建設用複合材料:市場シェア分析、産業動向、成長予測(2025~2030年)

Construction Composite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687127

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

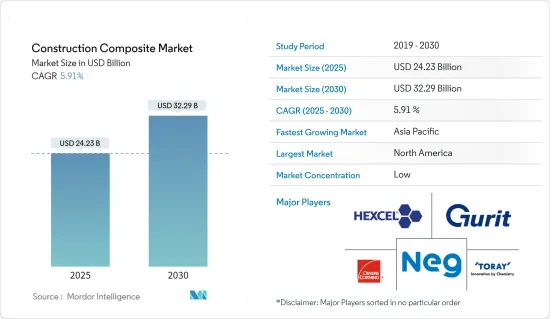

建設用複合材料の市場規模は2025年に242億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.91%で、2030年には322億9,000万米ドルに達すると予測されています。

COVID-19は、パンデミックが国際貿易に深刻な影響を与え、製造、建築、建設を含むいくつかの産業に支障をきたしたため、2020年の市場にマイナスの影響を与えました。しかし、2021年にはこれらのセクターからの市場需要が大幅に回復しました。

主要ハイライト

- 中期的には、建設用途での複合材料の使用増加と老朽化したコンクリート構造物の修復が市場成長の原動力となっています。

- 一方、複合材料の初期生産コストと施工コストが高く、熟練労働者の不足も相まって、市場の成長を妨げています。

- 建設セグメントでの複合材料の大量生産能力の向上は、今後数年間で市場に機会をもたらす可能性が高いです。

- 北米が収益面で市場を独占すると予想される一方、アジア太平洋が予測期間中に最も高いCAGRで推移すると考えられます。

建設用複合材料の市場動向

土木建設セグメントが市場を独占

- 土木建設は、橋梁、ダム、道路、空港、運河、鉄道インフラ、関連構造物の建設で構成されます。

- 2021年末には、中国のいくつかの省が大規模なインフラプロジェクトを発表しました。中国南部の広西チワン族自治区は、投資総額1,859億人民元(291億5,000万米ドル)の大型建設プロジェクトを発表しました。これらのプロジェクトは、交通、新エネルギー、物流、基礎インフラなど多くのセグメントをカバーしています。

- さらに中国は、都市化を推進し地域経済を活性化させる長期計画の一環として、世界第2位の規模を誇る鉄道網を今後15年間で3分の1に拡大する計画です。国有企業である中国国有鉄道集団が発表した計画によると、中国は2035年末までに約20万km(124,274マイル)の鉄道を敷設することを目標としており、その中には約7万kmの高速鉄道も含まれています。

- ドイツでは、交通・デジタルインフラ省が、電気モビリティや電気自動車充電インフラの自動化・ネットワーク化運転などの将来技術に3億4,872万米ドルを投資する計画です。また、シュヴァルムシュタットとヘッセン州中部のオームタールインターチェンジを結ぶA49高速道路プロジェクトにも着手しました。これにより、複合材料の消費量が増加することが予想されます。

- シュヴァルムシュタット-オームタールプロジェクトは官民パートナーシップ・モデルに基づいており、投資額は8億1,368万米ドルです。93kmの道路で構成されるこの工事は、2024年第3四半期に完成する予定です。こうした大規模な鉄道・道路建設プロジェクトが、予測期間中の建設用複合材料の需要を牽引する可能性があります。

- 米国国勢調査局によると、米国で実施された高速道路と道路建設の年間金額は、2020年の1億232万米ドルに対し、2021年は1億68万米ドルでした。

- カナダでは、「カナダへの投資」計画の一環として、政府は2028年までに国内の主要インフラ開発に約1,400億米ドルを投資する計画を発表しました。

市場を独占する北米地域

- 北米では、米国、カナダ、メキシコなどの国々で建設部門が成長しているため、建設用複合材料の利用が増加しています。

- 北米地域は、建設用複合材料の最大消費市場のひとつです。米国は世界最大の建設産業の1つです。2021年通年の建設支出は1兆5,903億7,000万米ドルに達し、2020年の1兆4,692億米ドルを8.2%上回りました。

- 米国国勢調査局によると、2022年2月の同国の建設支出は、季節調整済み年率1,704億米ドルと推定され、1月修正値の1兆6,955億米ドルを0.5%上回りました。さらに、2022年2月の推定値は、2021年2月の推定値1兆5,333億米ドルを11.2%上回ります。2022年1~2月期の建設支出は2,378億米ドルで、2021年同期の2,154億米ドルを10.4%上回りました。

- カナダでは最近、住宅・商業部門が安定した成長を遂げています。カナダ(より具体的にはトロント)では最近、超高層ビルの建設ブームが起きています。2025年までに30棟以上の超高層ビルが完成する見込みで、トロントではさらに50棟の超高層ビルが提案・計画段階にあります。

- さらに、「カナダへの投資計画」の一環として、政府は2028年までに国内のインフラ開発に1,400億米ドル近くを投資する計画を発表しています。

建設用複合材料産業概要

世界の建設用複合材料市場はセグメント化されています。同市場の主要企業(順不同)には、Hexcel Corporation、Owens Corning、Nippon Electric Glass、Toray Industries Inc.、Guritなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設用途における複合材料使用の増加

- 老朽コンクリート構造物の修復

- 抑制要因

- 複合材料の初期製造コストと設置コストの高さ

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 樹脂タイプ

- ポリエステル樹脂

- ビニルエステル

- ポリエチレン

- ポリプロピレン

- エポキシ樹脂

- その他

- 繊維タイプ

- 炭素繊維

- ガラス繊維

- 天然繊維

- その他の繊維タイプ

- 最終用途セグメント

- 工業用

- 商業

- 住宅用

- 民間

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ ランキング分析

- 主要企業の戦略

- 企業プロファイル(概要、財務、製品・サービス、最近の動向)

- Aegion Corporation

- Exel Composites

- Gurit

- Hexcel Corporation

- Kordsa Teknik Tekstil AS

- Toray Industries Inc.

- Mitsubishi Chemical Corporation

- Nippon Electric Glass Co. Ltd

- Owens Corning

- SGL Carbon

- Teijin Limited

第7章 市場機会と今後の動向

- 建設セグメントにおける複合材料の大量生産能力の向上

目次

The Construction Composite Market size is estimated at USD 24.23 billion in 2025, and is expected to reach USD 32.29 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020 as the pandemic severely affected international trade and hampered several industries, including manufacturing, building, and construction. However, in 2021, the market demand from these sectors recovered significantly.

Key Highlights

- Over the medium term, the factors driving the growth of the market studied are the increasing usage of composites in construction applications and the rehabilitation of old concrete structures.

- On the other hand, the high initial production and installation costs of composites, coupled with the inadequacy of skilled labor, are hindering the market's growth.

- Increasing the ability to mass-produce composites in the construction sector will likely create opportunities for the market in the coming years.

- North America is expected to dominate the market in terms of revenue while the Asia-Pacific region is likely to witness the highest CAGR during the forecast period.

Construction Composites Market Trends

Civil Construction Sector to Dominate the Market

- Civil construction comprises the construction of bridges, dams, roads, airports, canals, railway infrastructure, and related structures.

- Toward the end of 2021, several Chinese provinces announced major infrastructure projects. South China's Guangxi Zhuang Autonomous Region unveiled a batch of major construction projects, with a total investment of CNY 185.9 billion (USD 29.15 billion). Those projects cover many sectors, including transportation, new energy, logistics, and basic infrastructure.

- Furthermore, China plans to expand its railway network, which is the second-largest in the world, by one-third in the next 15 years, as part of a long-term plan to propel urbanization and stimulate local economies. According to a plan issued by the state-owned China State Railway Group, China aims to have about 200,000 km (124,274 miles) of railway tracks by the end of 2035, including about 70,000 km of high-speed railways.

- In Germany, the Ministry of Transport and Digital Infrastructure plans to invest USD 348.72 million in future technologies, such as electric mobility or automated and networked driving for electric vehicle charging infrastructure. Also, the country has started working on the A49 highway project connecting Schwalmstadt and the Ohmtal interchange in Central Hesse. This, in turn, is expected to increase the consumption of composite materials.

- The Schwalmstadt-Ohmtal project is based on a public-private partnership model with an investment of USD 813.68 million. The construction, which comprises 93 km of road, is expected to be completed in the third quarter of 2024. These massive railway and road construction projects may drive the demand for construction composites during the forecast period.

- According to US Census Bureau, annual value of highway and street construction put in place of United states, in 2021 accounted for USD 100.68 million, compared to USD 102.32 million in 2020.

- In Canada, as part of the "Investing in Canada" plan, the government announced plans to invest nearly USD 140 billion in major infrastructure developments in the country by 2028.

North America Region to Dominate the Market

- In North America, the utilization of construction composites is increasing due to the growing construction sector in countries such as the United States, Canada, and Mexico.

- The North American region is one of the largest consumption markets for construction composites. The United States has one of the world's largest construction industries. In the full year 2021, construction spending amounted to USD 1,590.37 billion, 8.2% above USD 1,469.2 billion in 2020, thereby increasing the consumption of construction composites from various construction applications.

- According to the US Census Bureau, during February 2022, the construction spending in the country was estimated at a seasonally adjusted annual rate of USD 1704.4 billion, 0.5% more than the revised January estimate of USD 1,695.5 billion. Moreover, the February 2022 estimation is 11.2% more than the February 2021 estimate of USD 1,533.3 billion. During the first two months of 2022, construction spending amounted to USD 237.8 billion, 10.4% percent above USD 215.4 billion for the same period in 2021.

- In Canada, the residential and commercial sectors have been witnessing steady growth in the recent past. There has been a boom in the construction of skyscrapers in Canada (more specifically in Toronto) in recent times. Over 30 high-rise buildings are expected to be completed by 2025, and another 50 such buildings are in the proposal and planning phases in Toronto.

- Moreover, as part of the ''Investing in Canada Plan'', the government has announced plans to invest nearly USD 140 billion in infrastructure developments in the country by 2028.

Construction Composites Industry Overview

The global construction composite market is fragmented. Some major players in the market (in no particular order) include Hexcel Corporation, Owens Corning and Nippon Electric Glass Co. Ltd., Toray Industries Inc., and Gurit.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use of Composites in Construction Applications

- 4.1.2 Rehabilitation of Old Concrete Structures

- 4.2 Restraints

- 4.2.1 High Initial Production and Installation Costs of Composites

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 Resin Type

- 5.1.1 Polyester Resin

- 5.1.2 Vinyl Ester

- 5.1.3 Polyethylene

- 5.1.4 Polypropylene

- 5.1.5 Epoxy Resin

- 5.1.6 Other Resin Types

- 5.2 Fiber Type

- 5.2.1 Carbon Fibers

- 5.2.2 Glass Fibers

- 5.2.3 Natural Fibers

- 5.2.4 Other Fiber Types

- 5.3 End-use Sector

- 5.3.1 Industrial

- 5.3.2 Commercial

- 5.3.3 Housing

- 5.3.4 Civil

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) ** / Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 Aegion Corporation

- 6.4.2 Exel Composites

- 6.4.3 Gurit

- 6.4.4 Hexcel Corporation

- 6.4.5 Kordsa Teknik Tekstil AS

- 6.4.6 Toray Industries Inc.

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Nippon Electric Glass Co. Ltd

- 6.4.9 Owens Corning

- 6.4.10 SGL Carbon

- 6.4.11 Teijin Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Ability to Mass Produce Composites in the Construction Sector

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日