|

市場調査レポート

商品コード

1906990

ファイバーセメント:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Fiber Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ファイバーセメント:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

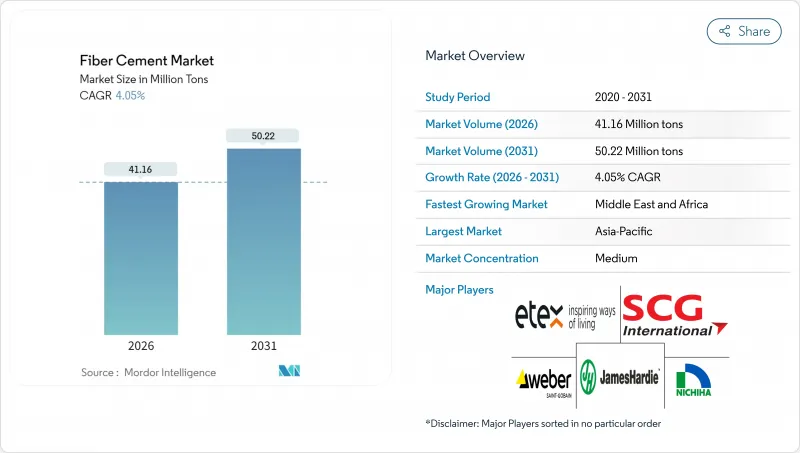

2026年のファイバーセメント市場規模は4,116万トンと推定され、2025年の3,956万トンから成長し、2031年には5,022万トンに達すると予測されています。

2026年から2031年にかけての年間平均成長率(CAGR)は4.05%となる見込みです。

堅調な需要は、より厳格な防火基準への適合を容易にする不燃性、ライフサイクルにおける交換コストを低減する優れた耐候性、そして個人住宅のリノベーションから大規模商業開発までを満足させる設計の柔軟性といった素材特性に起因しています。サプライチェーンパートナーも、木製サイディングと合成代替材の性能差を埋めるファイバーセメントの能力を認識しており、これが建設サイクル全体が鈍化した場合でも堅調な数量成長を支える要因となっています。建物所有者は40年に及ぶ耐用年数を評価し、保険会社は不燃性外壁に対して保険料の割引を適用するため、山火事多発地域での採用意欲が高まっています。競合面では、主要メーカーは流通チャネル管理を強化する建設業者との直接契約を加速させる一方、中堅企業は利益率維持のため合成繊維の革新やカーボンネガティブ配合技術に注力しています。

世界のファイバーセメント市場の動向と洞察

アジア太平洋地域における急速な都市化と住宅建設の回復

政府の住宅政策と大規模インフラ計画が、中国・インド・ASEAN諸国におけるファイバーセメント市場の安定した需要を牽引しています。中国では2024年に都市化率が66.2%に達し、年間1,400万人の都市住民が増加。インドでは2050年までに4億1,600万人の都市住民が統合されると予測されています。インドネシアでは2024年に建築許可件数が8.3%増加し、タイでは東部経済回廊構想のもと2025年に4.2%の業界成長が見込まれています。ファイバーセメントを不燃性外壁材として分類するASEAN統一防火安全基準が、地域での使用をさらに確固たるものにしています。人口動態の変化、住宅支援政策、より厳格な建築基準が相まって、ファイバーセメント市場には複数年にわたる需要の成長基盤が確保されています。

厳格な防火・遮音性能建築基準

カリフォルニア州の2024年タイトル24改正により、450万棟の構造物を対象とする山林市街地境界地域(WUI)においてクラスA外装材が義務化されました。同様にオーストラリアの国家建築基準改正では、280万戸の住宅に同等の要件が適用されます。2024年国際建築基準(IBC)は集合住宅プロジェクトの音響性能基準を強化し、音の伝達を抑制する高密度外壁材の採用を促進しています。ノースカロライナ州の火災試験データによれば、ファイバーセメントは木製サイディングに比べ着火確率が73%低く、追加層なしで18デシベルの騒音低減を実現します。こうした規制により、ファイバーセメントはプレミアムオプションから、拡大する管轄区域全体における適合要件へと地位を高めています。

ビニール代替品との初期設置コスト比較

ファイバーセメントの施工費用は1平方フィートあたり8~12米ドルで、ビニール材より60~100%高価です。多くの地域で人手不足が深刻化しており、粉塵管理用の特殊工具を必要とするため工数が25~35%増加し、価格差がさらに拡大しています。関税シナリオにより輸入資材コストがさらに6~14%上昇する可能性があり、2024年の購入者の32%を占める新規住宅購入者層における価格差が拡大する見込みです。コスト面での逆風は、メンテナンス費用が発生する前に物件を売却する開発業者が多い集合住宅プロジェクトで最も深刻であり、長寿命の外壁への投資意欲を低下させています。

セグメント分析

サイディングは2025年の市場シェア34.75%を維持。これは、木目調のファイバーセメントが美的基準を満たす一戸建て住宅や改修プロジェクトでの長年の使用実績を反映しています。老朽化した住宅ストックからの更新需要が、新規建設の周期的な変動から販売量を保護し、施工業者の高い熟知度が流通経路の安定性を強化しています。しかしながら、中層・高層建築物に対する厳格な防火規制とパネル化建築システムの急速な普及により、クラッディングは2031年までCAGR4.52%でサイディングを上回る成長が見込まれます。データセンター建設やインフラ大規模プロジェクトでは不燃性ファサードが頻繁に採用され、極端な温度変化に耐える厚手のファイバーセメントクラッディングパネルを建築家が指定する傾向が強まっています。屋根材、モールディング、トリミング部品は安定した追加需要を継続的に生み出し、既存のカラーコーティング設備を活用したクロスセリングの機会をメーカーに提供しています。こうした進化する用途構成が、ファイバーセメント市場全体におけるバランスの取れた成長要因を支えています。

クラッディングの拡大は、サイディングとの歴史的な差を縮め、現代的な複合素材の美学に適合するカラーパレットや表面テクスチャーの拡充をサプライヤーに促しています。最新の国際建築基準法(IBC)における規制の明確化は、不燃性外壁アセンブリを優先する性能要件を規定することで、この流れを強化しています。開発業者が総コストと規制順守を包括的に評価する中、商業用ファサードにおけるファイバーセメントの認知度向上は、ファイバーセメント市場における重要な成長経路となっています。

本ファイバーセメント市場レポートは、用途別(サイディング、クラッディング、モールディング・トリミング、屋根材、その他用途)、エンドユーザーセクター別(住宅、商業、産業・公共施設、インフラ)、地域別(アジア太平洋、北米、欧州、南米、中東・アフリカ)に分類されています。市場予測は数量(トン)単位で提供されます。

地域別分析

アジア太平洋地域は、急速な都市化、住宅政策の支援、地域全体での厳格な防火基準の採用により、2025年の数量の42.45%を占めました。中国では年間1,400万人の都市住民が増加し続けており、インドの地下鉄拡張は堅調な建築許可件数を支えています。インドネシアの建築許可件数は2024年に8.3%増加し、タイでは1兆7,000億バーツ(472億米ドル)を超える東部経済回廊への投資により、2025年の建設成長率は4.2%と予測されています。セルロース原料への近接性と発達したセメントインフラがコスト優位性をもたらし、ファイバーセメント市場全体で生産能力投資を誘引しています。

北米は成熟した市場ながら安定しており、建築基準に基づく建て替え需要が市場規模を支えています。米国西部における大規模な山火事のリスクが、不燃性建材への外壁改修を加速させており、保険会社の優遇措置が住宅所有者の関心を高めています。カナダでは、堅調な改修セグメントが多世帯住宅着工の減速を相殺しています。一方、メキシコでは新興中産階級が中層住宅向け耐久性外壁材の需要拡大を牽引しています。プレハブパネルの継続的革新と建設業者との直接契約が北米の需要を支え続け、同地域はファイバーセメント業界における世界の戦略の中核的地位を維持しています。

中東・アフリカ地域は2031年までに4.38%という最速の地域CAGRを達成する見込みです。サウジアラビアの「ビジョン2030」メガプロジェクト(NEOMやザ・ラインを含む)は5,000億米ドル以上の建設価値を生み出しますが、これら全てに厳格な外壁性能基準が適用されます。アラブ首長国連邦(UAE)とカタールではインフラ整備が継続され、高層ビル群における防火規制が不燃性クラッディングを推奨しています。湾岸地域の極端な気候条件は耐候性材料の需要を高め、ファイバーセメントの魅力が増しています。現地生産能力の制限により短期的供給が制約される可能性がありますが、既に発表されている合弁事業や工場拡張は、この有望なファイバーセメント市場セグメントにおけるボトルネック解消を目的としています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場促進要因

- アジア太平洋地域における急速な都市化と住宅建設の回復

- 厳格な防火・遮音性能建築基準

- 木材およびビニールサイディングに対するライフサイクルコストの優位性

- 中層建築物におけるパネル式プレハブファサードの採用状況

- セルロースナノファイバーを用いたカーボンネガティブセメント配合技術

- 市場抑制要因

- ビニール代替品との比較における初期設置コストの高さ

- エンジニアードウッドサイディングなどの代替品の入手可能性

- 世界のパルプ価格変動に伴う繊維調達リスク

- バリューチェーン分析

- 規制情勢

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 最終用途セクター動向

第5章 市場規模と成長予測

- 用途別

- サイディング

- クラッディング

- 成形およびトリミング

- 屋根材

- その他の用途

- エンドユーザーセクター別

- 住宅

- 商業

- 産業・公共施設

- インフラ

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- 北欧諸国

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- Allura

- American Fiber Cement.

- CSR Limited

- ElEMENTIA MATERIALS, SAB DE CV

- Eterno Ivica S.r.l.

- Etex Group

- Everest

- HIL Limited

- James Hardie Building Products Inc.

- KMEW Co., Ltd.

- Mahaphant Fibre-Cement(South Asia)Pvt. Ltd

- Maxitile Inc.

- NICHIHA

- Ramco Industries Limited

- Renaatus Group

- Saint-Gobain(Weber & Eternit)

- SCG International Corporation

- SHERA Public Company Limited

- Swisspearl Group AG