|

市場調査レポート

商品コード

1685958

世界のマネージドモビリティサービス-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Global Managed Mobility Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界のマネージドモビリティサービス-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 179 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

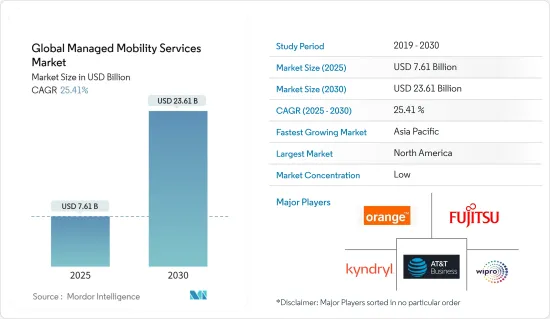

マネージドモビリティサービスの世界市場規模は、2025年に76億1,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは25.41%で、2030年には236億1,000万米ドルに達すると予測されます。

主なハイライト

- マネージドモビリティサービス・プロバイダーは、様々なデバイス・プラットフォームの複雑な管理に対応することで、企業のIT部門の負担を軽減するソリューションを提供しています。そのため、マネージドモビリティサービスは、モバイル・オフィス・ワーカーを管理、サーバー、データベースに接続することで、モバイル・オフィス・ワーカーとの容易なコミュニケーションを可能にします。そのため、企業は、ビジネスEメール、データベース、その他の企業コンテンツにのみPCを使用する従来のコミュニケーションを克服することができます。

- さらに、サービス・ソリューションとしてのモビリティは、モバイル・デバイスのライフサイクル全体を管理する単一のパートナーを提供することで、企業の従業員の複雑なモバイル・デバイス技術ニーズを簡素化します。このように、これらの企業はモバイル・テクノロジー管理の手間を省くことで、ITチームはリソースと時間を節約し、ビジネスの変革に役立つ戦略的イニシアティブに集中することができます。

- 成熟した組織では、デジタル・コネクティビティへのシフトが進んでおり、従業員の少なくとも50%が、一元管理が必要な複数のデバイスを業務に使用しています。このように、新しいタイプのキャリアデバイスの台頭は、職場に溢れ、モビリティエコシステムを拡大し続け、組織間の複雑なコミュニケーションに対応する経験豊富なMMSプロバイダーの必要性を高めています。

- 医師、看護師、患者、その他のサポートスタッフのモバイルデバイスの使用は世界中で増加しています。さらに、ヘルスケア・エンドユーザー業界の組織は、データの共有と保存に関してHIPAA規制を遵守しなければならないです。これらの要因によって、ヘルスケア業界におけるマネージドモビリティサービスの導入が促進されると予想されます。

- 顧客は、サードパーティのマネージドモビリティサービスに投資する際、コストの可視化という課題を依然として抱えています。ベンダーの中には、手作業で個々のパラメーターを追加して見積もりコストを算出するために、総コストやキャパシティ、リソースを見積もる専門知識が不足しているところもあります。このような課題は、市場に欠点をもたらしています。

- 全体として、世界のマネージドモビリティサービス市場に対するCOVID-19の影響はまちまちです。パンデミックは、リモートワークへのシフトによりMMSサービスに対する需要を増加させた一方で、サプライチェーンの混乱や経済の不確実性を引き起こし、場合によっては投資の減少につながりました。しかし、パンデミックは世界のMMS市場における技術の進歩を加速させ、新しい革新的なソリューションにつながっています。企業が効率を高め、変化するビジネス環境に適応する方法を模索していることから、MMSサービス市場は長期的に成長すると予想されます。

マネージドモビリティサービス市場の動向

IT・通信エンドユーザー産業セグメントが大きな市場シェアを占める

- IT・通信業界は、マネージド・サービスの重要な市場です。さまざまな技術の採用率が高いため、エンタープライズ・モビリティの動向は長年にわたって浮上してきました。今日、企業は主にビジネス戦略とコア・コンピタンスに重点を置き、BYOD(Bring-your-own-Device)の活用と採用に拍車をかけています。このため、合理化されたモビリティ・サービスに対する要求が高まり、こうしたモバイル・デバイスの管理に対する需要が高まる可能性が高いです。

- さらに、中国、インド、ブラジルなどの新興国におけるモバイル加入者数の増加がBYODポリシーの採用を後押しし、作業効率と業務の柔軟性を高めています。Cisco社のレポートによると、BYODポリシーを導入している企業は、従業員1人当たり平均で年間350米ドルを節約しています。さらに、リアクティブ・プログラムにより、従業員1人当たり年間1,300米ドルまで節約できます。

- 政府の規制やCOVID-19の大流行による封鎖措置により、マネージド・クラウド・サービスに対する需要は世界中で高まっており、マネージドモビリティサービスをさらに後押しし、企業はリモートワークへの移行を余儀なくされています。

- また、州政府や地方自治体、規制機関によって義務付けられているサイバーセキュリティ・コンプライアンス要件も、セキュリティに重点を置いたマネージド・モビリティ・アプリケーション・サービスの必要性を高めています。さらに、コンピューティングを目的とした専用のオンプレミスハードウェアが減少し、ほとんどの機能がクラウドベースになるため、プライバシーとセキュリティの問題がより深刻になります。

- ハードウェア・デバイス、組み込みソフトウェア、通信サービスを接続するマネージドモビリティサービスにIoTソリューションを採用することで、スマート通信環境、スマート交通、スマートホーム、スマートヘルスケアを提供し、予測期間中に市場を牽引するとみられます。

予測期間中、北米が主要シェアを占める

- シスコの年次インターネットレポートによると、世界の一人当たりの平均デバイス数と接続数は、2023年末までに3.6に増加すると予測されています。2023年までに一人当たりの平均デバイス数と接続数が最も多い国の中では、米国が13.6台でトップを維持し、韓国と日本がこれに続くと予想されます。

- さらに、同国における5Gの普及も今後のIoTデバイスの需要を後押しします。AT&T、スプリント、Tモバイル、ベライゾンのような各国の携帯電話事業者が5Gの展開に注力したことで、ここ数年で大きな進展がありました。GSMAによると、5Gは2023年初頭に1億件のモバイル接続に達し、2025年には1億9,000万件以上の5G接続で国内をリードするモバイルネットワーク技術となります。

- クラウドとデジタルトランスフォーメーションは、データ侵害の総コストを増大させています。モバイルプラットフォームの利用、広範なクラウド移行、IoTデバイスがコストを増加させる要因となっています。Ponemon Instituteの「Cost of Data Breach Study」によると、データ侵害の世界平均は383万米ドルでした。しかし、米国におけるデータ侵害の平均コストは864万米ドルと著しく高かったです。データ漏えいの可能性が高いことから、企業はITセキュリティにより重点を置くようになり、マネージド・モバイル・サービス市場の牽引役となることが予想されます。

- カナダのマネージドモビリティサービス市場は、COVID-19パンデミックに起因する労働文化によってさらに投資が増加しています。例えば、MSP Corp Investments Inc.は2021年9月、カナダ全土のマネージドITサービス・プロバイダー(MSP)を買収・投資するための成長資金として3,500万米ドルを調達しました。主な金融支援者には、CIBCとBDCキャピタルのGrowth Equity Partners-Fund IIが含まれます。同社は、カナダ国内の高業績MSPを提携・買収し、MSPチームを強化するためのテクノロジー、リソース、ビジネスサポートを提供します。同社の主な注力分野は、マネージド・ネットワーク・サービス、モビリティ・マネジメント、サイバーセキュリティ、クラウド・ホスティングなどです。

- インダストリー4.0構想が世界にもたらしたデジタル動向も、産業用IoTの必要性を後押ししています。例えば、2021年5月、トロントを拠点とする新興企業のベアテック(BehrTech)は、同社が2020年に開発したIoT向け無線接続製品が評価され、表彰されました。また、同社はインダストリー4.0ラボを建設するため、連邦政府と非営利団体の共同資金提供プログラムから300万米ドルの助成金を獲得しました。

マネージドモビリティサービス業界の概要

マネージドモビリティサービス市場は細分化されており、AT&T Intellectual Property、富士通、Kyndryl Inc.、Wipro、Orange SAといった大手企業が存在します。同市場の企業は、パートナーシップ、契約、イノベーション、買収などの戦略を採用し、サービス提供の強化と持続可能な競争優位の獲得を目指しています。

- 2023年2月キンドリーランド・ノキアが世界ネットワークとエッジコンピューティングの提携を拡大。この3年契約は、柔軟性、信頼性、安全性の高いLTEおよび5Gプライベート無線接続サービス、ならびにインダストリー4.0ソリューションの展開に関する協力と加速の計画を拡大するものです。さらに、Kyndryl社は、最高レベルのNokia Digital Automation Cloud(DAC)認定ステータスを取得することで、Nokia社への戦略的投資を拡大し、世界中の顧客をサポートできる専門家リソースと熟練した実務者を増やしていきます。Kyndryland Nokia社は、ノースカロライナ州ローリーにパートナー・イノベーション・ラボを開設しました。このラボでは、高度なワイヤレス接続とエッジコンピューティングを多要素ゼロ信頼モデルで統合し、企業のITとOTを融合します。

- 2023年3月ウィプロは「5G Def-i」プラットフォームを正式に発表。この統合プラットフォームは、モビリティ市場の企業がインフラ、ネットワーク、サービスをシームレスに変革できるようにするもので、MWCバルセロナのパネルでデビューし、コネクテッド・エンタープライズの目標を実現しました。オープンスタンダードに基づいて構築されたウィプロの5G Def-iplatformは、企業が既存のインフラをオンボード化し、新しいアプリやサービスをインキュベートし、技術的変化に対応するために必要なクラウドネイティブ環境、ネットワークAPI、サードパーティ統合を提供します。この統合スイートは、クラウドのスケーラビリティと5Gのスピードと容量を兼ね備えています。また、実用的なビジネスインサイトを構築するためのインテリジェンスレイヤーも含まれています。また、エンドポイントデバイスの可視化とデータインサイト、ネットワーク事業者のサービス導入の迅速化、新しいエンタープライズアプリケーションの迅速な展開も可能です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヵ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 多業種におけるBYOD導入の増加

- 企業のIT活動のアウトソーシング

- 市場抑制要因

- 運用管理とコストの可視性の欠如

第6章 市場セグメンテーション

- 機能別

- モバイルデバイス管理

- モバイルアプリケーション管理

- モバイル・セキュリティ

- その他の機能

- 展開別

- クラウド

- オンプレミス

- エンドユーザー業界別

- IT・通信

- BFSI

- ヘルスケア

- 製造業

- 小売

- 教育

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- AT&T Intellectual Property

- Fujitsu

- Kyndryl Inc.

- Wipro

- Orange SA

- Telefonica SA

- Samsung Electronics Co. Ltd

- Hewlett Packard Enterprise

- Vodafone Group PLC

- Microsoft Corporation

- Tech Mahindra

第8章 投資分析

第9章 市場の将来

The Global Managed Mobility Services Market size is estimated at USD 7.61 billion in 2025, and is expected to reach USD 23.61 billion by 2030, at a CAGR of 25.41% during the forecast period (2025-2030).

Key Highlights

- The managed mobility service providers offer solutions that ease the burden on enterprise IT departments by dealing with complex managing of various device platforms, with the help of interpreted content for specialized mobile applications. Therefore, managed mobility services enable easy communication with mobile office workers by connecting them with management, servers, and databases. Thus, it allows enterprises to overcome the traditional communications that involve PC only for business emails, databases, and other corporate content.

- Furthermore, mobility as a service solution simplifies corporate personnel's complex mobile device technology needs by offering a single partner to manage the whole mobile device lifecycle. Thus, these companies take the hassle of managing mobile technology so that IT teams can save resources and time to focus on the strategic initiatives that are helping them to transform their businesses.

- The growing shift of mature organizations toward digital connectivity drives at least 50% of employees to use more than one device for work that demands centralized management. Thus, the rise of new types of carrier devices continues to flood workplaces and expand the mobility ecosystem, driving the need for experienced MMS providers to handle the complexity of communication across organizations.

- The use of mobile devices among doctors, nurses, patients, and other supporting staff has increased worldwide. Moreover, organizations in the healthcare end-user industry must adhere to HIPAA regulations for data sharing and storage. These factors are expected to drive the adoption of managed mobility services in the healthcare industry.

- Customers are still witnessing challenges for cost visibility as they invest in the third-party managed mobility service. Some vendors lack the expertise to estimate the total costs or the capacity or resources in order to add individual parameters to arrive at an estimated cost manually. Such challenges add a drawback to the market.

- Overall, the impact of COVID-19 on the global managed mobility services market has been mixed. While the pandemic has increased demand for MMS services due to the shift toward remote work, it has also caused disruptions to supply chains and economic uncertainties, leading to a decrease in investment in some cases. However, the pandemic has also accelerated technological advancements in the global MMS market, leading to new and innovative solutions. The market for MMS services is expected to grow in the long term as companies look for ways to increase efficiency and adapt to changing business environments.

Managed Mobility Services Market Trends

IT and Telecom End-user Industry Segment Holds Significant Market Share

- The IT and telecom sector is a significant market for managed services. Due to the high rate of various technological adoptions, the enterprise mobility trend has emerged over the years. Today, companies primarily focus on business strategies and core competencies, fueling the utilization and adoption of bring-your-own-device (BYOD). This increases the requirement for streamlined mobility services, likely to boost the demand for managing these mobile devices.

- Furthermore, the growing mobile subscriber base in emerging countries, such as China, India, and Brazil, has been propelling the adoption of BYOD policies, enhancing work efficiency and flexibility in operations. According to a Cisco report, enterprises with a BYOD policy save, on average, USD 350 per year per employee. Moreover, reactive programs can boost these savings to USD 1,300 per year per employee.

- The demand for managed cloud services has increased across the globe due to government regulations and lockdown measures due to the COVID-19 pandemic, further boosting the managed mobility services and forcing businesses to move towards remote working modes, which has led companies to adopt cloud-based solutions to expand their requirements.

- Cybersecurity compliance requirements mandated by the state and local governments and regulatory bodies also drive the need for managed mobility application services to be security-focused. Additionally, as dedicated, on-premise hardware for computing purposes will decrease, and most of the functionality will become cloud-based, privacy and security issues will become more intense.

- Adopting IoT solutions in managed mobility services, which connect hardware devices, embedded software, and communication services, offers smart communication environments, smart transportation, smart homes, and smart healthcare and is expected to drive the market during the forecast period.

North America to Hold Major Share over the Forecast Period

- According to the annual internet report by Cisco, the average number of devices and connections per capita worldwide is anticipated to increase to 3.6 by the end of the year 2023. Among the countries with the highest average per capita devices and connections by 2023, the United States is expected to remain at the top with an average of 13.6 devices and connections per capita, followed by South Korea and Japan.

- Moreover, the 5G penetration in the country also encourages the demand for IoT devices in the future. The focus on deploying 5G by national mobile operators, like AT&T, Sprint, T mobile, and Verizon, has led to significant developments over the years. According to the GSMA, 5G will reach 100 million mobile connections in early 2023 and become the country's leading mobile network technology by 2025, with more than 190 million 5G connections.

- Cloud and digital transformation have increased the total cost of a data breach. The use of mobile platforms, extensive cloud migration, and IoT devices are the drivers increasing the cost. According to the Ponemon Institute's "Cost of Data Breach Study," the global average for a data breach was USD 3.83 million. However, the average data breach cost in the United States was significantly high at USD 8.64 million. The high potential of data breaches is expected to drive the managed mobile services market as enterprises focus more on IT security.

- The Canadian managed mobility services market is witnessing increased investments further driven by the COVID-19 pandemic-induced work culture. For instance, in September 2021, MSP Corp Investments Inc. raised USD 35 million in growth capital to acquire and invest in managed IT services providers (MSPs) across Canada. Major financial backers include CIBC and BDC Capital's Growth Equity Partners - Fund II. The company partners and acquires high-performing MSPs in the country to deliver technology, resources, and business support to empower MSP teams. Key areas of focus of the company include managed network services, mobility management, cybersecurity, and cloud hosting.

- The digital trends brought globally by the Industry 4.0 initiatives also drive the need for industrial IoT. For instance, in May 2021, Toronto-based BehrTech, a startup, was awarded for its wireless connectivity products for the IoT that the company developed in 2020, and the company also received a USD 3 million grant from a joint funding program between the federal government and a non-profit organization to build an Industry 4.0 lab.

Managed Mobility Services Industry Overview

The managed mobility services market is fragmented, with the presence of major players like AT&T Intellectual Property, Fujitsu, Kyndryl Inc., Wipro, and Orange SA. Players in the market are adopting strategies such as partnerships, agreements, innovations, and acquisitions to enhance their service offerings and gain sustainable competitive advantage.

- February 2023: Kyndryland Nokia expanded its global network and edge computing alliance. The three-year agreement extends plans to collaborate on and accelerate the deployment of flexible, dependable, and secure LTE and 5G private wireless connectivity services, as well as Industry 4.0 solutions. Furthermore, Kyndryl increases its strategic investment in Nokia by achieving the highest tier Nokia Digital Automation Cloud (DAC) accreditation status, increasing expert resources and skilled practitioners ready to support customers worldwide. Kyndryland Nokia opened a partner innovation lab in Raleigh, North Carolina. The lab will integrate advanced wireless connectivity and edge computing with a multi-factor zero trust model, converging IT and OT for enterprises.

- March 2023: Wipro officially launched its "5G Def-I" platform. The integrated platform, which enables businesses in the mobility market to transform their infrastructure, networks, and services seamlessly, debuted at the MWC Barcelona panel, realizing the connected enterprise's goals. Wipro's 5G Def-iplatform, built on open standards, offers the cloud-native environment, network APIs, and third-party integrations required for businesses to onboard existing infrastructure, incubate new apps and services, and keep up with technological changes. The integrated suite combines cloud scalability with 5G speed and capacity. It also includes an intelligence layer for creating actionable business insights. It also includes visibility into endpoint devices and data insights, faster service implementation for network operators, and rapid deployment of new enterprise applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of BYOD in Multiple Industries

- 5.1.2 Companies Outsourcing IT Activities

- 5.2 Market Restraints

- 5.2.1 Lack of Control over Operations and Cost Visibility

6 MARKET SEGMENTATION

- 6.1 By Function

- 6.1.1 Mobile Device Management

- 6.1.2 Mobile Application Management

- 6.1.3 Mobile Security

- 6.1.4 Other Functions

- 6.2 By Deployment

- 6.2.1 Cloud

- 6.2.2 On-premise

- 6.3 By End-user Industry

- 6.3.1 IT and Telecom

- 6.3.2 BFSI

- 6.3.3 Healthcare

- 6.3.4 Manufacturing

- 6.3.5 Retail

- 6.3.6 Education

- 6.3.7 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AT&T Intellectual Property

- 7.1.2 Fujitsu

- 7.1.3 Kyndryl Inc.

- 7.1.4 Wipro

- 7.1.5 Orange SA

- 7.1.6 Telefonica SA

- 7.1.7 Samsung Electronics Co. Ltd

- 7.1.8 Hewlett Packard Enterprise

- 7.1.9 Vodafone Group PLC

- 7.1.10 Microsoft Corporation

- 7.1.11 Tech Mahindra