|

市場調査レポート

商品コード

1686582

殺菌剤:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 殺菌剤:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 332 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

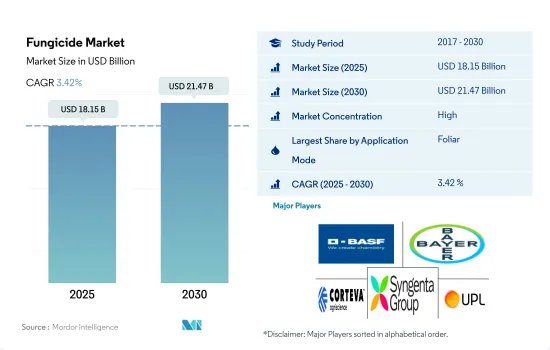

殺菌剤の市場規模は2025年に181億5,000万米ドルと予測され、2030年には214億7,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは3.42%で成長します。

真菌病害の増加が、さまざまな散布方法による殺菌剤の需要を牽引しています。

- 殺菌剤は、特定の要件や病害に応じて、さまざまな方法で散布されます。多様な散布方法は、様々な農業条件下で殺菌剤を効果的に散布する上で重要な役割を果たします。

- 2022年には、葉面散布が殺菌剤セグメントにおいて60.1%の最大市場シェアを占めました。この方法は、葉上の病原菌を直接標的にすることで、葉面真菌病に対する効率的な保護を提供するため、非常に好まれています。葉面散布は殺菌剤の植物組織への迅速な浸透・吸収を促進し、真菌病原体に対する効果的な作用を保証します。

- 殺菌剤の種子処理は、植物の生育初期における真菌感染への対応において重要な役割を果たします。これらの処理は種子の周囲に保護シールドを作り、種子の腐敗、苗立枯病、湿害、根腐れなどの様々な病害を効果的に予防します。特に、世界の殺菌剤市場において、殺菌剤種子処理剤は2022年に14.1%という大きな市場シェアを占めています。これは、植物の健康を守り、作物の定着を促進する上で、殺菌剤が大きく貢献していることを示しています。

- 散布方法の選択は、対象とする特定の病害、作物の種類、病害の発生段階、設備の有無など、複数の要因に影響されます。殺菌剤市場は拡大すると予測され、2023~2029年までの予測期間中の推定CAGRは3.8%です。この成長は、植物病害と闘い農業生産性を向上させる戦略の進化を反映しています。

真菌病原体による作物蔓延の増加が殺菌剤の採用を高めています。

- 菌類病害による作物損失の増加と世界の食糧安全保障に対する懸念の高まりが、殺菌剤のような作物保護化学品の採用を高めています。世界レベルでは、農家は作物の10~23%を真菌病で失っています。集約的な農業慣行の採用、単一農法、干ばつや熱波のような気候条件の変化は、農業生産における殺菌剤の高い利用をもたらした様々な真菌病の増加につながります。世界の殺菌剤市場は、2022年に163億7,000万米ドル、190万トンの消費量で、世界の作物保護化学品市場全体の18.1%の市場シェアを占めました。

- 南米の殺菌剤市場価値は30.3%を占め、市場価値は49億6,000万米ドルでした。市場シェアが高いのは、農作物への干ばつや熱波の影響により真菌病が蔓延し、農作物の損失が発生したためであり、その結果、同地域では殺菌剤の利用率が高まりました。同年、ブラジルは南米の殺菌剤市場の59.4%を占めましたが、主要作物である米、小麦、大豆が真菌病に非常にかかりやすいためです。

- 欧州の殺菌剤市場金額は、2022年の世界の殺菌剤市場金額の28.4%を占めました。ブドウ晩枯病、ブドウ早期疫病、うどんこ病、べと病、フザリウム枯病、セプトリア病、細菌性疫病は、この地域で栽培されている主要作物を襲う一般的な病害です。スペイン、ロシア、フランス、イタリアが主要な殺菌剤消費国で、それぞれ18.1%、15.0%、14.3%、12.5%の市場シェアを占めています。欧州では気温の上昇が様々な真菌病原菌の増殖に有利となっています。

世界の殺菌剤市場動向

年間平均経済損失の増加により、農家はより多くの殺菌剤を使用するようになっています。

- 真菌病は作物生産に大きな脅威をもたらし、穀物、果物、野菜、観葉植物など幅広い作物に影響を及ぼしています。2017年には1ヘクタール当たり1.4kgであった平均殺菌剤消費量が、2022年には1.6kgへと年々増加しているのは、病害を効果的に管理・防除し、作物への被害を最小限に抑え、最適な収量を確保する必要性が背景にあります。

- 調査対象地域の中で、2022年に化学殺菌剤のヘクタール当たりの年間散布量が最も多かったのは欧州で、農地1ヘクタール当たり2.5kgでした。これは、高付加価値作物を中心とした集約農法と単一栽培によるものです。集約的な農業は通常、1つの土地に作物を密集させるため、より多くの病原菌を引き寄せ、土壌養分を枯渇させ、植物を病原菌に感染しやすくします。そのため、作物を保護し収穫量を維持するために、化学殺菌剤を多用することになります。

- 殺菌剤の使用量では欧州に次いで南米が多く、2022年の1ヘクタール当たりの平均散布量は1.7kgでした。2022年の殺菌剤の使用量は、チリが4.1kg/ヘクタールで同地域で最も多くなりました。この高い使用量は、チリの特定の地域が高湿度、降雨量、気温の変動により真菌病害の発生を助長する気候条件を持っているためです。アジア太平洋、北米、中東のような他の地域も、殺菌剤の使用量が多いです。

- 食糧農業機関が提供したデータによると、殺菌剤が大量に使用されているにもかかわらず、真菌病は平均で約2,200億米ドルの経済損失をもたらしています。気候条件の変化や病害の頻発といった状況が状況を悪化させ、散布量を増加させる可能性さえあります。

マンコゼブは他の殺菌剤に比べて幅広い活性スペクトルを持っています。

- テブコナゾールはトリアゾール系の殺菌剤です。さまざまな作物の真菌病防除に広く使用されています。テブコナゾールは、真菌の細胞膜の重要な成分であるエルゴステロールの生合成を阻害することで効果を発揮します。2022年の価格は8,700米ドルでした。

- マンコゼブはジチオカルバミン酸塩の化学クラスに属する殺菌剤です。ジャガイモ、トマト、ブドウ、バナナなどの作物で、晩枯病、うどんこ病、初期疫病、炭そ病などの真菌性病害の防除によく使われます。Mancozebはその他の殺菌剤に比べ幅広い活性スペクトルを持ち、真菌細胞内の複数の部位に作用するため、より効果的です。Mancozebの2022年の価格は7,800米ドルでした。

- アゾキシストロビンはストロビルリン系の殺菌剤で、価格はトン当たり4,600米ドルです。アゾキシストロビンは、様々な作物の真菌性病害を防除するために広く使用されています。アゾキシストロビンは、真菌細胞のミトコンドリア呼吸を阻害することで、真菌の成長と繁殖を阻害し、最終的に死滅させる。

- メタラキシルは、晩枯病、べと病、根腐病などの真菌病害の防除に広く使用されており、価格はトン当たり4,400米ドルです。メタラキシルは、真菌細胞のRNA形成を阻害することで効果を発揮します。この阻害により必須タンパク質の合成が妨げられ、真菌の成長と繁殖が阻害されます。

- プロピネブとジラムはジチオカルバミン酸塩に属します。2022年の価格はそれぞれトン当たり3,500米ドル、3,300米ドルでした。過去期間中に価格がわずかに上昇したのは、これらの製品に対する需要の高まりと、生産に使用される原材料の高騰によるものです。

殺菌剤業界の概要

殺菌剤市場はかなり統合されており、上位5社で81.72%を占めています。この市場の主要企業はBASF SE、Bayer AG、Corteva Agriscience、Syngenta Group、UPL Limitedです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- チリ

- 中国

- フランス

- ドイツ

- インド

- インドネシア

- イタリア

- 日本

- メキシコ

- ミャンマー

- オランダ

- パキスタン

- フィリピン

- ロシア

- 南アフリカ

- スペイン

- タイ

- ウクライナ

- 英国

- 米国

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 用途別

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ別

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用植物

- 地域別

- アフリカ

- 国別

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他欧州

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- 国別

- アルゼンチン

- ブラジル

- チリ

- その他南米諸国

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 52906

The Fungicide Market size is estimated at 18.15 billion USD in 2025, and is expected to reach 21.47 billion USD by 2030, growing at a CAGR of 3.42% during the forecast period (2025-2030).

Rising fungal diseases are driving the demand for fungicides in various application methods

- Fungicides may be applied using a variety of methods, depending on the specific requirements and diseases. Diverse application methods play a crucial role in effectively applying fungicides across various agricultural conditions.

- In 2022, foliar application dominated the fungicide segment, holding the largest market share of 60.1%. This method is highly preferred as it provides efficient protection against foliar fungal diseases by directly targeting the pathogens on the leaves. The foliar application facilitates swift penetration and absorption of fungicides into the plant tissues, ensuring their effective action against fungal pathogens.

- Fungicide seed treatments play a crucial role in addressing fungal infections during the initial phases of plant growth. These treatments create a protective shield around seeds, effectively preventing various diseases like seed rots, seedling blights, damping off, and root rots. Notably, within the global fungicide market, fungicide seed treatments accounted for a significant market share of 14.1% in 2022. This highlights their substantial contribution to safeguarding plant health and promoting successful crop establishment.

- The selection of the application mode is influenced by multiple factors, encompassing the particular disease being targeted, the type of crop, the stage of disease development, and the availability of equipment. The fungicide market is anticipated to expand, projecting an estimated CAGR of 3.8% during the forecast period spanning from 2023 to 2029. This growth reflects the ongoing evolution of strategies to combat plant diseases and enhance agricultural productivity.

Growth in the crop infestations by the fungal pathogens raise the fungicides adoption

- Increasing crop losses due to fungal diseases and growing concerns over global food security raise the adoption of crop protection chemicals like fungicides. At the Global level, the farmers are losing 10-23% of their crops to fungal diseases. Adoption of intensive agricultural practices, monocultural practices, and changing climatic conditions like drought and heatwaves lead to the growth of various fungal diseases, which resulted in higher utilization of fungicides in agricultural production. The Global fungicide market accounted for 18.1% market share in the overall Global crop protection chemical market value with USD 16.37 billion in 2022 with a consumption volume of 1.9 million metric tons.

- South American fungicide market value accounted for 30.3%, with a market value of USD 4.96 billion. The higher market share is attributed to the drought and heatwave effect on the crops, which led to the proliferation of fungal diseases and crop losses, resulting in higher utilization of fungicides in the region. In the same year, Brazil accounted for 59.4% of the South American fungicide market, with rice, wheat, and soybeans being the major crops grown and are highly susceptible to fungal diseases.

- Europe's fungicide market value accounted for 28.4% of the Global fungicide market value in 2022. Grape late blight, early blight, powdery mildew, downy mildew, Fusarium wilting, Septoria, and bacterial blight are the common diseases attacking the major crops grown in the region. Spain, Russia, France, and Italy are the major fungicide-consuming countries with a market value share of 18.1%, 15.0%, 14.3%, and 12.5%, respectively. In Europe, temperature increases favor the various fungal pathogens' growth.

Global Fungicide Market Trends

Increasing average annual economic losses are driving farmers to use a higher amount of fungicides

- Fungal diseases pose a significant threat to crop production, affecting a wide range of crops, including cereals, fruits, vegetables, and ornamentals. The rise in the average per-hectare fungicide consumption over the years from 1.4 kg per ha in 2017 to 1.6 kg per ha in 2022 was driven by the need to manage and control diseases effectively, minimizing crop damage and ensuring optimum yields.

- Among the regions studied, in 2022, Europe had the highest per-hectare application of chemical fungicides annually, with 2.5 kg per ha of agricultural land. This was due to its intensified farming practices and monocultures with a focus on high-value crops. Intensive farming usually attracts more pathogens due to overcrowding of crops on a piece of land, depleting soil nutrients and making the plants more susceptible to pathogens. This leads to the overuse of chemical fungicides to protect crops and maintain crop yields.

- Europe is followed by South America in fungicide usage, with an average per-hectare application of 1.7 kg/ha in 2022. Chile had the highest per-hectare consumption of fungicides at 4.1 kg/ha in the region in 2022. This high usage was due to certain regions in Chile having climatic conditions that are conducive to fungal disease development due to high humidity, rainfall, and temperature fluctuations. Other regions like Asia-Pacific, North America, and the Middle East also have a significant amount of fungicidal application.

- According to the data provided by the Food and Agriculture Organization, fungal diseases cause an average economic loss of around USD 220.0 billion despite abundant usage of fungicides. Circumstances like changing climatic conditions and frequent disease outbreaks may even worsen the situation, increasing the application rates.

Mancozeb has a broad spectrum of activity compared to other fungicides

- Tebuconazole is a fungicide belonging to the chemical class of triazoles. It is widely used to control fungal diseases in various crops. Tebuconazole works by inhibiting the biosynthesis of ergosterol, a critical component of fungal cell membranes. This was priced at USD 8.7 thousand in 2022.

- Mancozeb is a fungicide belonging to the chemical class of dithiocarbamates. It is commonly used to control fungal diseases like late blight, downy mildew, early blight, and anthracnose in crops like potatoes, tomatoes, grapes, and bananas. Mancozeb has a broad spectrum of activity compared to other fungicides and acts on multiple sites within the fungal cell, making it more effective. Mancozeb was priced at USD 7.8 thousand in 2022.

- Azoxystrobin is a fungicide belonging to the chemical class of strobilurins and was priced at USD 4.6 thousand per metric ton. It is widely used to control fungal diseases in various crops. Azoxystrobin works by inhibiting the mitochondrial respiration in fungal cells, resulting in their inability to grow and reproduce and eventually causing their death.

- Metalaxyl is widely used to control fungal diseases such as late blight, downy mildew, and root rot and was priced at USD 4.4 thousand per metric ton. Metalaxyl works by inhibiting the formation of RNA in fungal cells. This disruption prevents the synthesis of essential proteins, leading to the inhibition of fungal growth and reproduction.

- Propineb and Ziram belong to the chemical class of dithiocarbamates. They were priced at USD 3.5 thousand and 3.3 thousand per metric ton, respectively, in 2022. These slight increases in the prices during the historical period were due to the growing demand for these products and the escalating costs of raw materials used in their production.

Fungicide Industry Overview

The Fungicide Market is fairly consolidated, with the top five companies occupying 81.72%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 Chile

- 4.3.6 China

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Myanmar

- 4.3.15 Netherlands

- 4.3.16 Pakistan

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Ukraine

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms