|

市場調査レポート

商品コード

1851513

保護コーティング:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Protective Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 保護コーティング:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月01日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

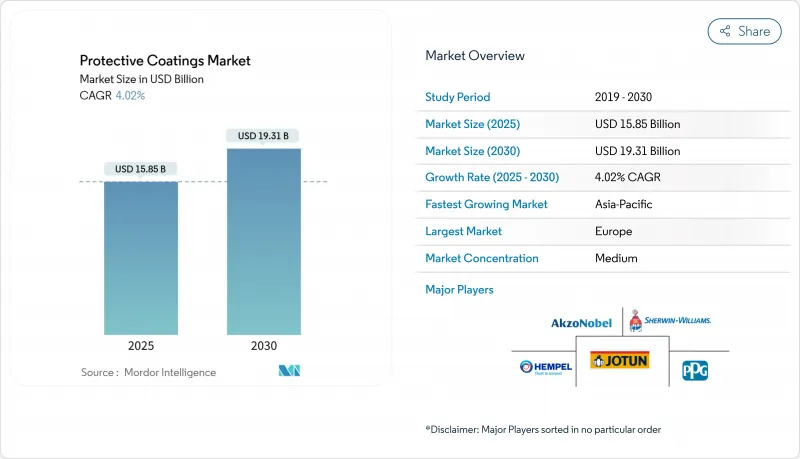

保護コーティング市場規模は2025年に158億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.02%で、2030年には193億1,000万米ドルに達すると予測されます。

厳格な環境規制と多額のインフラ支出に支えられた欧州が最大のシェアを占め、アジア太平洋は2030年までのCAGRで最速の5.23%を記録すると予測されます。インフラ整備、環境に優しい化学物質への移行、再生可能エネルギーと自動車軽量化における採用の増加が最も影響力のある成長促進要因です。ポリウレタン製品は樹脂需要をリードし、溶剤系化学物質はVOCの圧力にもかかわらず依然として優勢であり、ナノテクノロジーは自己修復とスマートサーフェスの新たな地平を切り開いています。トップ・サプライヤー間の業界再編は続いているが、新興経済国やプラスチックおよび複合基材用の先進的ソリューションには、ホワイト・スペースの機会が残っています。

世界の保護コーティング市場の動向と洞察

インフラ建設への投資の増加

保護コーティング市場を支えているのは、交通、エネルギー、市民プロジェクトへの大規模な公共投資です。米国インフラ投資・雇用促進法(Infrastructure Investment and Jobs Act)だけでも、橋や道路の修復に数十億米ドルの資金が投入され、長寿命防食システムの需要を押し上げています。中国、インド、欧州連合(EU)でも同様のプログラムが実施され、高性能の配合が好まれる耐久性の義務化が進んでいます。資産所有者は、初期費用よりもライフサイクルの経済性を重視する傾向が強まっており、メンテナンス間隔を延長したプレミアムグレードが求められています。このため、ポリウレタンやジンクリッチエポキシ系は、鋼橋や鉄筋露出コンクリートで仕様の優先度を高めています。塩分、湿度、温度サイクルが劣化を加速させる沿岸地域では、市場の恩恵はさらに大きくなります。

高まるグリーンコーティング需要

VOC排出量の上限規制は年々強化されており、特にカリフォルニア州大気資源委員会の規制値は、今や世界的な基準ベンチマークとなっています。配合メーカーは、水系、ハイソリッド系、粉体系など、従来の溶剤系製品と同等の耐食性を示す製品で対応しています。また、環境に優しい代替製品は、資産所有者が企業の持続可能性に関する誓約を達成するのに役立ちます。保護コーティング市場では、バイオベースのポリウレタン・ディスパージョンと低エネルギー・キュア・パウダー・ブレンドの急速なスケールアップが見られます。技術開発の焦点は、光沢と機械的性能を維持しながら乾燥時間を短縮する樹脂改質です。競合他社との差別化は、物理的特性だけでなく、定量化可能な環境フットプリントがますます重要になってきています。

VOC排出に関する規制

VOCの上限規制が強化されると、再製造を余儀なくされ、原材料コストの上昇を招き、生産工場の設備更新を余儀なくされます。また、法規制の遵守はエンドユーザーとの資格認定サイクルを長引かせるが、最終的には水性または粉体技術を使いこなすサプライヤーに有利となります。資産所有者がより環境に優しい規格に軸足を移し、溶剤グレードの段階的廃止による収益の減少を緩和することで、早期参入企業はシェアを獲得します。時間の経過とともに、技術革新はマージンの大半の減少を相殺し、規格に適合した生産者を優先的なパートナーとして位置づける。

セグメント分析

2024年、ポリウレタンは売上高の30.34%を占め、インフラ、自動車、エネルギー資産における比類なき柔軟性を反映しています。このセグメントは2030年までCAGR 4.79%で拡大すると予測されており、これは樹脂の中で最速です。これらの進歩により、資産所有者は高い耐摩耗性と長い外装耐久性を示すシステムに引き寄せられるため、保護コーティング市場におけるポリウレタンのシェアが上昇します。バイオベースのポリオールと湿気硬化型ポリオールの進歩は、性能を犠牲にすることなく環境プロファイルをさらに向上させる。また、弾性率のバランスと耐侵食性が重要となる洋上風力タービンのブレード先端保護材が急速に普及していることも、需要の追い風となっています。

高固形分および減水性グレードは、競争分野を再形成します。ポットライフや光沢保持性を犠牲にすることなくポリウレタンを配合できるサプライヤーは、溶剤ベースのエポキシから移行するプロジェクトでシェアを獲得しています。一方、ナノシリカとグラフェン添加剤は耐スクラッチ性と熱安定性を高め、自動車用クリアコートの魅力を高めています。その結果、ポリウレタン・セグメントは2030年までに樹脂の保護コーティング市場規模に占める割合がさらに大きくなると予想されます。

溶剤系は2024年の売上高の71.59%を占め、過酷な環境条件下での比類なき皮膜形成を反映しています。オフショアプラットフォーム、化学プラント、パイプラインのメンテナンス用塗料は、資産のダウンタイムコストが環境コンプライアンス費用に勝るため、溶剤系が主流となっています。規制の逆風にもかかわらず、溶剤系は2030年までかなりの市場規模を維持します。とはいえ、バリア性を高め、乾燥を促進する樹脂合成のブレークスルーに助けられ、水性ラインはCAGR 4.58%と最もダイナミックな軌道を描きます。粉体技術はまた、ゼロVOC認証とオーバースプレーのリサイクル可能性を活用し、加工スチール、アルミ形材、消費者向け機器の分野で足跡を伸ばしています。

地域分析

持続可能性政策と建築環境の老朽化が融合し、保護コーティングの普及を後押ししています。厳しいREACH規制が水系やハイソリッド処方の採用を後押しし、サプライヤーはより環境に優しい化学物質への投資を余儀なくされています。

アジア太平洋は、都市化と工業の拡大が続く中、最も急速に塗布量が増加しています。中国は、保護コーティングの需要を高速鉄道の軌道敷、石油化学コンビナート、巨大な造船所に向けています。また、内陸水路の橋梁をアップグレードする地方の取り組みも、改修サイクルを拡大しています。インドでは、国家インフラ・パイプライン(National Infrastructure Pipeline)がこの軌跡を反映しており、腐食防止システムのための鉄鋼やコンクリート表面積が大幅に増加しています。

北米は中間的な位置を占めているが、ハイスペック技術では極めて重要な位置を占めています。米国のインフラ・パッケージは、老朽化した州間橋、空港、淡水システムに資本を誘導しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- インフラ建設投資の増加

- 拡大するグリーンコーティング需要

- 自動車産業からの利用拡大

- 新エネルギー分野の需要拡大

- 海洋産業からの消費増加

- 市場抑制要因

- VOC排出規制

- 特定地域における熟練労働者の不足

- 変動する原材料価格

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 樹脂タイプ別

- エポキシ

- ポリウレタン

- ビニルエステル

- ポリエステル

- アルキド

- その他樹脂(アクリル、ジンクリッチ等)

- 技術別

- 溶剤系

- 水性

- パウダー

- その他の技術(ハイソリッド、UV硬化など)

- 基材別

- 金属

- コンクリート

- プラスチックと複合材料

- その他の基材(木材、ガラスなど)

- 最終用途産業別

- 石油・ガス

- パイプライン(水素パイプラインを含む)

- その他

- 鉱業

- 電力

- 風力エネルギー

- その他の発電セクター

- インフラ

- 水処理

- 配水パイプライン(飲料水および廃水排出)

- 海水淡水化と飲料水処理

- 工業用水インフラ

- その他のエンドユーザー産業(化学・石油化学,自動車,海洋)

- 石油・ガス

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 戦略的動向

- 市場シェア(%)分析

- 企業プロファイル

- Advanced Polymer Coatings

- Akzo Nobel N.V.

- Asian Paints PPG Pvt. Ltd.

- Axalta Coating Systems, LLC

- BASF

- Belzona International Ltd.

- Berger Paints India

- Chugoku Marine Paints, Ltd.

- DuluxGroup Ltd.

- Hempel A/S

- Jotun

- Kansai Paint Co.,Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- The Sherwin-Williams Company

- Tikkurila