|

|

市場調査レポート

商品コード

1851457

自動車用タイヤ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Automotive Tires - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用タイヤ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月07日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

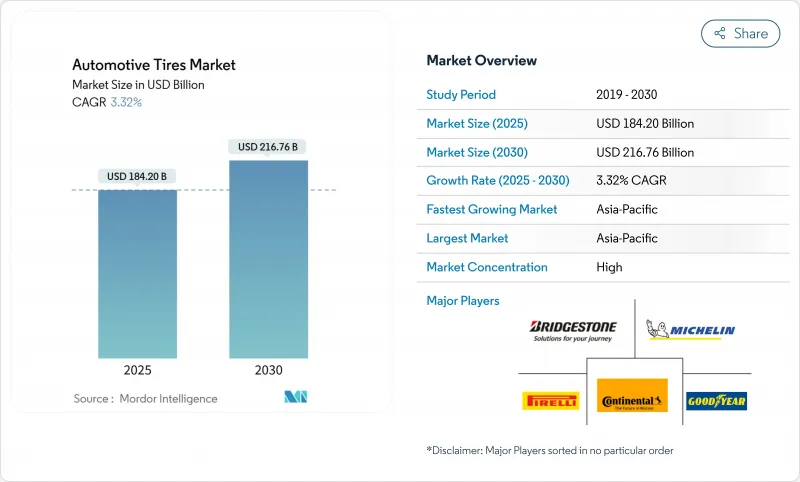

自動車用タイヤ市場は2025年に1,842億米ドル、2030年には2,167億6,000万米ドルに達し、CAGR 3.32%で拡大すると予測されます。

電気自動車の普及が超低騒音・低転がり抵抗製品の需要を高め、持続可能性政策が国内合成ゴムへの投資を促し、消費者の大径リム志向が平均販売価格を引き上げています。北米と欧州がコネクティビティとプレミアム性能を中心に革新を進める一方で、アジアの製造業の厚みと自動車保有台数の増加が地理的な軸を維持します。東南アジアのゴム葉病と欧州のカーボンブラック物流による供給サイドの圧力は、サプライチェーンの回復力の必要性を強調しています。しかし、自動車用タイヤ市場全体は、フリートが近代化し、データが豊富なスマートタイヤ契約が新たな収益源を解き放つにつれて、拡大を続けています。

世界の自動車用タイヤ市場の動向と洞察

電動化がもたらす超低騒音タイヤ需要

電動ドライブトレインはエンジンのマスキングノイズを除去し、タイヤと路面の相互作用を音響の最前線に位置づける。欧州連合(EU)の車外騒音規制の厳格化はこの傾向をさらに強め、自動車タイヤ市場の主流層もコンプライアンスと快適性のために同様の技術を要求しています。サプライヤーは、性能と規制を満たし、切望されるOE適合を確保し、原材料コストの上昇にもかかわらず価格規律を維持することができます。

中国における低RRタイヤ採用の義務化

Phase-6の燃費規制では、消費量の15%改善が義務付けられており、転がり抵抗にスポットが当てられています。国内およびグローバルブランドは、研究開発サイクルを18ヶ月に短縮し、燃費を8%向上させることができるシリカリッチコンパウンドを提供しています。中国のホモロゲーションで達成された利益は、アジアの幅広い生産に迅速に連鎖し、研究開発費を重複させることなく、自動車タイヤ市場全体のベースライン技術を向上させる。

東南アジアのゴム葉病の影響

ペスタロチオプシスの蔓延によりインドネシアではラテックス収量が減少し、天然ゴムのスポット価格が前年比33%上昇し、世界中のタイヤ工場のマージンが圧迫されています。罹患した木はタッピング成熟に達するまで10年を要するため、回復には時間がかかります。生産者はグアユールやロシアタンポポの原産地へ多様化しているが、商業的規模はまだ数シーズン先であり、中期的にはコスト圧力が続きます。

セグメント分析

2024年の自動車用タイヤ市場シェアはオールシーズン用が62.28%を占め、首位を維持した。冬用タイヤは小型ではあるが、欧州の安全義務化によって採用が拡大し、2025~2030年のCAGRは最速の4.24%を記録すると予測されます。夏用ラインは気温が常に高い地域で引き続き人気があり、オールテレイン/マッドテレインパターンはオフロード性能を重視するSUVオーナーを取り込んでいます。メーカーは現在、高シリカ・コンパウンドとアダプティブ・サイプをブレンドすることで、1つのトレッドで熱と小雪の両方に対応できるようにし、販売店の在庫の複雑さを軽減しています。

研究開発費は、電気自動車のニーズもターゲットにしています。発泡インサートはキャビンノイズを低減し、ゴム化学物質は氷点下でも柔軟性を維持するため、プレミアム冬用SKUはEVバイヤーにとって魅力的なものとなっています。配送バンにスリーピーク・マウンテン・スノーフレーク認証を指定するフリートも増えており、規制の範囲が拡大していることを物語っています。一方、データ主導のタイヤローテーション・サービスは、トレッドの寿命を延ばし、収益を付加価値の高い冬用交換パッケージへとシフトさせています。こうした相互作用の動向により、シーズンラインは単純な温度帯を超えた進化を遂げています。

ラジアル構造は、燃費効率、安定したハンドリング、長いトレッド寿命により、2024年の自動車用タイヤ市場シェアの86.24%を占めました。バイアスプライは、低速・高荷重のニッチ分野で存続しているが、その影響力は縮小の一途をたどっています。最も破壊的な進歩は非ニューマチック/エアレスセグメントで、建設、軍事、グランドメンテナンスの車両がパンクに強い稼働時間を求めているため、2030年まで年率5.67%の成長が予測されています。熱可塑性スポークと複合ウェブは、従来のラジアルタイヤとの転がり抵抗の差を縮めています。

パイロット・プログラムでは、パンク修理やダウンタイムを考慮に入れれば、エアレスタイヤはライフサイクルコストの節約につながることが示されており、OEMは次の開発サイクルで乗用車の試験を行うよう説得されています。ラジアルタイヤのサプライヤーは、強度を犠牲にすることなく質量を削減する強化ビードフィラーやスリムなスチールベルトで応え、EVのカーブウェイトが上昇する一方でシェアを守ることを目指しています。リサイクル性に関する規制は、使用後の処理を簡素化する単一素材のエアレス設計への関心をさらに高めています。その結果は、完全な代替ではなく、2本立ての技術革新競争です。

乗用車は2024年の販売台数の57.18%を占め、自動車用タイヤ市場規模の中核を固めました。SUVとクロスオーバーが引き続き台頭し、タイヤメーカーを高荷重指数と高径化に向かわせています。顕著な成長ストーリーはBEV専用タイヤであり、世界の電気自動車登録台数の急増に伴い、CAGR 10.92%の力強い成長が見込まれています。バッテリーの質量が増加し、瞬間的なトルクが加わることで、より強度の高いケーシング、シリカを多く含むトレッド、アコースティックダンパーなどの需要が高まる。

初期のプラットフォーム・エンジニアリングの段階で、プレミアム自動車メーカーは特注のBEVタイヤを共同開発することが増えており、ブランド独自の寸法を埋め込むことで交換需要を確保しています。買い替えチャネルでは、航続距離最適化マーケティングによって、コストに敏感な購買層が、充電1回あたりの走行距離が伸びると15~30%の価格プレミアムを受け入れるように説得しています。一方、小型商用車の電動化は、宅配便用の強化サイドウォールを備えた新しいSKUに火をつける。このような車両ミックスの進化は、サプライチェーン全体を通じて製品の複雑性を加速させる。

地域分析

アジアは2024年に自動車用タイヤ市場の54.66%を占め、2030年までのCAGRは6.51%と最も高いです。中国がその広大なOEM基盤を通じて地域の優位性を維持し、インドのSUVブームが18~20インチサイズとプレミアム輸入品の需要を促進しています。東南アジアのゴム葉病が天然ゴムの供給を制約しているため、合成ゴムの多様化とグアユールなどの代替作物が奨励されています。

北米は、成熟した補修用タイヤ販売と商用車へのスマートタイヤプラットフォームの急速な導入に支えられて第2位にランクされています。米国IRAが育成した国産合成ゴムの生産能力はサプライチェーンのリスクを低減し、EVの普及率は航続距離と騒音低減を優先する特殊タイヤラインに拍車をかけています。

欧州は引き続きプレミアムで持続可能な製品を優先しています。2024年のラベルの見直しは、消費者を高品位な代替品に誘導し、技術に富んだポートフォリオを持つブランドは報われます。しかし、カーボンブラックの物流課題はリードタイムを長くし、在庫コストを押し上げるため、回収カーボンブラックへの関心とサプライヤーとの緊密な連携を促しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場促進要因

- EU乗用車における電動化主導の超低騒音タイヤ需要

- 中国Phase-6燃料基準達成のための低RRタイヤ採用義務化

- 北米のラストマイル・フリートにおけるIoT対応スマートタイヤ契約

- 米国IRA傘下の合成ゴム生産能力が現地供給の安定性を高める

- インドSUVの18インチ超リムブームが台あたりASPを押し上げる

- EU-2024年のタイヤラベリング改正がAランクの買い替え需要を押し上げる

- 市場抑制要因

- 原材料コストを押し上げる東南アジアのゴム葉病

- 保証クレームを加速させるEVの過度な縁石重量

- 欧州におけるカーボンブラック輸送のボトルネック

- フッ素系離型剤の米国PFAS禁止が迫る

- バリュー/サプライチェーン分析

- 規制・技術的展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力/ 消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額・数量)

- タイヤタイプ別

- 夏

- 冬期

- オールシーズン

- オールテレイン/マッドテレイン

- タイヤデザイン別

- ラジアル

- バイアス

- ノンニューマチック/エアレス

- 車両タイプ別

- 乗用車

- SUVおよびクロスオーバー

- 小型商用車

- 大型商用トラック・バス

- 二輪車

- オフ・ザ・ロード&スペシャリティ(OTR、農業、鉱業、レース)

- 用途別

- オンロード

- オフロード(建設、鉱業、農業)

- エンドユーザー別

- OEM

- アフターマーケット(リプレイス&リトレッド)

- リムサイズ別

- 15インチ以下

- 15~20インチ

- 20インチ以上

- 推進力別

- 内燃自動車

- バッテリー電気自動車

- ハイブリッド車・燃料電池車

- 地域

- 北米

- 米国

- カナダ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- GCC

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Bridgestone Corporation

- Michelin Group

- Goodyear Tire & Rubber Company

- Continental AG

- Pirelli & C. SpA

- Hankook Tire & Technology

- Yokohama Rubber Co., Ltd.

- Sumitomo Rubber Industries

- MRF Ltd.

- Apollo Tyres

- JK Tyre & Industries

- Kumho Tire

- Toyo Tire Corporation

- Nexen Tire

- Zhongce Rubber Group

- Linglong Tire

- CEAT Ltd.

- Sailun Group

- Nokian Tyres

- Triangle Tire