|

市場調査レポート

商品コード

1907305

アクセス制御:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Access Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アクセス制御:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

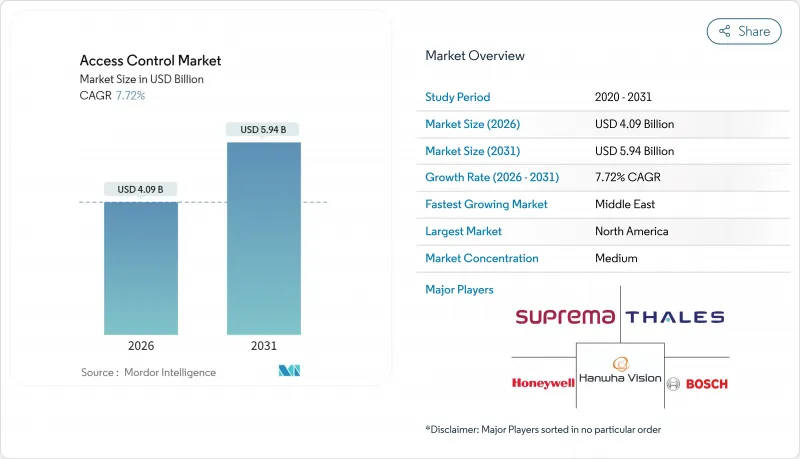

2026年のアクセス制御市場規模は40億9,000万米ドルと推定され、2025年の38億米ドルから成長を続けております。

2031年には59億4,000万米ドルに達する見込みで、2026年から2031年にかけてCAGR7.72%で拡大すると予測されております。

クラウド管理、モバイル認証、生体認証技術が企業、公共部門、重要インフラ施設において従来の鍵やカードを置き換えるにつれ、需要は高まっています。より厳格なデータ保護規制、非接触型ユーザー体験への重視、および映像監視システムとの統合が、アップグレードサイクルを加速させています。半導体不足に伴う価格上昇は、買い手をソフトウェア定義アーキテクチャへと導いており、これにより将来を見据えた設備投資が可能となり、サプライチェーンリスクも軽減されます。

世界のアクセス制御市場の動向と洞察

GDPR対応が求められるEUデータセンターにおける電子アクセス規制要件

2024年10月に発効するNIS2指令では、全ての物理的入口において多要素認証と改ざん防止機能付き監査証跡が義務付けられます。データセンター運営者は、暗号化および継続的監視条項を満たすため、従来のカードから生体認証やモバイル認証への移行を加速しています。ベンダーのサプライチェーン審査により調達基準が引き上げられ、自動化されたコンプライアンス報告機能を備えたプラットフォームへの需要が高まっています。NIS2とGDPRの相乗効果により、個人データを保護しつつ物理的セキュリティを強化する統合ソリューションの需要が高まり、アクセス制御市場全体の更新予算が増加しています。

北米企業不動産における非接触型モバイル認証の導入

商業用不動産オーナーは、物理的な接触なしで改札機・エレベーター・オフィスルームの解錠が可能なApple WalletおよびGoogle Pay認証を発行しております。リモートプロビジョニングによりバッジ発行コストが削減され、フレキシブルな座席ポリシーの実現を支援します。暗号化された無線更新により、施設管理チームは紛失した端末を即時無効化でき、セキュリティ強化とテナント体験の向上を両立します。既存のスマートフォンインフラとの互換性によりカードプリンター関連の経費が不要となり、導入メリットがさらに高まっております。迅速な導入サイクルは運用効率の顕著な向上につながり、アクセス制御市場の勢いをさらに加速させております。

EUクラウド導入におけるサイバーセキュリティコンプライアンスコスト(NIS2)

クラウドホスト型アクセスプラットフォームは、NIS2を満たすために継続的な脅威監視、セキュアなコード署名、文書化された開発パイプラインを追加する必要があり、ベンダーの運用コストを15~20%増加させます。小規模プロバイダーは監査費用やペネトレーションテスト費用の吸収に苦慮し、認定インフラを持つ世界のブランドへ買い手が集中する中で業界再編が引き起こされています。一部のEU企業はアップグレードを延期し、更新サイクルを延長しているため、アクセス制御市場の成長見通しはわずかに鈍化しています。

セグメント分析

2025年の収益はハードウェアが61.45%のシェアで主導し、物理的導入における電子錠、コントローラー、生体認証リーダーの必須性を反映しています。大学施設のリニューアルだけで、キャンパスがモバイル対応インフラへ移行する中で、大幅なロック更新サイクルが促進されました。電子錠は、ハンズフリー入室を可能にする超広帯域モジュールにより、最も速い単位成長を記録しました。生体認証マルチセンサーリーダーは、高信頼性認証を要求する研究所や薬局で普及が進んでいます。

ソフトウェアは2031年までにCAGR8.78%で拡大し、管理コンソールに予測分析やAI駆動型異常検知機能を追加します。クラウド制御基盤は分散サイトを統合し、リアルタイムポリシー配信と自動コンプライアンス監査を可能にします。ダッシュボード内での映像アクセス統合は調査能力を強化し、オープンAPIはエコシステム開発を促進します。統合サービスと継続的サポート契約はパートナー収益を拡大し、マネージドサービスをアクセス制御業界における堅牢な継続的収益源として位置づけています。

ホステッドACaaSは2025年の導入実績の51.60%を占め、サーバー所有よりも予測可能なサブスクリプションを好む中小企業が牽引しています。オンプレミスソリューションと同等の機能に加え、自動更新により、小規模なIT部門の技術的負担を軽減します。詳細なテナントポータルは、コワーキングブランドが数千人のメンバーを動的に管理することを支援し、アクセス制御市場における顧客ロイヤルティを深化させます。

ハイブリッドACaaSはCAGR8.35%で最も急成長しているモデルであり、規制対象企業向けにクラウドオーケストレーションとローカルエッジストレージのバランスを実現します。病院ではネットワーク障害時に機密ログをオンサイトアプライアンスにルーティングし、接続回復後に分析のためクラウドと同期します。マネージドACaaSは、複雑なマルチベンダー環境で特注の統合が必要なニッチ市場を維持していますが、プラットフォームはより広範なアクセス制御市場において、業界横断的に拡張可能なセルフサービス型パラダイムへと着実に収束しつつあります。

アクセス制御市場は、コンポーネント別(ハードウェア、ソフトウェア、サービス)、ACaaS導入形態別(ホステッド、マネージド、ハイブリッド)、認証方法別(シングルファクター、マルチファクター、モバイル認証)、接続技術別(RFID/NFC、スマートカード、Bluetooth LE、UWB)、エンドユーザー業種別(商業、産業、政府機関など)、および地域別に分類されます。市場予測は金額(米ドル)ベースで提供されます。

地域別分析

北米は、企業キャンパス、大学、病院における大規模な近代化を背景に、2025年における収益シェア38.30%を維持しました。ケンタッキー大学の9,000ドアの変換など、米国の高等教育機関における改修事例は、アクセス制御と出席分析を融合したモバイル対応プラットフォームがキャンパス全体で採用されていることを示しています。カナダのスマートビルディング奨励策やメキシコの越境物流施設が需要を押し上げています。UWB(超広帯域)や生体認証スタートアップへのベンチャー投資により、同地域はアクセス制御市場における技術革新の最前線に位置し続けています。

中東地域は2031年までCAGR9.22%で最も急速に成長する地域であり、国家主導のスマートシティ構想とセキュリティ優先の規制枠組みが牽引しています。アラブ首長国連邦(UAE)とサウジアラビアでは、物理的な身分証明書に代わる顔認証・虹彩認証・指紋認証システムの大規模導入が進み、カタールとオマーンでは全国規模のIoT指令センターにアクセス制御機能を組み込んでいます。現地のシステムインテグレーターは世界のベンダーのSDKを活用し、地域特化型ソリューションを開発することで市場の現地化を加速させています。

欧州では厳格なプライバシー法規制にもかかわらず着実な成長が見られます。NIS2(ネットワーク情報セキュリティ指令)やEU AI法では、生体認証利用に際し明示的な同意と透明性が求められています。これに対し、組織はハイブリッド型ACaaS(アクセス制御サービス)を採用し、機密性の高い生体認証テンプレートを欧州域内に保持する対応を取っています。ドイツ、フランス、英国はベンダーロックイン回避のためオープンプロトコルシステムを優先し、北欧の事業者は持続可能な低消費電力リーダーの開発を主導しています。東欧の交通ハブではカード式バリアをモバイル認証や映像認証による入退場システムへ更新しており、これら全てがアクセス制御市場の収益拡大に寄与しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- GDPR対応が求められるEUデータセンターにおける電子アクセス規制要件

- 北米企業不動産における非接触型モバイル認証の導入状況

- 中東におけるスマートシティ及び重要インフラ計画がバイオメトリクスを促進

- アジア太平洋地域のコワーキングスペース拡大がクラウドベースのACaaSを牽引

- 欧州交通ハブにおけるIPビデオアクセス制御の統合アップグレード

- 米国高等教育機関における老朽化したキーカードシステムの更新需要

- 市場抑制要因

- EUクラウド導入におけるサイバーセキュリティコンプライアンスコスト(NIS2)

- セキュアMCUチップ不足がリーダー出荷に影響

- 米国およびEU諸国における顔認証技術へのプライバシー反発

- 南米における中小企業の予算制約

- サプライチェーン分析

- 技術概要(進化、RFID対NFC、主要動向)

- 規制とテクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 投資と資金調達分析

第5章 市場規模と成長予測

- コンポーネント別

- ハードウェア

- カード/近接/スマートカードリーダー

- 生体認証リーダー(指紋、顔、虹彩、マルチモーダル)

- 電子錠(磁気式、電気ストライク、デッドボルト、ワイヤレススマートロック)

- コントローラーおよびパネル

- ソフトウェア

- アクセス制御管理スイート

- ビデオ管理統合プラグイン

- サービス

- 設置および統合

- サポートおよび保守

- ハードウェア

- アクセス制御サービス(Deployment)別

- ホスト型ACaaS

- マネージドACaaS

- ハイブリッドACaaS

- 認証方法別

- シングルファクター認証

- 多要素認証

- モバイル認証/Bluetooth LE

- コネクティビティテクノロジー別

- RFID/NFC

- スマートカード(125kHz、13.56MHz)

- Bluetooth Low Energy

- 超広帯域(UWB)

- エンドユーザー業界別

- 商業ビル

- 産業・製造業

- 政府および公共部門

- 輸送・物流

- 医療施設

- 軍事・防衛施設

- 住宅およびスマートホーム

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- ASEAN

- オーストラリア

- ニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- GCC

- トルコ

- イスラエル

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、提携、製品発表)

- 市場シェア分析

- 企業プロファイル

- ASSA ABLOY AB

- Johnson Controls International plc(Tyco)

- Honeywell International Inc.

- Dormakaba Holding AG

- Allegion plc

- Bosch Security Systems Inc.

- Thales Group(Gemalto)

- Suprema Inc.

- Hanwha Vision Co. Ltd.

- Schneider Electric SE

- NEC Corporation

- Idemia Group

- Nedap N.V.

- Axis Communications AB

- Panasonic Connect Co. Ltd.

- Brivo Systems LLC

- Identiv Inc.

- Salto Systems S.L.

- Siemens Smart Infrastructure

- Genetec Inc.