チョコレート:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Chocolate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 386 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687133

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

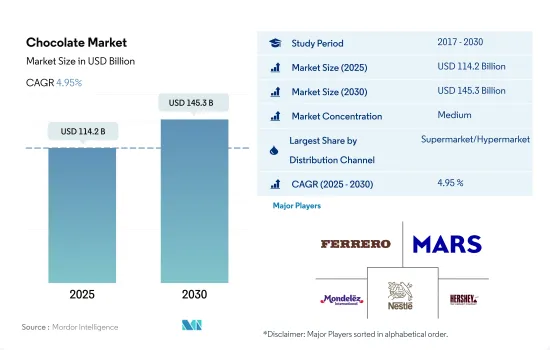

チョコレートの市場規模は2025年に1,142億米ドルと推定され、2030年には1,453億米ドルに達すると予測され、市場推計・予測期間(2025-2030年)のCAGRは4.95%です。

スーパーマーケットとハイパーマーケットは、季節のオファーや割引購入の主要な流通チャネルであり、前年比売上は着実に増加しています。

- スーパーマーケットとハイパーマーケットは、チョコレート販売の世界の主要流通チャネルです。スーパーマーケットとハイパーマーケットを通じた販売は、予測期間中にCAGR 4.67%を記録し、2030年には605億7,994万米ドルの市場規模に達すると予測されます。これらのチャネルに対する消費者の嗜好は、季節的なオファー、大量購入の割引、チョコレート製品の専用コーナーによる多様な製品へのアクセスによってもたらされます。コンビニエンスストアは棚面積が広いため、国内外のブランドを手に入れることができます。

- コンビニエンスストアは、チョコレートを購入するのにスーパーマーケット、ハイパーマーケットに次いで広く選ばれている流通チャネルです。2023年には、このセグメントの流通チャネル全体における数量シェアは30.48%に達しました。プライベート・ブランドへの幅広いリーチと容易なアクセスが、消費者が他の小売チャネルよりも伝統的な食料品店を好む原動力となっています。コンビニエンスストアを通じたチョコレートの販売額は、2023~2030年にCAGR 4.59%を記録すると予測されます。

- オンラインチャネルを通じたチョコレート菓子類の販売額は、2023~2030年のCAGRが5.72%と最も高く拡大し、2030年には93億9,362万米ドルに達すると予測されます。最大のチョコレート消費地域である欧州と北米は、2023年のオンラインチャネルを通じたチョコレート販売額で世界全体の73.47%のシェアを占めています。インターネット・ユーザーの増加は、チョコレート菓子類の購入におけるオンライン・チャネルの役割の進化に影響を与えています。2022年には、16歳から74歳の欧州の消費者の68%が、個人的な使用のためにオンラインで商品やサービスを購入しています。ASDA、Tesco、Sainsbury'sは欧州の主要オンライン食料品店です。

欧州と北米が世界のチョコレート市場をリードし、調査期間中の金額シェアはほぼ80%。

- 世界全体では、チョコレートの販売額は2022年と比較して2023年には4.42%の成長率を記録しました。チョコレートは、その様々な健康上の利点、入手のしやすさ、幅広い種類のチョコレートの入手可能性により、世界中で絶大な支持を得ています。

- 他の地域と比較して、欧州はチョコレートの販売において主要な役割を果たしており、金額ベースで2020年から2023年にかけて12.37%の成長率を記録しました。この成長は、高級チョコレートや持続可能なチョコレートに対する消費者の嗜好の高まりに起因しています。2022年の時点で、この地域の消費者の60%以上が、チョコレートを含む持続可能な方法で製造された製品に代金を支払っています。

- 欧州諸国は、一人当たりのチョコレート消費量の平均がかなり高いです。欧州は世界のカカオの35%を加工し、2022年には世界のチョコレート消費量の実に45%を消費しました。世界で最もチョコレートを消費する国は欧州にあります。スイスが最もチョコレートを消費し、2022年の一人当たり消費量は11kgでした。欧州のチョコレート市場は予測期間中にCAGR 4.41%を記録しました。

- 北米は世界第2位のチョコレート市場です。チョコレートの販売額は、2022年と比較して2027年には29.40%の成長が見込まれます。アメリカ人はチョコレートに強い親近感を抱いており、イースター、クリスマス、バレンタインデーなどのお祝い事や特別な日、大型連休に関連することが多いため、同地域のチョコレート売上を牽引しています。ホリデーシーズンには、200キロカロリー以下のパッケージサイズの選択肢が増えます。この地域のほとんどの消費者はバレンタインデーにチョコレートを贈る。2022年には、アメリカ人の27%以上がバレンタインデーにチョコレートを贈られています。

世界のチョコレート市場動向

贈答文化に支えられたチョコレートの一人当たり消費量の増加と、消費者のスイーツへの嗜好の高まりが相まって、世界中でチョコレートの需要が増加しています。

- チョコレートの消費地域は欧州がトップで、北米、アジア太平洋がこれに続きます。欧州は世界のカカオの35%を加工し、2023年には世界のチョコレート消費量の47.67%を占める。英国とスイスの一人当たりチョコレート消費量は、2023年時点でそれぞれ10.7kgと8.9kgと高いです。

- フレーバー、テクスチャー、味は、世界のチョコレート市場における消費者の購買行動に影響を与える重要な属性です。オーガニック、フェアトレード認証、レインフォレスト・アライアンス/UTZ認証といったラベルの付いたチョコレートは、欧州各国で大きな支持を集めています。アジア太平洋では、サクサク、フルーティ、ナッツのような食感のチョコレートを好む消費者が多いです。

- チョコレートの小売価格は、ミルク、カカオ豆、ココアバター、砂糖などの主要原材料価格の変動に影響されます。経済状態に基づき、消費者のチョコレートの選択は次のように分類される:スペシャリティ/プレミアム、ミドルエンド、ローエンドチョコレートがそれぞれ8~10%、18~20%、75~80%を占める。

- 世界的に、チョコレートの消費は一般的に健康的な観点からとらえられており、さまざまな意見があります。チョコレートは、特にキャンディーバー、チョコレートデザート、ホットチョコレートのような飲料の形で、人気の嗜好品として広く消費されています。

チョコレート業界の概要

チョコレート市場は適度に統合されており、上位5社で62.10%を占めています。この市場の主要企業は以下の通りです。 Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA and The Hershey Company(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子類

- ダークチョコレート

- ミルクチョコレートとホワイトチョコレート

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット/ハイパーマーケット

- その他

- 地域

- アフリカ

- 国別

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 欧州

- 国別

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- スイス

- トルコ

- 英国

- その他欧州

- 中東

- 国別

- バーレーン

- クウェート

- オマーン

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他中東

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- 国別

- アルゼンチン

- ブラジル

- その他南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Arcor S.A.I.C

- August Storck KG

- Barry callebaut AG

- Cargill Incorporated

- Chocoladefabriken Lindt & Sprungli AG

- Ferrero International SA

- ITC Limited

- Lotte Corporation

- Mars Incorporated

- Meiji Holdings Company Ltd

- Mondelez International Inc.

- Morinaga & Co. Ltd

- Nestle SA

- The Hershey Company

- YIldIz Holding AS

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 55484

The Chocolate Market size is estimated at 114.2 billion USD in 2025, and is expected to reach 145.3 billion USD by 2030, growing at a CAGR of 4.95% during the forecast period (2025-2030).

Supermarkets and hypermarkets are the leading distribution channel for seasonal offers and discounted purchases, with Y-o-Y sales increasing steadily

- Supermarkets and hypermarkets are the leading distribution channels for chocolate sales globally. Sales through supermarkets and hypermarkets are anticipated to record a CAGR of 4.67% during the forecast period to reach a market value of USD 60,579.94 million by 2030. Consumer preference for these channels is driven by seasonal offers, discounts on bulk purchases, and access to diversified products through a dedicated section of chocolate products. Due to the large shelf space, these channels allow access to local and international brands.

- Convenience stores are the second most widely preferred distribution channels after supermarkets and hypermarkets to purchase chocolates. In 2023, the segment had a 30.48% volume share in the overall distribution channels. The broader reach and easy access to private label brands drive the consumer preference for traditional grocery stores over other retail channels. The sales value of chocolates through convenience stores is anticipated to record a CAGR of 4.59% during 2023-2030.

- The sales value of chocolate confectionery through the online channel is projected to expand at the highest CAGR of 5.72% during 2023-2030, reaching USD 9,393.62 million in 2030. Being the largest chocolate-consuming regions, Europe and North America collectively had a 73.47% share of global chocolate sales through online channels in terms of value in 2023. The increasing number of internet users influences the evolving role of online channels in chocolate confectionery purchases. In 2022, 68% of European consumers aged 16 to 74 bought online goods or services for personal use. ASDA, Tesco, and Sainsbury's are leading online grocery stores in Europe.

Europe and North America lead the chocolate market globally, with a value share of almost 80% during the study period

- Globally, the sales value of chocolate registered a growth rate of 4.42% in 2023 compared to 2022. Chocolates have gained immense traction across the world due to their various health benefits, easy accessibility, and the availability of a wide range of chocolates.

- Compared to other regions, Europe plays a major role in the sales of chocolates and registered a growth rate of 12.37% from 2020 to 2023 by value. The growth is attributed to growing consumer's preference for premium chocolates and sustainable chocolates. As of 2022, more than 60% of consumers in the region paid for sustainably made products, including chocolates.

- European countries show significantly higher averages in per capita consumption of chocolates. Europe was responsible for processing 35% of the world's cacao and consumed a whopping 45% of world chocolate consumption in 2022. The world's highest chocolate consumption nations are found in Europe. Switzerland consumed the most chocolate with a per capita consumption of 11 kg in 2022. The chocolate market in Europe registered a CAGR of 4.41% during the forecast period.

- North America is the second-largest chocolate market globally. The sales value of chocolates is anticipated to grow by 29.40% in 2027 compared to 2022. Americans have a strong affinity for chocolate, and it is often associated with celebrations, special occasions, and major holidays like Easter, Christmas, and Valentine's Day, driving chocolate sales in the region. More options in package sizes of 200 calories or less are available during the holiday season. Most consumers in the region gift chocolates on Valentine's Day. In 2022, more than 27% of Americans were gifted chocolate on Valentine's Day.

Global Chocolate Market Trends

The rising per capita consumption of chocolates supported by the gifting culture, coupled with growing indulgence in sweets among consumers, increases the demand for chocolates across the globe

- Europe is the leading chocolate-consuming region, followed by North America and Asia-Pacific. Europe processed 35% of the world's cacao and accounted for 47.67% of world chocolate consumption in 2023. The UK and Switzerland recorded high per capita chocolate consumption of 10.7 kg and 8.9 kg, respectively, as of 2023

- Flavors, texture, and taste are key attributes that influence consumer buying behavior in the global chocolate market. Chocolates with labels such as organic, Fairtrade-certified, and Rainforest Alliance/UTZ-certified are gaining significant traction across European countries. In Asia-Pacific, consumers have a strong preference for textural chocolates, such as crunchy, fruity, and nutty variants.

- Retail prices of chocolates are influenced by the fluctuations in prices of key raw materials, including milk, cocoa beans, cocoa butter, and sugar. Based on economic status, consumers' chocolate choices are categorized as follows: specialty/premium, middle-end, and low-end chocolates constituting 8-10%, 18-20%, and 75-80%, respectively.

- Globally, the consumption of chocolate is generally viewed from a health perspective with a mix of opinions. Chocolate is widely consumed as a popular indulgence, particularly in the form of candy bars, chocolate desserts, and beverages like hot chocolate.

Chocolate Industry Overview

The Chocolate Market is moderately consolidated, with the top five companies occupying 62.10%. The major players in this market are Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA and The Hershey Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Dark Chocolate

- 5.1.2 Milk and White Chocolate

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Nigeria

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Malaysia

- 5.3.2.1.7 New Zealand

- 5.3.2.1.8 South Korea

- 5.3.2.1.9 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 Belgium

- 5.3.3.1.2 France

- 5.3.3.1.3 Germany

- 5.3.3.1.4 Italy

- 5.3.3.1.5 Netherlands

- 5.3.3.1.6 Russia

- 5.3.3.1.7 Spain

- 5.3.3.1.8 Switzerland

- 5.3.3.1.9 Turkey

- 5.3.3.1.10 United Kingdom

- 5.3.3.1.11 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Bahrain

- 5.3.4.1.2 Kuwait

- 5.3.4.1.3 Oman

- 5.3.4.1.4 Qatar

- 5.3.4.1.5 Saudi Arabia

- 5.3.4.1.6 United Arab Emirates

- 5.3.4.1.7 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Arcor S.A.I.C

- 6.4.2 August Storck KG

- 6.4.3 Barry callebaut AG

- 6.4.4 Cargill Incorporated

- 6.4.5 Chocoladefabriken Lindt & Sprungli AG

- 6.4.6 Ferrero International SA

- 6.4.7 ITC Limited

- 6.4.8 Lotte Corporation

- 6.4.9 Mars Incorporated

- 6.4.10 Meiji Holdings Company Ltd

- 6.4.11 Mondelez International Inc.

- 6.4.12 Morinaga & Co. Ltd

- 6.4.13 Nestle SA

- 6.4.14 The Hershey Company

- 6.4.15 YIldIz Holding AS

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

チョコレート:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 386 Pages

- 納期

- 2~3営業日