|

市場調査レポート

商品コード

1907309

医薬品受託製造機関(CMO):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Pharmaceutical Contract Manufacturing Organization (CMO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医薬品受託製造機関(CMO):市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

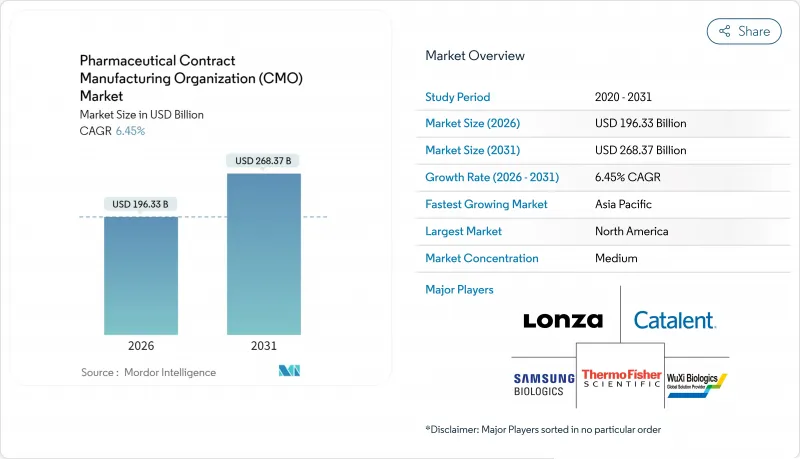

医薬品受託製造機関(CMO)市場は、2025年の1,844億4,000万米ドルから2026年には1,963億3,000万米ドルへ成長し、2026年から2031年にかけてCAGR 6.45%で推移し、2031年には2,683億7,000万米ドルに達すると予測されています。

この成長の勢いは、業界が中核的な創薬・商業化業務へ戦略的に再調整し、複雑な生産活動を専門パートナーに委ねる動きに起因しています。バーチャルバイオテック企業へのベンチャーキャピタル流入、先進的治療法の記録的な承認件数、高効力APIパイプラインの拡大が、外部生産能力への移行を後押ししています。一方、コスト圧力、規制当局の監視強化、最先端技術の必要性により、大手製薬企業、専門企業、ジェネリック企業を問わず、適格な受託製造業者との連携深化が進んでいます。開発、スケールアップ、充填・仕上げサービスを包括的に提供しつつ、世界の品質基準を維持できるプロバイダーは、医薬品受託製造機関(CMO)市場において引き続き大きな機会を獲得しています。

世界の医薬品受託製造機関(CMO)市場の動向と洞察

中小規模製薬企業のアウトソーシング加速

FDAによる2024年の査察体制刷新後、コンプライアンスコストが急増し、中規模工場の年間品質関連費用は200万~500万米ドル増加しました。この資本負担により、リソースに制約のあるスポンサー企業は、がん治療薬や希少疾患治療薬のポートフォリオにおいて戦略的なアウトソーシングを選択する傾向にあります。開発と商業化機能を統合した受託製造企業は、予測可能なパイプライン流入の恩恵を受ける一方、従量課金型とリスク分担型を組み合わせたハイブリッドモデルが注目を集めています。

バイオ医薬品パイプラインの複雑化

マルチ特異性抗体、抗体薬物複合体、自家細胞療法は、独自のアップストリーム細胞培養、精製、コールドチェーンインフラを必要とし、自社内での導入を正当化できる革新企業はほとんどありません。サムスンバイオロジクスは2024年、シングルユースバイオリアクターの容量拡大に24億米ドルを投資することを表明し、現代的な生物学的製剤生産に必要な投資規模を示しました。ターンキープロセス開発、ウイルス除去、充填・仕上げサービスを提供するプロバイダーは、生物学的製剤のライフサイクル全体において、今や重要なパートナーとなっています。

充填・仕上げラインにおける生産能力のボトルネック

複雑な注射剤において稼働率が85%を超え、リードタイムが18ヶ月を超える状況は、CDMOが新規バイオ医薬品プログラムを吸収する能力を制限しています。無菌室、高度なロボット技術、シリアル化アップグレードには複数年にわたる投資が必要であり、改善が遅れることで短期的な供給逼迫が続き、近い将来の収益実現が制約される可能性があります。

セグメント分析

2025年時点で、医薬品受託製造機関(CMO)市場シェアの41.98%を原薬製造が占め、ジェネリック医薬品とブランド医薬品の幅広い需要を支えています。低分子医薬品の生産量が依然として主流である一方、バイオ医薬品および高活性原薬(HPAPI)の生産能力増強により、収益構成は高付加価値製品へと移行しつつあります。顧客は供給の引き継ぎを排除するため、合成・精製・最終製剤製造を同一拠点で提供する統合サービスをますます求めています。

固形剤と注射剤の両方の製剤を提供できる受託企業は、範囲の経済性を享受しています。デジタルシリアル化、連続製造、予知保全は運営コスト曲線を再構築し、参入障壁を新たに設定しています。包装サービス、特に改ざん防止機能や追跡管理ソリューションとの統合は、提供者をさらに差別化します。

2025年の収益に占める低分子医薬品の割合は依然として56.85%でしたが、先進医療分野が8.22%のCAGRで最も急速な拡大を遂げました。開発者が根治的治療の可能性を追求する中、ウイルスベクター生産、細胞培養技術、極低温保存が現在、設備投資の優先事項を支配しています。先進治療薬向け医薬品受託製造機関市場規模は、承認製品の自家移植から同種移植プロセスへの移行が進むにつれ拡大が見込まれ、より大規模で標準化された製造工程が求められるようになります。

バイオシミラーの採用と新規抗体フォーマットにより、生物学的製剤は中間的な成長段階にあります。全ての分子クラスにおける持続的な投資は、CDMOが単一プラットフォームの専門性ではなく、多様な技術ポートフォリオを維持することが戦略的に不可欠であることを裏付けています。

医薬品受託製造機関レポートは、サービスタイプ(原薬製造など)、薬剤分子タイプ(低分子、生物学的製剤、先進治療など)、操業規模(臨床段階製造など)、エンドユーザー(大手製薬企業、ジェネリック医薬品企業など)、治療領域(腫瘍学、循環器など)、地域別に分類されています。市場予測は金額ベース(米ドル)で提供されます。

地域別分析

北米は2025年の収益の39.85%を占めており、強固な知的財産権枠組み、医薬品開発企業への近接性、深い規制専門知識に支えられています。継続的製造および細胞療法インフラへの継続的な投資により、同地域は優先的なパートナー拠点であり続けていますが、高い人件費が増設容量の拡大を制限しています。

アジア太平洋地域は8.91%のCAGRで最も急速に成長しており、中国、インド、韓国における大規模投資が牽引しています。サムスンバイオロジクスの24億米ドル規模の拡張計画は、同地域が最先端のバイオ医薬品生産能力に注力していることを示す好例です。通貨変動や進化する品質要求が運営上の課題となる一方、低い固定費と政府の優遇措置が、医薬品受託製造機関(CMO)市場における同地域の魅力を維持しています。

欧州は、ドイツ、アイルランド、スイス、スカンジナビアに確立されたクラスターにより安定した需要を享受しています。調和された欧州医薬品庁(EMA)の規制は、特に先進治療分野において国境を越えたサプライチェーンを促進します。中東・アフリカ地域は依然として発展途上ですが、各国政府が医薬品の安全保障と現地製造義務を追求する中で潜在性を示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 中小規模製薬企業のアウトソーシング加速

- バイオ医薬品パイプラインの複雑化

- ベンチャーキャピタル資金によるバーチャルバイオテック企業の増加

- 高効力原薬(HPAPI)に対する需要急増

- 細胞・遺伝子治療CDMO生産能力の拡大

- ESG連動型サプライチェーン認証

- 市場抑制要因

- 充填・包装ラインにおける生産能力のボトルネック

- 規制検査の強化と是正コストの増加

- 変動の激しいシングルユースシステムの供給

- 新興拠点における通貨変動に起因するコスト上昇

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- マクロ経済要因の影響

- 投資分析

第5章 市場規模と成長予測

- サービスタイプ別

- API製造

- 低分子化合物

- 高分子医薬品

- 高活性医薬品原料(HPAPI)

- FDFの開発と製造

- 固形剤

- 液剤

- 注射剤

- 二次包装

- API製造

- 薬剤分子タイプ別

- 低分子化合物

- 生物学的製剤

- 先進医療(細胞・遺伝子治療)

- 運用規模別

- 臨床段階製造

- 商業規模製造

- エンドユーザー別

- 大手製薬企業

- ジェネリック医薬品

- 新興/バーチャルバイオテック

- スペシャリティ医薬品

- 治癒領域別

- 腫瘍学

- 循環器系

- 中枢神経系(CNS)

- 感染症

- その他の治療領域

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ケニア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Lonza Group Ltd.

- Catalent Inc.

- Thermo Fisher Scientific Inc.

- Samsung Biologics Co. Ltd.

- WuXi Biologics(Cayman)Inc.

- Recipharm AB

- Jubilant Pharmova Ltd.

- Boehringer Ingelheim GmbH

- Pfizer CentreOne(Pfizer Inc.)

- Baxter International Inc.(Baxter BioPharma Solutions)

- Aenova Holding GmbH

- PCI Pharma Services

- Cambrex Corporation

- Siegfried Holding AG

- Evonik Industries AG

- Alcami Corporation

- Ajinomoto Bio-Pharma Services

- Eurofins CDMO Alphora Inc.

- Famar SA

- Tapemark LLC