欧州のエネルギー管理システム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Europe Energy Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1849960

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

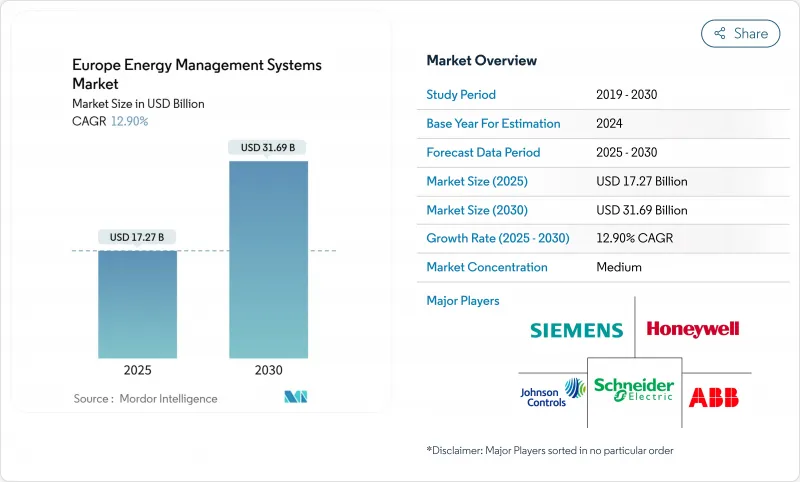

欧州のエネルギー管理システム市場は、2025年に172億7,000万米ドルに達し、2030年には316億9,000万米ドルに達すると予測されています。

デジタル優先の送電網のアップグレード、FIT-FOR-55の義務化、加速する企業のネット・ゼロ目標が総体的にこの拡大を支えており、この技術は裁量的な支出からインフラの必需品へと移行しています。5,840億ユーロ規模の電力投資が計画されている急速なスマートグリッド近代化は、ソフトウェア中心の最適化プラットフォームに対する広範な需要を引き起こしています。ビル・レベルの人工知能ツールは、エネルギー強度を30%削減し、施設をアクティブなグリッド・ノードに変えています。ドイツは、再生可能エネルギー80%という目標を背景に早期導入を進め、スペインではスマートホームブームが住宅用スケールアップのペースを作っています。ベンダー各社が予測分析とサイバーセキュリティの統合に向けた競争を繰り広げるなか、競合の激しさも増しています。

欧州のエネルギー管理システム市場動向と洞察

スマートグリッドインフラの導入拡大

EUの電力会社は、2030年までに5,840億ユーロの送電網投資を計画しており、このうち1,700億ユーロは堅牢なEMSプラットフォームに依存するデジタル化に充てられます。分散型再生可能エネルギー、ビークル・ツー・グリッドの流れ、仮想変電所ではリアルタイムのオーケストレーションが必要となり、EMSはコスト削減からグリッドクリティカルな資産へと昇格します。Enlit 2024におけるシュナイダーエレクトリックの仮想変電所の展開は、双方向電力アーキテクチャに対するベンダーのポジショニングを示しています。ビルは現在、柔軟性サービスを提供し、HEMSと配電系統運用者の間に相互データループを作り出しています。GridX社は、相互運用性標準の成熟に伴い、2030年までに欧州の住宅EMSが11倍に拡大すると予測via-tt.com

EUの「Fit-for-55」エネルギー効率義務化

改正建築物エネルギー性能指令は、2030年までのゼロエミッション建築と、最も性能の悪いストックに対する段階的なアップグレードを義務付けており、EMSの機能が遵守の前提条件となっています。全寿命炭素評価の義務化により、空調、照明、オンサイト再生可能エネルギーにわたる統合モニタリングが推進されます。スペインでは、国家統合エネルギー・気候計画を通じ、すでにビルオートメーション・ソフトウェアを年間17.21%引き上げており、規制の緊急性がそのまま販売パイプラインに反映されています。データロギング、分析、レポーティングをバンドルしたソリューションは、監査サイクルを短縮し、認証のリスクを軽減します。

分断された国レベルの建築基準

EUレベルの指令があるにもかかわらず、各国の規則がバラバラなため、サプライヤーは認証やインターフェイスのカスタマイズを余儀なくされ、プロジェクトのライフサイクルが膨れ上がっています。ドイツの基準はスペインやイタリアの基準から大きく逸脱しているため、複数の国のベンダーが並行して開発を進めざるを得ないです。エネルギー・スマート・アプライアンスのための自主行動規範は、プロトコルの整合を図ろうとするものだが、強制力を欠いています。規制のスペシャリストを持たない中小企業は競争に苦戦する可能性があり、統合を促しています。

セグメント分析

2024年の欧州のエネルギー管理システム市場シェアの45.3%をビルエネルギー管理システム(BEMS)が占める。BEMSに関連する欧州のエネルギー管理システム市場規模は、オフィスや小売チェーンがグリッドサービスのためにHVAC、照明、オンサイトストレージを改修するにつれて着実に上昇すると予想されます。ベンダーは、需要応答モジュールと監視制御をバンドルし、ビルを柔軟性資産として位置づける。家庭用エネルギー管理システム(HEMS)のCAGRは13.1%と最も速く、2025年までに380万戸の住宅をスマート化するというスペインの計画に後押しされています。AI対応のダッシュボードとモバイルアプリが消費者の利用を促進し、電力会社のリベートで投資回収がさらに促進されます。2030年までにHEMSが11倍に拡大するというGridXの予測は、EUの消費者向けインセンティブと一致し、住宅破壊の可能性を強調しています。

産業用EMSのニッチは、スコープ1の緩和を追い求めるエネルギー集約型セクターを対象に、より小さな基盤から成長しています。データセンターEMSとスマートシティプラットフォームは「その他」のバケットに属し、そこではレイテンシーに敏感な最適化が牽引役となっています。BEMSサプライヤーはマイクログリッド・コントローラを統合し、HEMSアプリはEV-to-homeやVPP参加機能を公開しています。

ハードウェアは2024年の売上高の42.7%を占め、アナリティクスが盛んになる前にメーター、ゲートウェイ、コントローラーが必要であることを強調しています。しかし、ソフトウェアがCAGR 14.3%で成長をリードしており、欧州のエネルギー管理システム市場がクラウドとAIの価値レイヤーに軸足を移していることを反映しています。急速に進化するSaaSパッケージは、予知保全、炭素会計、料金適応型スケジューリングなどを実現します。ソフトウェアに付随する欧州のエネルギー管理システム市場規模は、サブスクリプションモデルが永久ライセンスに取って代わり、資本制約が緩和されるにつれて拡大すると予測されます。

サービス導入、再委託、管理された最適化は、先に述べた人材の空白を埋めるものです。ベンダーは、ハードウェアがコモディティ化する中、アドバイザリーサービスをクロスセルして利幅を維持します。ジョンソンコントロールズの分析に重点を置いたMetasys 14.0は、静的なダッシュボードから継続的な改善エンジンへの移行を例証しており、ソフトウェアとサービスの境界線を曖昧にしています。

欧州のエネルギー管理システム市場は、ソリューションタイプ(ビルエネルギー管理システム(BEMS)、ホームエネルギー管理システム(HEMS)、その他)、コンポーネント(ハードウェア、ソフトウェア、サービス)、導入形態(オンプレミス、クラウドベース)、エンドユーザー(商業・小売、住宅、その他)、国別に区分されます。市場予測は金額(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- スマートグリッドインフラの導入拡大

- EUの「Fit-for-55」エネルギー効率規制

- 企業のネットゼロ目標がEMS導入を加速

- HVAC負荷の建物レベルのAI/ML最適化

- 柔軟性市場と需要応答収入の台頭

- プロジェクトリスクを軽減するエッジツークラウドのサイバーセキュリティツールキット

- 市場抑制要因

- 国レベルの建築基準法の断片化

- 高度な分析に必要なスキルセットの不足

- 従来のBMSプロトコル間の相互運用性のギャップ

- 中小企業セグメントにおけるインフレによる設備投資の延期

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 市場におけるマクロ経済動向の評価

第5章 市場規模と成長予測

- ソリューションタイプ別

- ビルエネルギー管理システム(BEMS)

- ホームエネルギー管理システム(HEMS)

- 産業/製造業向けEMS(IEMS)

- その他

- コンポーネント別

- ハードウェア

- ソフトウェア

- サービス

- 展開モード別

- オンプレミス

- クラウドベース

- エンドユーザー別

- 商業および小売

- 住宅用

- 産業施設

- ヘルスケア

- その他

- 国別

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベネルクス

- 北欧諸国

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Schneider Electric SE

- Siemens AG

- Honeywell International Inc.

- ABB Ltd

- Johnson Controls International plc

- Panasonic Holdings Corp.

- Enel X S.r.l.

- Uplight Inc.

- SAP SE

- British Gas Services(Centrica plc)

- Green Energy Options Ltd

- Efergy Technologies SL

- Cisco Systems Inc.

- IBM Corporation

- Eaton Corporation plc

- Rockwell Automation Inc.

- ENGIE Digital

- Landis+Gyr AG

- Delta Electronics Inc.

- Trane Technologies plc

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日