土壌処理:市場シェア分析、産業動向、成長予測(2025年~2030年)

Soil Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 323 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685946

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

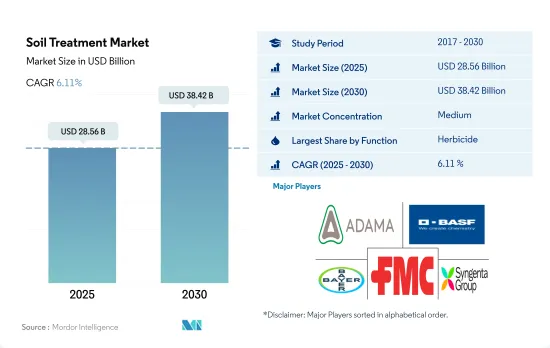

土壌処理市場規模は2025年に285億6,000万米ドルと推定され、2030年には384億2,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは6.11%で成長する見込みです。

土壌処理による効果で除草剤が市場を独占

- 2022年の土壌処理法の利用では、除草剤が72.8%と最も高いシェアを占めました。これらの除草剤は特に雑草の種子を標的とし、作物の播種前であってもその発芽を阻害します。この方法は、雑草の個体数をプロアクティブに管理し、より良い作物の定着と全体的な雑草防除を確実にする能力により人気を博しています。

- 不耕起栽培や最小耕起栽培など、近代的な農法を採用する傾向が高まっています。除草剤は、土壌処理法を用いて、雑草の圧力が高い圃場内の特定の場所をターゲットとして正確に散布することができるため、除草剤の使用を最適化し、コストを削減することができます。これらの要因が、除草剤散布における土壌処理の採用を促進しています。

- 殺虫剤は2022年の世界の土壌処理市場で12.8%のシェアを占めました。土壌中の蛹や卵は通常量の殺虫剤では影響を受けないが、幼虫期や成虫期は土壌処理によって防除できる可能性があります。シロイチモジヨトウ、ワレモコウ、フナクイムシ、ソイルメアリなどの害虫は、土壌処理によって効果的に管理できる可能性があります。

- 土壌処理殺菌剤の利用は、主に穀物および穀類に集中しており、市場において45.4%という最大の金額シェアを占めています。この嗜好は、殺菌剤が穀物や穀類の品質保護に有効であり、真菌感染の予防や軽減に役立つためです。

- アルジカルブ、フェナミホス、オキサミルのような殺線虫剤の土壌処理は、さまざまな作物に大きな損失をもたらすことで知られるMeloidogyne incognitaやPratylenchus brachyurusのような微小線虫の防除に効果的に使用されます。

- 前述の要因により、土壌処理市場は成長すると予想されます。

主要国における害虫による収量損失の増加が土壌処理の使用を促進しています。

- 土壌を媒介する害虫は、農業や生態系に世界的に大きな影響を与える可能性があります。これらの害虫には、土壌に生息する線虫、真菌、細菌、昆虫が含まれ、作物に被害を与え、収量を減少させ、生態系を乱す可能性があります。害虫を効果的に管理することは、食糧安全保障を確保し、安定した食糧供給を維持するために不可欠です。

- 2022年、南米の土壌処理セグメントは世界市場の実質的な34.2%のシェアを占めました。2017年から2022年にかけて、この地域は市場価値の顕著な増加を示し、2022年には85億6,890万米ドルを占めました。生産者は一般的に、土壌処理に土壌ドレンチ、散布、溝施用技術を採用しています。これらの方法で土壌を媒介する病気や害虫の駆除を強化することで、作物の収量が向上します。土壌の健全性を維持することが重視されるようになったことで、農家はこうした土壌処理アプローチを採用するようになりました。

- 北米は第二の主要国であり、29.6%の世界市場シェアを占めています。土壌を媒介とする病害は、作物生産の大きな制約と考えられています。リゾクトニア属菌、フザリウム属菌、バーティシリウム属菌、スクレロチニア属菌、ピシウム属菌、フィトフトラ属菌などの土壌伝染性植物病原菌は、小麦、綿花、トウモロコシ、野菜、果物、観葉植物などの多くの作物で、50%~75%の収量損失を引き起こす可能性があります。

- したがって、世界の土壌処理市場価値は、2023年から2029年の間にCAGR 5.0%を記録すると予想され、気候の変化と害虫の侵入による作物損失の増加のため、すべての作物の種類で大きな成長を示すと予想されます。

世界の土壌処理市場動向

土壌を媒介とする害虫、病気、雑草の蔓延が増加しているため、農薬の土壌処理による1ヘクタール当たりの消費量は世界的に増加するとみられます。

- 土壌施用モードによる作物保護化学物質の世界平均消費量は、2022年には農地1ha当たり2,345.0gと記録され、2017年の2,065.0gと比較して13.6%増加しました。

- 不耕起栽培や最小耕起栽培を含む近代的農法を採用する傾向が強まっているため、土壌中の害虫が増加しており、害虫、雑草、土壌伝染性病害を駆除するために農薬を土壌散布する必要があります。

- 除草剤、特に出芽前除草剤は、特に雑草の種子を標的にするため、一般に土壌に散布され、作物の播種前であってもその発芽を阻害します。この方法は、雑草の個体数をプロアクティブに管理し、より良い作物の定着と全体的な雑草防除を確実にする能力により、人気を博しています。

- ホワイトグラブの蔓延により、根系は大豆で約25%、トウモロコシで64%減少しました。フィロファガ・カピラータ(Phyllophaga capillata)とエゴプシス・ボルボセリドゥス(Aegopsis bolboceridus)はすべての評価変数に被害を与え、ブラジルのような南米諸国で大豆の生産性を58.62%、トウモロコシの生産性を59.76%低下させたことが観察されました。これらの土壌媒介害虫はすべて、殺虫剤の土壌散布によって効果的に防除できる可能性があります。

- 同様に、Meloidogyne incognitaやPratylenchus brachyurusのような線虫は、果菜類に大きな損失をもたらします。例えば、ニンジンでは平均20.0%という大きな損失が発生しやすいです。これらの寄生線虫は土壌に生息する生物であるため、殺線虫剤で土壌を処理し、これらの生物を死滅させることが重要です。

土壌伝染性病害の防除の必要性に伴い、土壌処理農薬の使用量が増加しています。

- 農薬市場のダイナミックな状況の中で、土壌処理農薬は重要な構成要素として際立っています。これらの特殊な化学薬品は、作物の健全な生育、効果的な害虫・病害の防除、持続可能な農業を促進する上で極めて重要な役割を果たしています。

- シペルメトリンはピレスロイド系殺虫剤で、土壌処理農薬として使用されることがあります。土壌に散布すると、シロアリや根ウジなど、土壌を媒介するさまざまな害虫を効果的に駆除します。シペルメトリンの作用機序は、接触時に害虫の神経系を標的とし、麻痺と最終的な死に至る。2022年の価格はトン当たり2万1,000米ドルでした。

- アトラジンは、農地や非農耕地における様々な広葉雑草やイネ科雑草の防除に、土壌処理として一般的に使用される除草剤です。特に、作物と栄養分、水、日照をめぐって競合する雑草の個体数を管理するのに効果的です。2022年の価格は1トン当たり1万3,800米ドルでした。

- マラチオンは有機リン系殺虫剤で、農地や非農耕地における様々な害虫駆除のための土壌処理に使用されます。作物やその他の植物に被害を与える飛翔性昆虫と匍匐性昆虫の両方に有効です。マラチオンの価格は1トンあたり1万2,500米ドル。

- Mancozebは殺菌剤であり、土壌処理剤として、うどんこ病、疫病、べと病など様々な真菌病の防除に使用されます。ジチオカルバメート系に属し、広範な植物病原菌に効くことで知られます。2022年の価格は1トン当たり7,800米ドルでした。

土壌処理業界の概要

土壌処理市場は適度に統合されており、上位5社で44.67%を占めています。この市場の主要企業は以下の通りです。 ADAMA Agricultural Solutions Ltd, BASF SE, Bayer AG, FMC Corporation and Syngenta Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- チリ

- 中国

- フランス

- ドイツ

- インド

- インドネシア

- イタリア

- 日本

- メキシコ

- ミャンマー

- オランダ

- パキスタン

- フィリピン

- ロシア

- 南アフリカ

- スペイン

- タイ

- ウクライナ

- 英国

- 米国

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 機能

- 殺菌剤

- 除草剤

- 殺虫剤

- 軟体動物駆除剤

- 殺線虫剤

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 地域

- アフリカ

- 国別

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他の欧州

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米

- 南米

- 国別

- アルゼンチン

- ブラジル

- チリ

- その他の南米諸国

- アフリカ

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd

- American Vanguard Corporation

- BASF SE

- Bayer AG

- FMC Corporation

- Nufarm Ltd

- PI Industries

- Rallis India Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 49722

The Soil Treatment Market size is estimated at 28.56 billion USD in 2025, and is expected to reach 38.42 billion USD by 2030, growing at a CAGR of 6.11% during the forecast period (2025-2030).

Herbicides dominate the market due to their effectiveness through soil treatment methods

- Herbicides accounted for the highest share of 72.8% in the utilization of soil treatment methods in 2022. These herbicides specifically target weed seeds, impeding their germination even prior to crop sowing. This approach has gained popularity due to its ability to proactively manage weed populations proactively, ensuring better crop establishment and overall weed control.

- There is a growing trend toward adopting modern farming practices, including no-till and minimum-till farming. Herbicides may be applied through the soil treatment method with precision, targeting specific areas in the field where weed pressure is high, thereby optimizing herbicide use and reducing costs. These factors are driving the adoption of soil treatment for herbicide applications.

- Insecticides accounted for a share of 12.8% of the global soil treatment market in 2022. Although the pupae and eggs in the soil are not affected by the normal doses of pesticides, larval and adult stages may be controlled by soil treatment. Pests like white grubs, wireworms, fungus gnats, and soil mealybugs may effectively be managed by soil application.

- The utilization of soil treatment fungicides was predominantly focused on grains and cereals, representing the largest value share of 45.4% in the market. This preference is driven by the effectiveness of fungicides in protecting the quality of grains and cereals, as they help prevent or reduce fungal infections.

- The soil treatment of nematicides like aldicarb, fenamiphos, and oxamyl may effectively be employed in controlling microscopic nematodes like Meloidogyne incognita and Pratylenchus brachyurus that are known to cause significant losses in various crops.

- Owing to the aforementioned factors, the market for soil treatment is anticipated to grow.

The rise in yield losses in major countries due to pests is driving the use of soil treatment

- Soil-borne pests may have a significant global impact on agriculture and ecosystems. These pests include nematodes, fungi, bacteria, and insects that live in the soil and can damage crops, reduce yields, and disrupt ecosystems. Managing pests effectively is essential for ensuring food security and maintaining a stable food supply.

- In 2022, the soil treatment segment in South America held a substantial 34.2% share of the global market. From 2017 to 2022, the region witnessed a noteworthy increase in market value, accounting for USD 8,568.9 million in 2022. Growers commonly employ soil drenching, broadcast, and furrow application techniques for soil treatment. Enhancing the control of soil-borne diseases and pests through these methods improves crop yields. The growing emphasis on preserving soil health has prompted farmers to embrace these soil treatment approaches.

- North America is the second leading country, holding a substantial 29.6% global market share. Soil-borne diseases are considered a major limitation of crop production. Soil-borne plant pathogens such as Rhizoctonia spp., Fusarium spp., Verticillium spp., Sclerotinia spp., Pythium spp., and Phytophthora spp. can cause 50% to 75% yield loss for many crops such as wheat, cotton, maize, vegetables, fruits, and ornamentals.

- Therefore, the global soil treatment market value is expected to register a CAGR of 5.0% during 2023-2029 and is anticipated to witness significant growth in all crop types due to the changing climate and rising crop losses due to pest infestation.

Global Soil Treatment Market Trends

The increasing infestation of soil borne pest, diseases, and weeds, the per hectare consumption of soil treatment of pesticides is likely to increase globally

- The global average consumption of crop protection chemicals through soil application mode was recorded as 2,345.0 g per ha of agricultural land in 2022, which increased by 13.6% compared to 2017, which was 2,065.0 g per ha.

- The growing trend toward the adoption of modern farming practices, including no-till and minimum-till farming, is increasing the pest population in the soil, necessitating the soil application of pesticides to control pests, weeds, and soil-borne diseases.

- Herbicides, specifically pre-emergent herbicides, are generally applied to soil as they specifically target weed seeds, impeding their germination even prior to crop sowing. This approach has gained popularity due to its ability to proactively manage weed populations proactively, ensuring better crop establishment and overall weed control.

- The white grub infestation reduced the root system by approximately 25% in soybeans and 64% in maize. It was observed that Phyllophaga capillata and Aegopsis bolboceridus damaged all evaluated variables, reducing overall soybean productivity by 58.62% and maize productivity by 59.76% in South American countries like Brazil. All these soil-borne pests may effectively be controlled by soil application of insecticides.

- Similarly, nematodes like Meloidogyne incognita and Pratylenchus brachyurus cause significant losses in fruit and vegetable crops. For instance, carrots are susceptible to considerable losses, averaging up to 20.0%. As these parasitic nematodes are soil-dwelling organisms, it is important to treat the soil with nematicides to kill these organisms.

Soil treatment pesticide usage is increasing with the need for controlling soil-borne diseases

- Amid the dynamic landscape of the pesticide market, soil treatment pesticides stand out as crucial components. These specialized chemicals play a pivotal role in fostering healthy crop growth, effective pest and disease control, and sustainable agricultural practices.

- Cypermethrin is a pyrethroid insecticide that may be used as a soil treatment pesticide. When applied to the soil, it provides effective control against a variety of soil-borne pests, including termites and root maggots. Cypermethrin's mode of action involves targeting the nervous system of the pests upon contact, leading to paralysis and eventual death. It was priced at USD 21.0 thousand per metric ton in 2022.

- Atrazine is an herbicide commonly used as a soil treatment to control various broadleaf and grassy weeds in agricultural fields and non-crop areas. It is particularly effective in managing weed populations that compete with crops for nutrients, water, and sunlight. In 2022, it was priced at USD 13.8 thousand per metric ton.

- Malathion is an organophosphate insecticide used as a soil treatment to control a variety of insect pests in agricultural fields and non-crop areas. It is effective in managing both flying and crawling insects that may cause damage to crops and other plants. Malathion was priced at USD 12.5 thousand per metric ton.

- Mancozeb is a fungicide and soil treatment used to control various fungal diseases such as damping-off, blight, and downy mildew. It belongs to the class of dithiocarbamates and is known for its broad-spectrum activity against a wide range of plant pathogens. In 2022, it was priced at USD 7.8 thousand per metric ton.

Soil Treatment Industry Overview

The Soil Treatment Market is moderately consolidated, with the top five companies occupying 44.67%. The major players in this market are ADAMA Agricultural Solutions Ltd, BASF SE, Bayer AG, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 Chile

- 4.3.6 China

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Myanmar

- 4.3.15 Netherlands

- 4.3.16 Pakistan

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Ukraine

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 PI Industries

- 6.4.8 Rallis India Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

土壌処理:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 323 Pages

- 納期

- 2~3営業日