冷凍潤滑油:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Refrigeration Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1686243

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

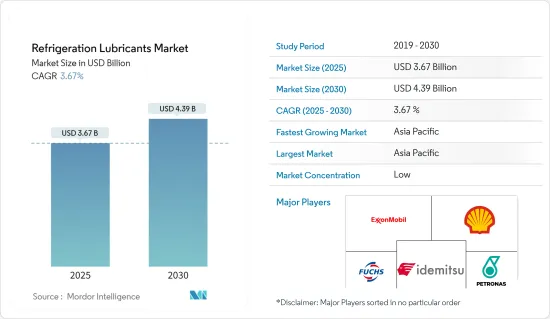

冷凍潤滑油市場規模は2025年に36億7,000万米ドルと推定・予測され、予測期間(2025年~2030年)のCAGRは3.67%で、2030年には43億9,000万米ドルに達すると予測されます。

COVID-19の発生により、世界中で全国的な封鎖、製造活動やサプライチェーンの混乱、生産停止が発生し、調査対象の市場に悪影響を与えました。しかし、2021年には状況が回復し始め、予測期間中に市場の成長軌道が回復することが期待されます。

主なハイライト

- エネルギー効率に最適化された新世代冷凍用潤滑油の出現、世界のHVACR産業における勢いの増加、自動車産業の回復が冷凍用潤滑油市場の成長を牽引すると予想されます。

- その反面、絶え間ない規制改正による既存冷媒の段階的廃止が市場成長の妨げになると予想されます。

- ナノ潤滑技術への注目の高まりと極低温用途への需要の増加は、調査された市場に新たな機会をもたらすと予想されます。

- アジア太平洋は世界市場を独占し、インドや中国などの国々からの消費が最も大きいです。

冷凍潤滑油市場の動向

世界のHVACR産業における勢いの増加

- 空調(AC)ユニットは、密閉されたエリアの湿度と気温を調整するように設計されています。エアコンの主要部品は、コンプレッサー、蒸発器、膨張弁、凝縮器です。潤滑剤は、パイプラインの腐食などの副作用を低減し、一般的な冷凍ガスとのより良い互換性を提供します。

- 冷凍用潤滑剤には、熱の除去、可動部品の潤滑、シール剤としての役割、コンプレッサーの重要部品の冷却など、複数の目的があります。

- 国際エネルギー機関(IEA)によると、2021年にはあらゆる建築物の最終用途の中で空間冷房需要が最も高い年間成長率を記録し、建築物部門の最終電力消費量(約2,000 TWh)の16%近くを占めるようになりました。これは予測期間中、空調用潤滑油市場に利益をもたらすと予想されます。

- インド政府は2021年11月、白物家電の生産連動型奨励金(PLI)制度で26件の申請を選定しました。これらはエアコン(AC)製造向けで、3,898カロールインドルピーの投資が約束されています。この取り組みにより、国内での生産が促進され、冷凍用潤滑油市場にも好影響を与えると思われます。

- 電気自動車の動向の高まりは、冷凍潤滑油市場をさらに下支えする可能性が高いです。2021年の電気自動車生産は中国がトップでした。中国乗用車協会(CPCA)によると、同国の2021年の販売台数は330万台を超え、2020年比で169%増となりました。

- インドの電気自動車市場は、2021年に48%以上を占める二輪車セグメントが主な牽引役となっています。道路交通・高速道路省(MoRTH)によると、国内で販売された電気自動車は32万9,190台で、2020年の販売台数と比較すると168%の増加となっています。

- 上記の要因は、冷凍潤滑油市場にポジティブな影響を与えると思われます。

アジア太平洋が市場を独占する見込み

- アジア太平洋は冷凍潤滑油の最大市場です。冷凍用潤滑油の需要が増加しているのは、家庭用および産業用空調システムの使用が増加しているためです。

- 中国は世界最大の自動車ハブです。OICAによると、2021年の同国の自動車生産台数は全体で2,608万2,220台となり、2020年から3%増加しました。

- 中国の大手電気自動車メーカーには、テスラ、BYD社、ニオ社などがあります。同国における電気自動車の需要拡大が、自動車コンプレッサー用冷凍潤滑油市場を牽引しています。

- OICAの報告書によると、2021年第1四半期から第3四半期までの欧州の生産台数は1,188万6,776台であるのに対し、中国は同期間に1,824万2,588台を生産しました。そのため、自動車のAC需要は増加し続けています。

- 韓国自動車技術研究院(KAII)が収集したデータによると、2021年1~9月の韓国の電気自動車販売台数は96%増の7万1,006台に急増しました。欧州、アジア太平洋、南北アメリカの輸入経済圏からの需要増加により、販売台数はさらに増加すると予想されます。

- 2021年、インドの第1~3四半期の電気自動車生産台数は328万9,683台で、2020年から53%の大幅増となりました。自動車部門の成長により、予測期間中の市場拡大が期待されます。

- インドは、米国、ロシア、中国に次いで、世界で最も大規模な鉄道システムで4位にランクされており、線路の長さは123,542km、路線の長さは67,415km、駅の数は7,300以上です。

- 世界第2位の人口を誇るこの国の鉄道網では、13,523本の旅客列車と9,146本の貨物列車が定期的に運行されています。鉄道は2020~2021年度に12億3,000万トンの貨物を運びました。

- 以上のような要因から、アジア太平洋が今後数年間は市場を独占すると予想されます。

冷凍潤滑油産業の概要

冷凍潤滑油市場は、各国の複数の排ガス規制のために細分化が進んでいます。市場の主要企業(順不同)には、エクソンモービル、シェルPLC、フックス、出光興産、PETRONAS Lubricants Internationalが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- エネルギー効率に最適化された新世代冷凍用潤滑油の登場

- 世界のHVACR産業における勢いの増加

- 自動車産業の回復

- 抑制要因

- 恒常的な規制改正による既存冷媒の段階的廃止

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- ベースオイル別

- 鉱物油系潤滑油

- パラフィン系オイル

- ナフテン系オイル

- 芳香族油

- 合成潤滑油別

- 合成炭化水素

- ポリアルファオレフィン(PAO)

- アルキル化芳香族

- ポリブテン

- エステル別

- ジエステル

- ポリオールエステル

- リン酸エステル

- ポリマーエステル

- ポリアルキレングリコール(PAG)

- その他の合成潤滑油

- 鉱物油系潤滑油

- 用途別

- 空調

- 輸送

- 自動車

- その他の輸送手段(鉄道、航空、船舶)

- その他の空調用途(据置型)

- 冷凍(家庭用、工業用、極低温用)

- 空調

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- BP PLC

- BVA Oil

- Chevron Corporation

- China National Petroleum Corporation

- China Petroleum & Chemical Corporation(SINOPEC Group)

- CPI Fluid Engineering

- ENEOS Corporation

- ExxonMobil Corporation

- Fuchs

- HP Lubricants

- Idemitsu Kosan Co. Ltd

- Isel

- Kluber Lubrication

- Kuwait Petroleum

- Matrix Specialty Lubricants B.V.

- Parker Hannfin Corp

- PETRONAS Lubricants International

- Shell plc

- Tazzetti S.p.A

- TotalEnergies

- Xaerus Performance Fluids International

第7章 市場機会と今後の動向

- ナノ潤滑技術への注目の高まり

- 極低温用途の需要拡大

目次

The Refrigeration Lubricants Market size is estimated at USD 3.67 billion in 2025, and is expected to reach USD 4.39 billion by 2030, at a CAGR of 3.67% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns around the globe, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market studied. However, the conditions started recovering in 2021, which is expected to restore the market's growth trajectory during the forecast period.

Key Highlights

- The emergence of new-generation refrigeration lubricants optimized for energy efficiency, increasing momentum in the global HVACR industry, and recovering automotive industry are expected to drive the growth of the refrigeration lubricants market.

- On the flip side, phasing out of existing refrigerants due to constant regulations amendments is expected to hinder the market's growth.

- Augmenting prominence for nano lubricant technology and a gain in demand for cryogenic applications are expected to unveil new opportunities for the market studied.

- Asia-Pacific dominated the global market, with the most significant consumption from the countries such as India and China.

Refrigeration Lubricants Market Trends

Increasing Momentum in the Global HVACR Industry

- Air conditioning (AC) units are designed to modify humidity and air temperature in an enclosed area. The primary components of an air conditioner are compressor, evaporator, expansion valve, and condenser. Lubricants reduce side effects, such as pipeline corrosion, and provide better compatibility with common refrigeration gases.

- Refrigeration lubricants have multiple purposes, such as removing heat, lubricating moving parts, acting as a sealant, and cooling the critical components of compressors.

- According to the International Energy Agency, space cooling demand experienced the highest annual growth among all buildings end uses in 2021 and accounted for nearly 16% of the buildings sector's final electricity consumption (about 2 000 TWh). This is expected to benefit the air conditioning lubricant market over the forecast period.

- The Government of India, in November 2021, selected 26 applications under the production-linked incentive (PLI) scheme for white goods. These are for air-conditioning (AC) manufacturing with a committed investment of INR 3,898 crore. This initiative is likely to boost production in the country and have a positive impact on the refrigeration lubricants market.

- The rising trends for electric vehicles are further likely to support the refrigeration lubricant market. China was the leading producer of electric vehicles in 2021. According to the China Passenger Car Association (CPCA), the country sold over 3.3 million units in 2021, which also accounted for an increase of 169% compared to 2020.

- The electric vehicles market in India is majorly driven by the two-wheeler segment that accounted for over 48% in 2021. According to the Ministry of Road Transport & Highways (MoRTH), 3,29,190 electric vehicles were sold in the country, representing an increase of 168% compared to the sales in 2020.

- The factors mentioned above are likely to impact the refrigeration lubricants market positively.

Asia-Pacific is Expected to Dominate the Market

- The Asia-Pacific region was the largest market for refrigeration lubricants. The rising demand for refrigeration lubricants can be attributed to the increasing usage of air conditioning systems for domestic and industrial applications.

- China is the largest automotive hub in the world. According to OICA, the overall automotive production in the country in 2021 stood at 2,60,82,220, a 3% increase from 2020.

- China's leading electric car manufacturers include Tesla, BYD Co., and Nio Inc. The growing demand for electric vehicles in the country is driving the market for refrigeration lubricants for automotive compressors.

- As per the report by OICA, Europe produced 11,886,776 units from quarter 1 to quarter 3 of 2021, whereas China produced 18,242,588 vehicles in the same period. Therefore the demand for AC in automobiles continues to increase.

- South Korean sales of electric vehicles surged by 96% to 71,006 units in the first nine months of 2021, according to data collected by the Korea Automotive Technology Institute (KAII). The sales figure is further expected to increase with growing demand from the importing economies in Europe, Asia Pacific, and the Americas.

- In 2021, India produced 32,89,683 electric vehicles for the first three quarters of 2021, a massive increase of 53% from 2020. The growing automotive sector is expected to augment the market in the forecast period.

- India ranks fourth in the most extensive railway system in the world after the United States, Russia, and China, with 123,542 km of tracks, 67,415 km of route, and more than 7,300 stations.

- The second-largest populated country in the world runs 13,523 passenger trains and 9,146 freight trains regularly on its network. The railways carried 1.23 billion metric tons of freight in FY2020-FY2021.

- Due to all the factors above, Asia-Pacific is expected to dominate the market in the upcoming years.

Refrigeration Lubricants Industry Overview

The refrigeration lubricants market has a higher degree of fragmentation owing to multiple emission regulations in various countries. Key players (not in any particular order) in the market include ExxonMobil Corporation, Shell PLC, Fuchs, IdemitsuKosan Co. Ltd, and PETRONAS Lubricants International.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Emergence of New Generation Refrigeration Lubricants Optimized for Energy Efficiency

- 4.1.2 Increasing Momentum in the Global HVACR Industry

- 4.1.3 Recovering Automotive Industry

- 4.2 Restraints

- 4.2.1 Phasing out of Existing Refrigerants due to Constant Regulations Amendments

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 By Base Oil

- 5.1.1 Mineral Oil Lubricant

- 5.1.1.1 Paraffinic Oil

- 5.1.1.2 Naphthenic Oil

- 5.1.1.3 Aromatic Oil

- 5.1.2 By Synthetic Lubricant

- 5.1.2.1 Synthetic Hydrocarbon

- 5.1.2.1.1 Polyalphaolefin (PAO)

- 5.1.2.1.2 Alkylated Aromatics

- 5.1.2.1.3 Polybutene

- 5.1.2.2 By Ester

- 5.1.2.2.1 Diester

- 5.1.2.2.2 Polyol Ester

- 5.1.2.2.3 Phosphate Ester

- 5.1.2.2.4 Polymer Ester

- 5.1.2.3 Polyalkylene Glycols (PAG)

- 5.1.2.4 Other Synthetic Lubricants

- 5.1.1 Mineral Oil Lubricant

- 5.2 By Application

- 5.2.1 Air Conditioning

- 5.2.1.1 Transportation

- 5.2.1.1.1 Automotive

- 5.2.1.1.2 Other Modes of Transportation (Rail Road, Airways, and Marine)

- 5.2.1.2 Other Air Conditioning Applications (Stationary Applications)

- 5.2.2 Refrigeration (Household, Industrial, and Cryogenics)

- 5.2.1 Air Conditioning

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 BP PLC

- 6.4.3 BVA Oil

- 6.4.4 Chevron Corporation

- 6.4.5 China National Petroleum Corporation

- 6.4.6 China Petroleum & Chemical Corporation (SINOPEC Group)

- 6.4.7 CPI Fluid Engineering

- 6.4.8 ENEOS Corporation

- 6.4.9 ExxonMobil Corporation

- 6.4.10 Fuchs

- 6.4.11 HP Lubricants

- 6.4.12 Idemitsu Kosan Co. Ltd

- 6.4.13 Isel

- 6.4.14 Kluber Lubrication

- 6.4.15 Kuwait Petroleum

- 6.4.16 Matrix Specialty Lubricants B.V.

- 6.4.17 Parker Hannfin Corp

- 6.4.18 PETRONAS Lubricants International

- 6.4.19 Shell plc

- 6.4.20 Tazzetti S.p.A

- 6.4.21 TotalEnergies

- 6.4.22 Xaerus Performance Fluids International

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Augmenting Prominence for Nano Lubricant Technology

- 7.2 Gain in Demand for Cryogenic Applications

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日