|

市場調査レポート

商品コード

1686641

ペットフード:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ペットフード:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 499 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

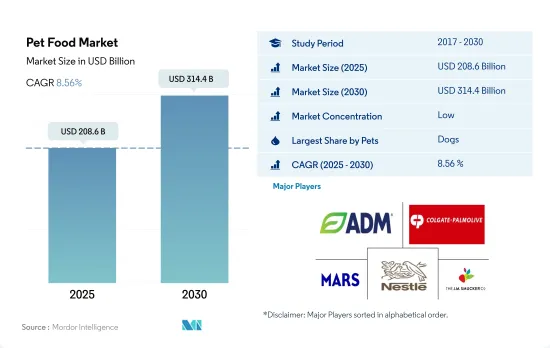

ペットフード市場規模は2025年に2,086億米ドルと推計され、2030年には3,144億米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは8.56%で成長します。

市販フードの利用率が高く、一人当たりの消費量が多いため、犬が市場を独占する

- 世界のペットフード市場は、世界的にペットの飼育が増加していることから、プラスの動向を示しています。市場は2017年から2022年の間に59.4%の成長を示しました。この成長は、ペットの人間化傾向の増加、ペットのプレミアム化、市販フードの給餌、2017年から2022年にかけてのペット数の13.0人増に起因しています。

- 世界的に、犬はペットの親が採用する主要なペットです。2022年、犬は世界のペットフード市場で最大のシェアを占め、2022年の市場価値は800億3,000万米ドルでした。2029年には1,566億米ドルに達すると予測されています。この高いシェアは、家庭料理から市販フードに移行する飼い主が多いこと、他のペットに比べて犬の食事ニーズが高いこと、犬の飼育数が多いことによる。例えば、2022年の犬の飼育数は6億450万人であったのに対し、猫の飼育数は世界全体で4億820万人でした。

- 猫セグメントはペットフードの2番目の主要消費者で、2022年には32.3%を占め、予測期間中のCAGRは7.9%と予測されます。この成長は、2017年から2022年の間に猫の飼育数が18.8%大幅に増加したこと、次いで比較的メンテナンスの必要性が低いことから猫のコンパニオン人気が高まったことによる。

- その他のペットセグメントは、鳥類、小型哺乳類、げっ歯類、観賞魚で構成されています。同年の人口シェアが35.0%であったにもかかわらず、2022年の市場シェアは19.0%でした。この低いシェアは、犬猫に比べて体のサイズが小さいため、必要なフード量が少ないためです。

- 業務用フード使用の増加、ペットの人間化、世界のペット数の増加が、予測期間中にCAGR 8.7%で市場を牽引すると予測される要因です。

北米は、ペット数の多さ、可処分所得の高さ、ペットの人間化という一般的な動向により、世界のペットフード市場を独占しています。

- 2022年、北米は世界のペットフード市場において最大の地域市場に浮上し、その市場規模は774億3,000万米ドルでした。米国とメキシコは、これらの国々における高いペット飼育率により、北米ペットフード市場に大きく貢献しています。北米市場は、2017年から2022年の間に74.7%の増加したが、これはペットの導入の増加、可処分所得の増加、ペットの人間化の一般的な動向によるものです。

- 欧州は、2022年に477億4,000万米ドルと評価され、同市場で2番目に大きな地域シェアを占めています。この市場は、原材料、カスタマイズされた食品、グレインフリー、オーガニックフードに対する意識の高まりによって大きく牽引されています。欧州は、2017年の2億9,050万人から2022年には3億2,440万人に達する同地域のペット数の増加により、2017年から2021年にかけて23.6%の大幅な成長を記録しました。

- アジア太平洋諸国では近年、ペットの人間化が著しく進み、プレミアムペットフード製品に対する消費者の嗜好が高まっています。同地域のペットオーナーは市販のペットフード製品を選ぶようになっており、これが同地域の市場成長を促進しています。こうした要因により、アジア太平洋地域のペットフード市場は2022年に293億6,000万米ドルに達しました。

- アフリカと南米は市場で最も急成長している地域で、市場推計・予測期間中のCAGRはそれぞれ12.2%と12.1%です。これは主に、ペット数が増加していることと、ペットの人間化の動向の高まりに伴い、多くの飼い主が家庭料理から市販のペットフードに移行していることによる。

- 世界のペット数の増加、可処分所得の増加、ペットのヒューマニゼーションの動向は、予測期間中に市場を牽引すると予測されます。

世界のペットフード市場動向

猫は、コンパニオンとしての猫の採用が増加しているため、世界的に採用ペットの第2位であり、猫を飼うことの利点に関する意識の高まりが猫市場を牽引しています。

- 世界的に、猫は犬に比べ飼育頭数が少ないです。2022年、猫の飼育数は24.8%を占め、2017年から2022年の間に19.2%増加しました。欧州では歴史的な時代から猫を幸運や幸運のシンボルと考えているため、特にペットとしての猫の飼育数が多い主要国であるロシアでのシェアが高くなります。世界的に猫の飼育数が高い伸びを示したのは、ペットの人間化が進んだためです。猫は犬よりも生活スペースが少なくて済み、世話をする人間がいない間、家の中で一匹で長く留まることができます。例えば、2017年から2022年にかけて、ロシアと米国の猫の親を含むペットの親の70%以上が、猫を家族、友人、または子供とみなしています。

- COVID-19の大流行時には、人々が屋内で過ごさざるを得なくなり、猫も閉塞感を感じることなく屋内で過ごすことができたため、猫の養子縁組が大幅に増加しました。猫は犬よりも無口です。米国では、在宅勤務の文化が仲間を求めることにつながり、ペットを飼う人の多くがミレニアル世代であったため、パンデミック時にペットとして猫を飼う人が増加しました。例えば2022年には、米国ではミレニアル世代の33%がペットの親となっています。大流行中の猫の採用率が高いことから、ペットフード市場の成長に長期にわたってプラスの影響を与えると予想されます。

- 猫の採用や購入の増加、ペットの人間化の増加といった要因は、ペットの猫の飼育数を増加させると予想され、予測期間中のペットフード市場の成長にさらに貢献すると思われます。

プレミアム化が進み、様々な流通チャネルで多数のペット用品を入手できるようになったことが、世界のペット支出の増加に寄与しています。

- 世界のペット支出は増加傾向にあり、2017年から2022年にかけて24.8%増加しました。プレミアム化の進展と健康への関心の高まりが理由です。犬のペット支出シェアは高く、2022年には39.4%を占めるが、これは主に猫よりもペットフードの消費量が多く、プレミアムペットフードが人気のフードであるためです。

- ペットの親はペットの健康に気を配るため、ペット支出額の大半をペットフードに投資しています。例えば、米国では2022年にペットフードがペット費用の42.4%を占めました。他の見栄えの良いペットとのより良い社会化のために、ペットのグルーミング、ペットのデイケア、ペットの散歩などの他のサービスを提供することが増加しています。この動向は北米、欧州、アジア太平洋で顕著です。人々はまた、ペットに高品質のフードを食べさせたいと考え、プレミアム価格を支払うことを厭わないため、プレミアムペットフードを購入しています。米国では、2022年にペットの親の約40%がプレミアム・ペットフードを購入し、香港のキャットフード市場では、2022年にプレミアム・ペットフード・セグメントがペットフード売上の75%を占める。

- 特にCOVID-19の大流行後は、ウェブサイトで入手できるペット用品の数が多いため、ペットフードの購入先がオフラインの店舗からオンラインショップへと変化しています。しかし、オランダなど一部の国では、製品の品質の高さから、ペットの親はペットショップからの購入を好みます。例えば米国では、フードを含むペットケアのオンライン販売は、2020年の32%から2022年には40%に増加しました。プレミアム化と健康への関心の高まりが、予測期間中にペットの支出を増加させると予想される要因です。

ペットフード業界の概要

ペットフード市場は細分化されており、上位5社で31.55%を占めています。この市場の主要企業は以下の通り。 ADM, Colgate-Palmolive Company(Hill's Pet Nutrition Inc.), Mars Incorporated, Nestle(Purina)and The J. M. Smucker Company(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他のペット

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブプロダクト別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェット・ペットフード

- ペット用栄養補助食品・サプリメント

- サブプロダクト別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用おやつ

- サブプロダクト別

- カリカリおやつ

- デンタル・トリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のおやつ

- ペット用動物飼料

- サブプロダクト別

- 糖尿病

- 消化器過敏症用

- オーラルケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンライン・チャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 地域

- アフリカ

- 国別

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- 台湾

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ロシア

- スペイン

- 英国

- その他の欧州

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米

- 南米

- 国別

- アルゼンチン

- ブラジル

- その他の南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- Heristo Aktiengesellschaft

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

- The J. M. Smucker Company

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 53527

The Pet Food Market size is estimated at 208.6 billion USD in 2025, and is expected to reach 314.4 billion USD by 2030, growing at a CAGR of 8.56% during the forecast period (2025-2030).

Dogs dominate the market due to higher usage of commercial foods and high per capita consumption

- The global pet food market shows a positive trend as there is an increasing pet adoption globally. The market witnessed a growth of 59.4% between 2017 and 2022. This growth was attributed to the increasing pet humanization trend, pet premiumization, feeding of commercial foods, and the rise in pet population by 13.0 between 2017 and 2022.

- Globally, dogs are the major pets adopted by pet parents. In 2022, they accounted for the largest share of the global pet food market, accounting for a market value of USD 80.03 billion in 2022. They are anticipated to reach USD 156.60 billion in 2029. This higher share is due to a significant number of pet owners shifting from home-cooked food to commercial food, the higher dietary needs of dogs compared to other pets, and the higher dog population. For instance, the dog population was 604.5 million in 2022, whereas the cat population was 408.2 million globally.

- The cats segment was the second major consumer of pet food, accounting for 32.3% in 2022, which is estimated to register a CAGR of 7.9% during the forecast period. This growth is due to the significant increase in the cat population by 18.8% between 2017 and 2022, followed by the rise in popularity of cat companionship due to their comparatively low maintenance requirements.

- The other pets segment consists of birds, small mammals, rodents, and ornamental fish. They accounted for 19.0% of the market in 2022 despite the 35.0% population share in the same year. This lower share was due to their smaller body size, resulting in lower food requirements compared to cats and dogs.

- The rise in commercial food usage, pet humanization, and the growing population of pets worldwide are the factors anticipated to drive the market at a CAGR of 8.7% during the forecast period.

North America dominates the global pet food market due to a high pet population, higher disposable incomes, and the prevailing trend of pet humanization

- In 2022, North America emerged as the largest regional market in the global pet food market, with a value of USD 77.43 billion. The United States and Mexico are the major contributors to the North American pet food market due to the high pet ownership rates in these countries. The North American market witnessed an increase of 74.7% between 2017 and 2022, driven by the increasing adoption of pets, rising disposable income, and the prevailing trend of pet humanization.

- Europe holds the second-largest regional share of the market, valued at USD 47.74 billion in 2022. This market is highly driven by the increasing awareness of ingredients, customized food products, grain-free, and organic food. Europe registered significant growth of 23.6% between 2017 and 2021, owing to the increasing pet population in the region, which reached 324.4 million in 2022, rising from 290.5 million in 2017.

- The Asia-Pacific countries have witnessed significant increases in pet humanization and consumer preference for premium pet food products in recent years. Pet owners in the region are increasingly opting for commercial pet food products, which is driving market growth in the region. Due to these factors, the Asia-Pacific pet food market reached USD 29.36 billion in 2022.

- Africa and South America are the fastest-growing regions in the market, with estimated CAGRs of 12.2% and 12.1%, respectively, during the forecast period. This is mainly due to their growing pet populations and a large number of pet owners shifting from home-cooked food to commercial pet food, in line with the rising trend of pet humanization.

- The growing pet population, increased disposable incomes, and pet humanization trends globally are estimated to drive the market during the forecast period.

Global Pet Food Market Trends

Cats are the second-largest type of adopted pets globally due to the growing adoption of cats as companions, and increasing awareness about the benefits of owning a cat is driving the cat market

- Globally, cats are being less adopted as compared to dogs. In 2022, the cat population accounted for 24.8%, increasing by 19.2% between 2017 and 2022. The share of cats will be higher in Europe as they consider them a symbol of luck or fortune since historical times, particularly in Russia, a major country with a high population of cats as pets. The high growth of the cat population globally was because of the rise in pet humanization. Cats require less space to live than dogs and can stay alone in a home for a longer time while no human is available to care for the cat. For instance, between 2017 and 2022, more than 70% of pet parents, including cat parents in Russia and the United States, considered cats as family members, friends, or children.

- Cat adoption significantly increased during the COVID-19 pandemic as people had to stay indoors, and cats could stay indoors without feeling cooped up. Cats are more silent than dogs. The United States witnessed higher adoption of cats as pets during the pandemic because of the work-from-home culture, leading to a demand for companionship, with the higher number of pet owners being millennials. For instance, in 2022, 33% of millennials were pet parents in the United States. The higher adoption of cats during the pandemic is expected to positively impact the pet food market growth for a longer period.

- Factors such as an increase in the adoption and purchase of cats and an increase in pet humanization are expected to boost the pet cat population, which will further help in the growth of the pet food market during the forecast period.

The rise in premiumization and availability of a large number of pet products on various distribution channels are contributing to the increase in pet expenditure globally

- Globally, there is a trend of increase in pet expenditure, and it increased by 24.8% between 2017 and 2022 because of the rise in premiumization and growing health concerns. Dogs have a higher share of pet expenditure, accounting for 39.4% in 2022, mainly due to the higher consumption of pet food than cats and premium pet food being the popular food choice.

- Pet parents invest most of their pet expenditure in pet food as they are concerned about their pets' well-being. For instance, pet food accounted for 42.4% of pet expenses in the United States in 2022. There has been a rise in providing other services such as pet grooming, pet daycare, and pet walking for better socialization with other good-looking pets. This trend has been majorly witnessed in North America, Europe, and Asia-Pacific. People are also purchasing premium pet food as they want their pets to consume high-quality food and are willing to pay premium prices. In the United States, about 40% of pet parents purchased premium pet food in 2022, and in Hong Kong's cat food market, the premium pet food segment accounted for 75% of the pet food sales in 2022.

- There is a change in purchasing pet food from offline stores to online stores, especially after the COVID-19 pandemic, because of the large number of pet products available on websites. However, in some countries, such as the Netherlands, pet parents prefer purchasing from pet stores due to the quality of their products. For instance, in the United States, online sales of pet care, including food, increased from 32% in 2020 to 40% in 2022. Premiumization and growing concern about health are the factors expected to increase pet expenditure during the forecast period.

Pet Food Industry Overview

The Pet Food Market is fragmented, with the top five companies occupying 31.55%. The major players in this market are ADM, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Mars Incorporated, Nestle (Purina) and The J. M. Smucker Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Region

- 5.4.1 Africa

- 5.4.1.1 By Country

- 5.4.1.1.1 South Africa

- 5.4.1.1.2 Rest of Africa

- 5.4.2 Asia-Pacific

- 5.4.2.1 By Country

- 5.4.2.1.1 Australia

- 5.4.2.1.2 China

- 5.4.2.1.3 India

- 5.4.2.1.4 Indonesia

- 5.4.2.1.5 Japan

- 5.4.2.1.6 Malaysia

- 5.4.2.1.7 Philippines

- 5.4.2.1.8 Taiwan

- 5.4.2.1.9 Thailand

- 5.4.2.1.10 Vietnam

- 5.4.2.1.11 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 By Country

- 5.4.3.1.1 France

- 5.4.3.1.2 Germany

- 5.4.3.1.3 Italy

- 5.4.3.1.4 Netherlands

- 5.4.3.1.5 Poland

- 5.4.3.1.6 Russia

- 5.4.3.1.7 Spain

- 5.4.3.1.8 United Kingdom

- 5.4.3.1.9 Rest of Europe

- 5.4.4 North America

- 5.4.4.1 By Country

- 5.4.4.1.1 Canada

- 5.4.4.1.2 Mexico

- 5.4.4.1.3 United States

- 5.4.4.1.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 By Country

- 5.4.5.1.1 Argentina

- 5.4.5.1.2 Brazil

- 5.4.5.1.3 Rest of South America

- 5.4.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 General Mills Inc.

- 6.4.5 Heristo Aktiengesellschaft

- 6.4.6 Mars Incorporated

- 6.4.7 Nestle (Purina)

- 6.4.8 PLB International

- 6.4.9 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.10 The J. M. Smucker Company

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms