|

市場調査レポート

商品コード

1686201

北米のペットフード:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のペットフード:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 352 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

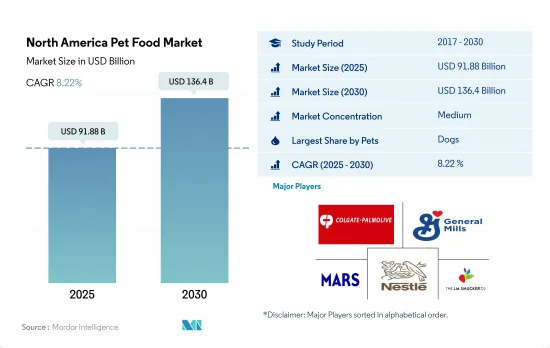

北米のペットフード市場規模は2025年に918億8,000万米ドルと推定され、2030年には1,364億米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは8.22%で成長する見込みです。

犬はペットフードの嗜好性の幅が広いため、猫に比べて犬用の市販ペットフードの利用が増加しています。

- 北米のペットフード業界は、特にペットフード市場において急速な成長を遂げています。北米のペットフード市場では、犬と猫が数量・金額ともに大きなシェアを占めています。この背景には、ペットの飼い主の間で健康とウェルネスに対する意識が高まっていることがあります。一般的に、犬は猫に比べて食事内容が多様で、多くの飼い主がドライフードとウェットフードを組み合わせて与えることを選択しています。

- この地域では、ペットフードとおやつが動物に与える主な餌の種類であり、2022年の市場シェアの85.5%を占めています。かつては、ペットフードは主に肉や穀物を原料としたドライフードとウェット製品で構成されていました。しかし、消費者の嗜好が変化し、ペットの健康とウェルネスが重視されるようになったため、ペットフード業界は特定の食事ニーズや嗜好に対応した幅広い製品を提供するように進化しました。

- 北米におけるペットフードの主な流通チャネルは、スーパーマーケット、ペットショップ、オンライン小売業者で、2022年の市場シェアはこれらのチャネル合計で77.4%を占めました。これらのチャネルは、アクセスのしやすさ、利便性、オンラインショッピングの人気のため、消費者に好まれています。

- 消費の面では、米国とカナダが北米の主要国で、2022年のペットフードの市場シェアは合計で94.8%を占めています。これは、ペットの飼育率の高さ、可処分所得の増加、プレミアム・ペットフードやオーガニック・ペットフードに対する消費者の嗜好の変化といった要因によるものです。

- したがって、ペットフード市場の成長は、eコマースの台頭と、ペットの健康とウェルネスに対する消費者の嗜好の変化によって牽引されています。予測期間中のCAGRは8.4%を記録すると予想されます。

米国では業務用ペットフードの普及が進み、米国市場は他国を上回る成長を遂げます。

- 北米のペットフード市場は、世界のペットフード市場の中でも最大規模です。2022年、北米はペット数が多く、過去5年間のペット飼育率が高く、同地域でペット専用フード製品に対する認識が高まっていることから、世界市場の727億1,000万米ドルを占めました。

- 北米ペットフード市場で最大のシェアを占めるのは米国です。この地域でペット数が最も多く、ペットの人間化とプレミアム化が進んでいるためで、2022年には市場の88.5%を占めました。例えば、米国のペット数は2017年の2億1,540万頭から2022年には2億3,910万頭に増加し、2022年にはペットの親の40%がプレミアムペットフードを購入しています。

- カナダは米国に比べてペットの飼育数が少ないため、2022年には45億3,000万米ドルと評価され、市場シェア第2位を占めました。同国は、ペットの健康に対する意識の高まりとペットへの支出の増加により、予測期間中にCAGR 4.5%を記録すると予想されています。

- メキシコはこの地域で最も急成長している国の一つです。メキシコのペットの親たちは、ペットのために高品質で栄養価の高いペットフード製品を購入するようになっているため、メキシコのペットフード市場は予測期間中にCAGR 7.1%を記録すると予想されます。同国ではペットの年齢が上昇しており、これが動物用飼料の需要増につながると予想されます。

- ペット数の増加、プレミアムフードに対する需要の高まり、ペットの健康不安に対する意識の高まりが、予測期間中の北米ペットフード市場の成長を後押しすると予想されます。

北米のペットフード市場の動向

若年層とミレニアル世代からの採用の増加がキャットフード市場を牽引

- 北米ではペットとしての猫の飼育が増加しているが、これは同伴者としての需要が高く、犬よりも猫のペットフードへの支出が少ないためです。同地域では、ペットの人間化が進んでいること、また、猫は犬よりも飼育面積が少なくて済むことから、ペットとしての猫は2017年から2022年にかけて13.6%増加しました。例えば米国では、猫をペットとして飼っている世帯は2020年には26%だったが、2022年には53.5%に増加しました。

- 米国、カナダ、メキシコでは、在宅勤務の文化が同伴者の需要につながり、ペットを飼う人の多くがミレニアル世代であることから、流行期にペットとしての猫の採用が増加しました。例えば、2022年には、米国ではミレニアル世代がペットの親の33%を占め、2020年には、猫のペット数の40%が国内の動物保護施設から引き取られました。さらに、ペットの親は高収入のため、ペットショップから猫を購入しました。例えば、2020年には、米国の猫の親の43%がペットショップから猫を購入しています。したがって、この地域のペットとしての猫は2020年から2022年の間に5.34%増加しました。

- 同地域では成猫よりも若い猫が多く飼われており、その数では米国がリードしています。例えば、2021年の米国の猫の飼育数は684,144頭で、若い猫が53.5%を占めています。若い猫の飼育数が増え、ミレニアル世代がペットの親となることで、予測期間中のペットフード製品の成長に貢献すると予想されます。猫の養子縁組と購入の増加、ペットの人間化の増加がペット数の増加に貢献すると予想されます。ペット数の増加は、同地域のペットフード市場の成長に寄与するであろう。

自然食品と有機食品への需要が同地域での支出を増加させています。

- 北米ではペットの支出が増加しています。ペットの支出が増加しているのは、さまざまな種類のペットフードが入手可能になったことと、米国とカナダでペットフード製品のプレミアム化が進んでいるためです。同地域では、カスタマイズされたペットフード、ナチュラルフード、オーガニックフードなど、プレミアムセグメントへの支出が増加しています。

- ペットの親が最も多く支出するのはペットフードであり、これは予測期間中に増加すると予測されます。例えば、米国では2022年にペットフードがペット費用の42.4%(1億3,680万米ドル)を占めました。ペットフードのシェアが最も大きく、ペットの親がペットを家族として扱うようになり、ペット専用フードに対する意識が高まるにつれて増加すると予測されます。ドッグフードの支出シェアが猫よりも高いのは、犬の飼育数が多いことと、猫よりもフードの消費量が多いためです。ペットペアレントはペットを家族の一員と考え、高級ペットフードを与え、グルーミングやデイケアなどのサービスを利用します。米国では、ペットの親の約40%がプレミアム・ペットフードを購入し、2022年にはペットのグルーミングや散歩などのサービスに114億米ドルが費やされました。

- ペットの親は、オンライン小売店、スーパーマーケット、ペットショップを通じてペットフードを購入します。様々なペットフード製品がeコマースサイトで販売されているため、オンライン小売業者を通じてペットフードの売上が増加しています。例えば米国では、フードを含むペットケア製品のオンライン販売は、2020年の32%から2022年には40%に増加しました。

- プレミアム化と高品質フードの利点に関する意識の高まりは、この地域のペット支出を押し上げると予想される要因です。

北米ペットフード産業の概要

北米ペットフード市場は適度に統合されており、上位5社で45.37%を占めています。この市場の主要企業は以下の通りです。 Colgate-Palmolive Company(Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle(Purina)and The J. M. Smucker Company(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他のペット

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェット・ペットフード

- ペット用栄養補助食品・サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用おやつ

- サブ製品別

- クランキートリーツ

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&チューイートリーツ

- その他のおやつ

- ペット用獣医食

- サブ製品別

- 糖尿病

- 消化器過敏症用

- オーラルケア

- 腎臓

- 尿路疾患

- その他の獣医食

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンライン・チャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

- The J. M. Smucker Company

- Virbac

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The North America Pet Food Market size is estimated at 91.88 billion USD in 2025, and is expected to reach 136.4 billion USD by 2030, growing at a CAGR of 8.22% during the forecast period (2025-2030).

Dogs exhibit a wider range of pet food preferences, which has led to an increased usage of commercial pet foods for dogs compared to cats

- The pet food industry in North America is experiencing rapid growth, particularly in the market for pet food. Dogs and cats held a significant share in both the volume and value of the North American pet food market. This can be attributed to the increased awareness about health and wellness among pet owners. Dogs typically have a more varied diet compared to cats, with many owners choosing to feed them a combination of dry and wet food.

- Pet food and treats are the primary types of food given to animals in the region, accounting for 85.5% of the market share in 2022. In the past, pet food mainly consisted of dry and wet products made from meat and grains. However, due to changing consumer preferences and a greater focus on pet health and wellness, the pet food industry has evolved to offer a wider range of products that cater to specific dietary needs and preferences.

- The main channels for distributing pet food in North America are supermarkets, pet stores, and online retailers, which collectively accounted for a 77.4% market share in 2022. These channels are preferred by consumers due to their accessibility, convenience, and the popularity of online shopping.

- In terms of consumption, the United States and Canada are the major countries in North America, representing a combined market share of 94.8% for pet food in 2022. This can be attributed to factors such as high pet ownership rates, increasing disposable incomes, and changing consumer preferences toward premium and organic pet food.

- Therefore, the growth of the pet food market is being driven by the rise of e-commerce and changing consumer preferences toward pet health and wellness. It is anticipated to record a CAGR of 8.4% during the forecast period.

Higher adoption of commercial pet food products in the United States to boost the US market in growing faster than other countries

- The North American pet food market is one of the largest in the global pet food market. In 2022, North America accounted for USD 72.71 billion of the global market due to the large pet population, the high adoption rate of pets over the past five years, and growing awareness about specialized pet food products in the region.

- The United States holds the largest share of the North American pet food market. It accounted for 88.5% of the market in 2022 due to the highest pet population in the region and the growing pet humanization and premiumization. For instance, the pet population in the United States increased from 215.4 million heads in 2017 to 239.1 million heads in 2022, and 40% of pet parents purchased premium pet food in 2022.

- Canada held the second-largest share of the market, valued at USD 4.53 billion in 2022, due to the lower adoption of pets compared to the United States. The country is expected to register a CAGR of 4.5% during the forecast period due to the rising awareness about pet health and the growing pet expenditure.

- Mexico is one of the fastest-growing countries in the region. The Mexican pet food market is anticipated to register a CAGR of 7.1% during the forecast period due to Mexican pet parents increasingly purchasing high-quality and nutritious pet food products for their pets. There is a rise in the pets' ages, which is expected to help increase the demand for veterinary diets in the country.

- The rising pet population, growing demand for premium foods, and rising awareness about health concerns in pets are anticipated to boost the growth of the North American pet food market during the forecast period.

North America Pet Food Market Trends

Increasing adoptions from young adults and millennials are driving the cat food market

- There is an increase in the adoption of cats as pets in North America, owing to the high demand for companionship and less expenditure on pet food for cats than dogs. In the region, cats as pets increased by 13.6% between 2017 and 2022 due to the rise in pet humanization and because cats require less area to live than dogs. For instance, in the United States, households owning a cat as a pet was 26% in 2020, which increased to 53.5% in 2022.

- The United States, Canada, and Mexico witnessed higher adoption of cats as pets during the pandemic because of the work-from-home culture leading to a demand for companionship and a higher number of pet owners being millennials. For instance, in 2022, millennials were 33% of pet parents in the United States, and in 2020, 40% of the cat pet population was adopted from animal shelters in the country. Additionally, pet parents purchased cats from pet stores due to high income. For instance, in 2020, 43% of cat parents in the United States purchased cats from pet stores. Therefore, cats as pets in the region increased by 5.34% between 2020 and 2022.

- Young cats are being adopted more than adult cats in the region, with the United States leading in terms of that number. For instance, in 2021, the adopted cat population in the United States was 684,144, and young cats accounted for 53.5% of the cats adopted. The higher population of young cats and millennials being pet parents is expected to help in the growth of pet food products during the forecast period. An increase in the adoption and purchase of cats and an increase in pet humanization are expected to help in the growth of the pet population. The increasing pet population will help in the growth of the pet food market in the region.

Demand for natural and organic foods is increasing the expenditure in the region

- Pet expenditure is increasing in North America. The rise in pet expenditure is due to the availability of different types of pet food and the growing premiumization of pet food products in the United States and Canada. Pet parents are spending more on premium segments in the region, such as customized, natural, and organic pet food.

- The highest expenses of pet parents are on pet food, which is estimated to increase during the forecast period. For instance, pet food accounted for 42.4% of pet expenses in the United States (USD 136.8 million) in 2022. Pet food has the largest share, which is projected to increase as pet parents increasingly treat their pets as family members and the awareness about specialized pet food rises. The expenditure share of dog food is higher than that of cats because the dog population is higher and because they consume a larger quantity of food than cats. Pet parents provide premium pet food to their pets and use services such as pet grooming and pet daycare in the region as they consider them as family members. In the United States, about 40% of pet parents purchased premium pet food, and USD 11.4 billion was spent on services such as pet grooming and pet walking in 2022.

- Pet parents purchase pet food through online retailers, supermarkets, and pet stores. Higher pet food sales are generated through online retailers as a variety of pet food products are available on e-commerce sites; also, the pandemic increased the number of online orders. For instance, in the United States, online sales of pet care products, including food, increased from 32% in 2020 to 40% in 2022.

- Premiumization and rising awareness about the benefits of quality food are factors anticipated to boost pet expenditure in the region.

North America Pet Food Industry Overview

The North America Pet Food Market is moderately consolidated, with the top five companies occupying 45.37%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and The J. M. Smucker Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Country

- 5.4.1 Canada

- 5.4.2 Mexico

- 5.4.3 United States

- 5.4.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 General Mills Inc.

- 6.4.5 Mars Incorporated

- 6.4.6 Nestle (Purina)

- 6.4.7 PLB International

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 The J. M. Smucker Company

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms