|

市場調査レポート

商品コード

1850136

肥料添加剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Fertilizer Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 肥料添加剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

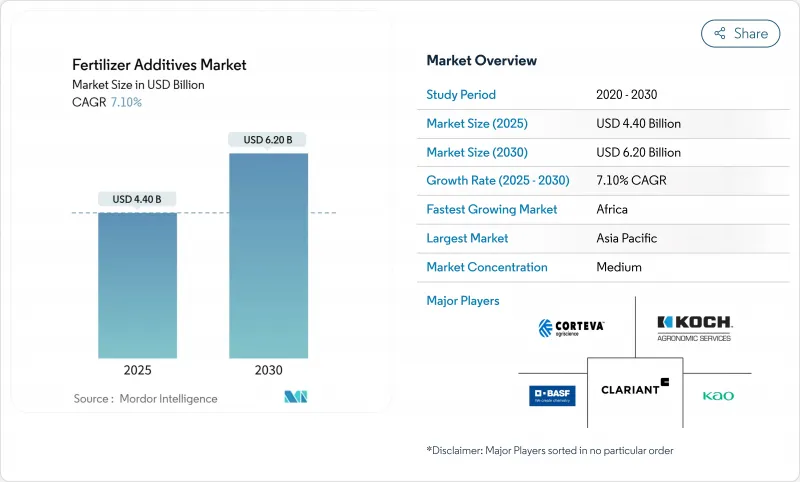

肥料添加剤市場は、2025年には44億米ドルであったが、2030年には62億米ドルに拡大し、予測期間を通じて7.10%のCAGRで堅調に推移します。

成長の背景には、養分使用規則の厳格化、精密農業の急増、投入コストの上昇などがあり、生産者は窒素やリン酸の施用単位を保護する添加剤を求めるようになります。効率向上製品は現在、米国のトウモロコシ栽培面積の37%をすでにカバーしている可変レート技術と組み合わされ、圃場と灌漑ピボットに同様に微量投与の精度をもたらしています。両地域とも、プラントゲートからプランターボックスまでの流動性を維持するために、固結防止剤とコーティング剤に依存しています。グリーン・アンモニア・プロジェクトが増加し、-33℃の貯蔵温度でも活性を維持する薬剤が必要とされる中、需要は低温アンモニア・ロジスティクス周辺にも形成されつつあります。サプライヤー間の集中は緩やかで、生物学的安定剤、バイオポリマー・コーティング、デジタル投与サポートを1つの性能パッケージにまとめた革新的なサプライヤーが活躍する余地があります。

世界の肥料添加剤市場の動向と洞察

集約型農業地域における肥料消費の増加

穀物需要の急増は、すでに最大強度で耕作している地帯の添加剤量を増加させる。OECD-FAO Outlookは、世界の穀物需要が2032年までに31億トンに達すると見ており、そのほとんどはアジアとアフリカからのものです。添加剤は、湿度の高い灌漑システムで増加する養分損失を阻止し、500万エーカー以上の農地が、灌漑中の揮発を削減する強化された製剤で稼動しているworldfertilizer.com。点滴やピボット・システムを使用する生産者は、90%近い養分使用効率を達成し、高湿度下でも混合液の流動性を保つ固結防止剤やコーティング剤のさらなる普及を推進しています。食糧安全保障に向けた資本の流入は、添加物サプライヤーにとって予測可能な長期的需要曲線を生み出します。

効率向上肥料(EEF)の需要。

198億米ドルの付加価値肥料は、バイオ刺激剤、阻害剤、および放出制御コーティング剤を、タイミングと作物相に合わせて単一の粒剤に統合したものです。NBPTのようなウレアーゼ阻害剤は、Duromide安定剤と組み合わせることで、アンモニア損失を54%低減し、生産者が余分なパスなしに高タンパク質の穀物を得るのに役立ちます。米国のバイオスティミュラントの売上は2026年までに3倍の12億米ドルになり、従来の栄養プログラムに生物学的製剤が組み込まれます。ポリマー・コーティングされた放出制御型薬剤は、デリバリー・ウィンドウをさらに強化し、肥料添加剤市場を、供給と根の需要を同期させる、よりスマートな多層フィルムへと向かわせる。

作物投入資材のコスト上昇

2025年初めの肥料価格は11%上昇し、穀物価格が低迷する中、農家の利幅を圧迫しました。UAN28の出荷価格は1トン当たり354米ドル、DAPは765米ドル、MAPは810米ドルに達し、資金繰りに苦しむ生産者にとってはプレミアム添加剤の販売が難しくなりました。ラボバンクのアフォーダビリティ・インデックスは、特に窒素とリン酸のカテゴリーで、すでに農家支出の大部分を占めている需要破壊リスクを示唆しています。アフリカと南アジアの小規模農家は、最も厳しいトレードオフに直面しており、投資回収が証明されているにもかかわらず、効率向上のための購入を延期することが多いです。

セグメント分析

2024年の肥料添加剤市場では、固結防止剤が売上の37%を占め、最も大きな割合を占めています。この優位性は、湿度の高い出荷シーズンや倉庫での長い待ち時間の間、粒子の流れを維持するためにこの材料が重要な役割を果たすことに起因しています。脂肪アミンブレンドと還元界面活性剤システムは現在、鉄道車両内での圧縮に耐えるより薄く柔軟なフィルムを作ることで、初期のバイオワックスを凌駕しています。しかし、コーティング剤はCAGR 9.8%で成長の王冠をかぶり、45日から90日のスパンで放出されるポリマーとバイオポリマーフィルムに後押しされています。この2大リーダーは、信頼性と栄養タイミングがいかに購買決定を左右するかを示しています。

第二のカテゴリーも進化しています。インヒビターは亜酸化窒素の抑制という規制の要請に応え、造粒助剤は厳しい粒子公差を要求する精密アプリケーターのコンバージョンを獲得しています。新興のハイブリッド製品は、固結防止剤、抑制剤、コーティング剤の機能を単一の添加剤に融合させたもので、混入率を削減し、サプライチェーンを簡素化します。腐食防止剤が液体肥料に使用されるようになる一方、作業員の暴露基準が厳しくなっている地域では除錆剤が勢いを増しています。肥料添加剤市場は、1回の投与で複数の難点を解決できる多目的化学物質に引き寄せられ続けています。

粒状栄養剤は、タルクベースのコンディショナー、ワックス、脂肪アミンパウダーの売上の68%を占め、安定したキャッシュフローを生み出しています。バルクターミナルとバージのオペレーターは、固形固結防止剤に頼って、山積みの流動性を維持しています。液剤は規模は小さいもの、CAGR 8.4%を記録しており、灌漑面積の増加とドローンスプレーの採用を反映しています。液体分散液はナースタンクで素早く溶解し、収量マップに合わせた可変レートでのインライン注入を可能にします。

マイクロカプセル剤は、この2つの極の中間に位置します。有効成分を保護し、放出を遅らせ、ポリ乳酸やデンプンから作られた堆肥化可能な殻で、迫り来るマイクロプラスチック規制を満たします。ミリケンのマイクロカプセルへの取り組みは、次世代デリバリー・ルートへの資本移動を示しています。肥料添加剤市場では、フォームファクターが収束しつつあります。いくつかのサプライヤーは現在、液体シードドレッシングと、トップドレスパス用のコンパニオンドライコーティングの両方を含むキットを提供しており、シーズンを通して一貫した栄養コントロールを保証しています。

地域分析

アジア太平洋地域は、中国とインドの小規模農家が密集しており、合計で30億人近い人々にサービスを提供しているため、2024年の売上高で39%の王座を維持した。中国がリン酸塩の輸出を一時的に制限したことで、国内の添加剤ラインが恩恵を受け、供給が地元チャネルに再編成され、輸入依存度が低下します。インドの化学品セクターは、土壌ラボや農場センサーに資金を提供するデジタル農業ミッションに後押しされ、2025年までに500億米ドルの特殊売上高を達成する勢いです。肥料添加剤の市場規模では、国内生産者が統合サプライチェーンを活用し、不安定な運賃市場にもかかわらず納入コストを低く抑えています。

アフリカは、政府と民間資本が新たな生産拠点に資金を投入しているため、CAGR最速の10.5%を示しています。ナイジェリアの150万トンプラントとインドラマの280万トン拡張に牽引され、10年後までに栄養塩の消費量は760万トンから1,360万トンに急増すると思われます。西アフリカだけでも、2030年までに460万トンを超える可能性があります。しかし、添加剤サプライヤーは、フローコンディショナーを農民のトレーニングとともにパッケージ化し、受け入れ拡大につなげる余地があると考えています。

北米と欧州はCAGR 5.2%と4.5%と、成熟しつつも革新的な成長を示しています。英国の農場の28%が、マメ科植物の輪作を利用して肥料計画を調整し、窒素を固定して化学合成農薬の散布を抑制しています。EUの炭素国境調整メカニズムは2026年に導入され、肥料の輸入業者には炭素含有量の開示が義務付けられます。両大陸では、生物学的代替肥料がシェアを伸ばしているが、寒冷地や狭い作付け期間でもその性能データが安定していることから、化学コーティング剤も根強い人気を誇っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 高集約型農業地域における肥料消費量の増加

- 高効率肥料(EEF)の需要

- 栄養素利用効率を高める規制の推進

- マイクロドージングを可能にする精密農業の導入

- 極低温低炭素アンモニア物流が新たな固結防止ニーズを生み出す

- 土壌微生物に優しいバイオポリマーコーティング

- 市場抑制要因

- 農作物の投入コストの上昇

- 添加物に関する環境規制の強化

- 特殊界面活性剤の石油化学原料の揮発性

- 生物学的代替品の急速な出現

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 機能別

- 阻害剤

- コーティング剤

- 造粒助剤

- 固結防止剤

- 除塵剤

- 腐食防止剤

- 消泡剤

- その他のニッチ機能

- 形態別

- 固体

- 液体

- マイクロカプセル化

- 用途別

- 尿素

- 硝酸アンモニウム

- リン酸二アンモニウム(DAP)

- リン酸一アンモニウム(MAP)

- 硫酸アンモニウム

- トリプルスーパーリン酸(TSP)

- カリブレンド

- その他の特殊肥料

- 作物別

- 穀物

- 油糧種子

- 果物と野菜

- 芝生と観賞用植物

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- BASF SE

- Corteva Agriscience

- Clariant International Ltd

- KAO Corporation

- Koch Agronomic Services

- Arkema(ArrMaz)

- Dorf Ketal Company LLC

- Michelman Inc.

- Novochem Group

- Lanxess AG

- Croda International Public Limited Company(Cargill, Incorporated)

- Hubei Forbon Technology Co., Ltd.

- Jiangsu Kolod Food Ingredients Co., Ltd.

- TIMAC AGRO INDIA PRIVATE LIMITED

- Nutrien Ltd.

- CF Industries

- The Mosaic Company

- Yara International

- ADM

- ICL Group