|

市場調査レポート

商品コード

1687134

タイの肥料:市場シェア分析、産業動向、成長予測(2025年~2030年)Thailand Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイの肥料:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 109 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

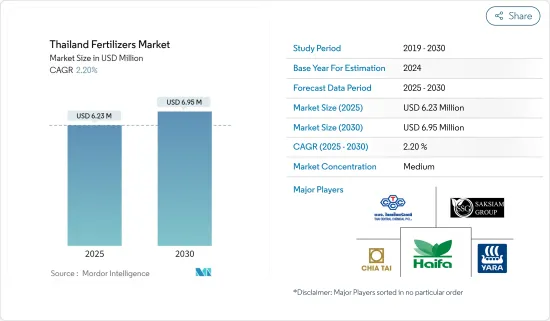

タイの肥料市場規模は2025年に623万米ドルと推定され、予測期間(2025~2030年)のCAGRは2.2%で、2030年には695万米ドルに達すると予測されています。

タイの肥料市場は、増大する食糧需要を満たすために農業生産性を向上させる必要性が高まっていることから拡大しています。とうもろこし、トウモロコシ、サトウキビ、コメなどの主要作物は大量の養分投入を必要とし、肥料需要を牽引しています。窒素肥料がタイ市場を独占しているが、これは主に窒素欠乏土壌と稲作の普及によるものです。尿素が最もよく使われる肥料です。有機栽培の面積が拡大しているにもかかわらず、農業従事者はバイオ肥料や有機肥料に関連する課題を理由に、化学合成肥料や化学肥料を好んで使用しています。

肥料補助金やソフトローンを通じた政府の支援は、市場力学に大きな影響を与えています。2024年には、従来の農業従事者手当制度に代わって、新たな肥料補助金制度が導入され、1ライ当たり29.7米ドル(20ライまたは3.2ヘクタールまで)の現金支援が行われました。政府は前年度、このプログラムに17億米ドルを割り当てました。このような支援の拡大により、今後数年間は肥料の消費が促進され、農業従事者の生産性が向上すると予想されます。

タイの肥料市場動向

農業生産性向上の必要性

タイの農業生産性は、農地面積が安定しているにもかかわらず、近年低下しています。FAOSTATのデータによると、豆類の収量は2021年の953.2kg/haから2022年には952.4kg/haに減少します。このような農業収量の減少は、肥料を含む様々な農業製品や技術の採用を増加させる可能性が高いです。

タイの東北地方は、農地保有数が最も多い地域です。この地域は、質の悪い土壌、季節による降雨量の変動、地表水の不足など、いくつかの農業課題に直面しています。これらの要因により、この地域でより高い生産性の向上を達成するためには、肥料の施用が不可欠となっています。

タイ政府は、国内の農業生産を促進するため、農業投入物に補助金を支給して農業従事者を支援してきました。例えば、政府は肥料への補助金という形で、タイの農業従事者に対する新たな刺激策を導入しました。この措置は国の福祉スマートカードを通じて実施され、カード所有者に直接補助金が支給されました。こうした政府の取り組みと農業生産増加への取り組みが相まって、予測期間中、タイにおける肥料需要を牽引すると予想されます。

窒素肥料需要の拡大

耕地面積の減少や経済における農産物輸出の重要性の高まりを背景に、タイの農業セクターにとって肥料の使用は不可欠です。

タイの土壌は、大規模な稲作が主要原因で、窒素が不足しています。そのため、窒素肥料、特に尿素が最もよく使われています。硫安(AS)は、タイでは尿素に次いで2番目に広く使われている窒素肥料です。ASは植物に不可欠な窒素(N)と硫黄(S)の栄養素を供給し、他の窒素肥料に比べて毒性(NH3水溶液)が低く、NH3の揮発による窒素の損失が少ないなど、農業的にも環境的にも利点があります。

窒素肥料は、トウモロコシ、キャッサバ、サトウキビなど、タイの主要作物に広く施用されています。尿素は広く使用されているため、依然として最も多く輸入されている肥料です。チアタイは単肥尿素市場で強い存在感を示しており、ロシアから高品質の尿素を入手できる恩恵を受けています。国際肥料協会(IFA)によると、タイの尿素消費量は2022年に92万6,000トンに達します。同国の窒素肥料需要は、より早い成長と高い収量を促進する肥料へのニーズの高まりにより、予測期間中に増加すると予測されています。

タイの肥料産業概要

タイの肥料市場は統合されており、参入企業は、Yara (Thailand) Company Limited、Haifa、Chai Thai、Thai Central Chemical Public Company Limited、Saksiam Groupです。合併や買収、提携、事業拡大、新製品の発売は、これらの積極的な市場参入企業が採用する最も一般的な事業戦略の一部です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 政府の取り組みと支援

- 農業生産性の低下と地域課題

- 食品需要の増加

- 市場抑制要因

- 気候変動と自然災害

- 有機農業へのシフト

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品

- 窒素肥料

- 尿素

- 硝酸アンモニウムカルシウム(CAN)

- 硝酸アンモニウム

- 硫酸アンモニウム

- 無水アンモニア

- その他の窒素肥料

- リン酸肥料

- リン酸一アンモニウム(MAP)

- 第二リン酸アンモニウム(DAP)

- トリプル過リン酸塩(TSP)

- その他のリン酸肥料

- カリ肥料

- 微量要素肥料

- その他

- 窒素肥料

- 用途

- 穀物・穀類

- 豆類と油糧種子

- 商業作物

- 果物・野菜

- その他

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Yara International ASA

- NFC Public Company Limited

- Chai Thai Co. Ltd

- Thai Central Chemical Public Company Limited

- Haifa Group

- SAKSIAM GROUP

- ICL Group Ltd

- Rayong Fertilizer Trading Company Limited(UBE Group)

- Grupa Azoty S.A.(Compo Expert)

- ICP FERTILIZER COMPANY

第7章 市場機会と今後の動向

The Thailand Fertilizers Market size is estimated at USD 6.23 million in 2025, and is expected to reach USD 6.95 million by 2030, at a CAGR of 2.2% during the forecast period (2025-2030).

The Thailand fertilizer market is growing due to the growing need to improve agricultural productivity to meet the growing food demand. Major crops such as corn, maize, sugarcane, and rice require substantial nutrient inputs, driving fertilizer demand. Nitrogenous fertilizers dominate the Thai market, primarily due to nitrogen-deficient soils and widespread rice cultivation. Urea is the most commonly used fertilizer. Despite an expanding area under organic cultivation, farmers prefer synthetic or chemical fertilizers due to challenges associated with biofertilizers and organic alternatives.

Government support through fertilizer subsidies and soft loans has significantly influenced market dynamics. In 2024, a new fertilizer subsidy scheme replaced the previous farmers' allowance program, which provided cash support of USD 29.7 per rai (up to 20 rai or 3.2 hectares). The government allocated USD 1.7 billion to this program in the previous year. This increased support is expected to drive fertilizer consumption and enhance farm productivity in the coming years.

Thailand Fertilizers Market Trends

Need for Increasing Agricultural Productivity

Thailand's agricultural productivity has declined in recent years, despite stable agricultural land area. FAOSTAT data indicates a decrease in pulses yield from 953.2 kg/ha in 2021 to 952.4 kg/ha in 2022. This reduction in agricultural yield is likely to increase the adoption of various agricultural products and technologies, including fertilizers.

The Northeastern region of Thailand has the largest number of farm holdings. This area faces several agricultural challenges, including poor-quality soil, seasonal rainfall variability, and scarcity of surface water. These factors have made fertilizer application essential for achieving higher productivity gains in the region.

The Thai government has supported farmers by providing subsidies on farm inputs to boost agricultural production in the country. For example, the government introduced new stimulus measures for Thai farmers in the form of subsidized fertilizers. This measure was implemented through the state welfare smartcard, providing the subsidy directly to cardholders. These government initiatives, combined with efforts to increase agricultural production, are expected to drive the demand for fertilizers in Thailand during the forecast period.

Growing Demand for Nitrogenous Fertilizers

Fertilizer usage is essential for Thailand's agricultural sector, driven by decreasing arable land and the increasing significance of agricultural exports to the economy.

Thailand's soil is predominantly nitrogen-deficient, largely due to extensive rice cultivation. As a result, nitrogenous fertilizers, particularly urea, are the most commonly used. Ammonium sulfate (AS) ranks as the second most widely used nitrogenous fertilizer in Thailand after urea. AS provides essential nitrogen (N) and sulfur (S) nutrients for plants, offering agronomic and environmental advantages such as reduced toxicity (aqueous NH3) and decreased N loss through NH3 volatilization compared to other N fertilizers.

Nitrogen fertilizers are extensively applied to major crops in Thailand, including corn, cassava, and sugarcane. Urea remains the most imported fertilizer due to its widespread use. Chia Tai has a strong presence in the single-nutrient urea market, benefiting from access to high-quality urea from Russia. According to the International Fertilizer Association (IFA), urea consumption in Thailand reached 926 thousand metric tons in 2022. The demand for nitrogen fertilizers in the country is projected to increase during the forecast period due to increasing the need for fertilizers that promote faster growth and higher yields.

Thailand Fertilizers Industry Overview

Thailand Fertilizer market is consolidated, with players such as Yara (Thailand) Company Limited, Haifa, Chai Thai Co. Ltd, Thai Central Chemical Public Company Limited, and Saksiam Group. being some of the active players in the market. Mergers and acquisitions, partnerships, expansion, and product launches are some of the most adopted business strategies by these active players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Initiatives and Support

- 4.2.2 Declining Agricultural Productivity and Regional Challenges

- 4.2.3 Rising Food Demand

- 4.3 Market Restraints

- 4.3.1 Climate Change and Natural Disasters

- 4.3.2 Shift Towards Organic Farming

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product

- 5.1.1 Nitrogenous Fertilizers

- 5.1.1.1 Urea

- 5.1.1.2 Calcium Ammonium Nitrate (CAN)

- 5.1.1.3 Ammonium Nitrate

- 5.1.1.4 Ammonium Sulfate

- 5.1.1.5 Anhydrous Ammonia

- 5.1.1.6 Other Nitrogenous Fertilizers

- 5.1.2 Phosphatic Fertilizers

- 5.1.2.1 Mono-Ammonium Phosphate (MAP)

- 5.1.2.2 Di-Ammonium Phosphate (DAP)

- 5.1.2.3 Triple Superphosphate (TSP)

- 5.1.2.4 Other Phosphatic Fertilizers

- 5.1.3 Potash Fertilizers

- 5.1.4 Micronutrient Fertilizers

- 5.1.5 Other Products

- 5.1.1 Nitrogenous Fertilizers

- 5.2 Application

- 5.2.1 Grains and Cereals

- 5.2.2 Pulses and Oilseeds

- 5.2.3 Commerical Crops

- 5.2.4 Fruits and Vegetables

- 5.2.5 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Yara International ASA

- 6.3.2 NFC Public Company Limited

- 6.3.3 Chai Thai Co. Ltd

- 6.3.4 Thai Central Chemical Public Company Limited

- 6.3.5 Haifa Group

- 6.3.6 SAKSIAM GROUP

- 6.3.7 ICL Group Ltd

- 6.3.8 Rayong Fertilizer Trading Company Limited (UBE Group)

- 6.3.9 Grupa Azoty S.A. (Compo Expert)

- 6.3.10 ICP FERTILIZER COMPANY