウェットペットフード

- ドライペットフード

- サブ製品別

- ペット用栄養補助食品/サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質およびペプチド

- ビタミン・ミネラル

- その他の栄養補助食品

- サブ製品別

- ペット用おやつ

- サブ製品別

- カリカリおやつ

- デンタルおやつ

- フリーズドライ・ジャーキーおやつ

- ソフト&チューイおやつ

- その他のおやつ

- サブ製品別

- ペット用医療食

- サブ製品別

- 皮膚用ダイエットフード

- 糖尿病

- 消化器系敏感性

- 肥満用ダイエットフード

- 口腔ケア用フード

- 腎臓用

- 尿路疾患

- その他の獣医用ダイエットフード

- サブ製品別

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他の販売チャネル

第7章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- Brand Positioning Matrix

- Market Claim Analysis

- 企業概要

- 企業プロファイル.

- Alltech Inc.

- Dechra Pharmaceuticals PLC

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- Farmina Pet Foods

- General Mills Inc.

- Mars, Incorporated

- Nestle S.A.(Purina)

- Virbac

- Vafo Praha s.r.o.

- Spectrum Brands Holdings Inc.

- Pets at Home Group plc

- IPN Holdings Ltd.

- Diamond Pet Foods(Schell and Kampeter, Inc.)