予防ワクチン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Preventive Vaccines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 105 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685898

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

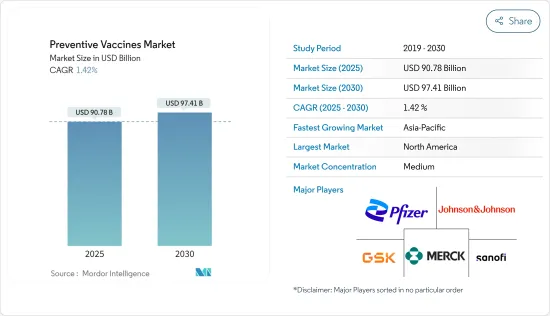

予防ワクチン市場規模は2025年に907億8,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは1.42%で、2030年には974億1,000万米ドルに達すると予測されます。

感染症の蔓延、ワクチン開発における革新的技術、政府や国際機関からの資金提供の増加、予防接種プログラムに対する政府の関心の高まりなどの要因が、市場の成長を後押ししています。

感染症の発生件数の増加は、予測期間中に予防ワクチンの需要を促進すると予想される主な要因です。例えば、2023年11月に発表された世界保健機関(WHO)のデータによると、結核はCOVID-19に次いで世界で2番目に死亡者の多い感染症でした。2022年には、世界で推定1,060万人が結核に罹患し、その内訳は男性580万人、女性350万人、小児130万人でした。さらに、米国疾病予防管理センター(CDC)によると、米国の結核罹患率は2022年の10万人当たり2.5人から2023年には2.9人となり、2024年3月には15%上昇しました。

このように、人々の間で結核の負担が増加していることから、その予防の必要性が高まっており、そのことが予測期間中の市場の成長を促進すると予測されています。さらに、世界保健機関(WHO)が2023年7月に発表したデータによると、世界全体で推定5,800万人がC型慢性肝炎ウイルスに感染しており、毎年約150万人が新たに感染しています。同資料によると、C型肝炎ウイルスは血液を媒介とする病原体であり、少量の血液にさらされることで発症するケースが最も多いです。従って、肝炎の負担増が市場の成長を促進しています。

ワクチン技術の急速な進歩は、遺伝子工学、ワクチン送達技術、プロテオミクスの導入によって促進されています。例えば、2024年1月、中国国家医薬品監督管理局は、CSPCファーマシューティカル・グループの呼吸器合胞体ウイルス(RSV)ワクチン候補に対し、ヒト臨床試験開始の規制承認を与えました。これにより、予防ワクチン製品の開発が活発化し、市場の成長が促進されると予想されます。

感染症の蔓延を防ぐための予防接種プログラムを組織する政府の取り組みが活発化し、ワクチン接種の必要性が高まっていることが、予測期間中の市場の成長を高めると予想されます。例えば、インド政府は2024年2月、子宮頸がん予防を目的とした9~14歳の女児を対象とした予防接種プログラムを開始しました。さらに、政府は対象年齢層へのワクチン接種を積極的に推進しています。したがって、こうした要因から、市場は予測期間中に成長すると予想されます。しかし、副作用のリスクやワクチン開発コストの高さが、予測期間中の市場成長の妨げになる可能性が高いです。

予防ワクチン市場の動向

肝炎分野は予測期間中に大幅な成長が見込まれる

肝炎は肝臓の炎症を特徴とし、ウイルス、アルコール、薬物などさまざまな感染源から発生する可能性があります。A型肝炎、B型肝炎、C型肝炎が主流で、それぞれ異なるウイルスに由来します。一般的な症状は、黄疸、疲労、腹部不快感などです。治療方針は、根本的な原因と症状の重症度によって決まる。

肝炎患者の増加は、効果的なワクチン接種ソリューションに対する需要の増加により、予防ワクチン市場の成長を促進すると思われます。肝炎は、特に感染率の高い地域において、依然として世界的に重要な健康問題であるため、公衆衛生への取り組みと個人の意識の両方が、ワクチン開発と流通へのより大きな投資につながっています。例えば、2024年に更新された世界保健機関(WHO)のデータによると、2022年には世界で3億400万人が慢性ウイルス性B型肝炎およびC型肝炎と診断され、さらに2022年にはこれらの慢性ウイルス性肝炎株の新規感染が220万件発生しました。そのため、肝炎患者の増加に対抗するために効果的なワクチン接種ソリューションの需要が高まるにつれ、ワクチンの開発と配布がより重視されるようになっています。予防と公衆衛生への関心の高まりは、このセグメントへの投資と技術革新を促進します。

予防ワクチン市場の推進には、ワクチン接種プログラムの推進、調査への資金提供、公衆衛生政策の実施など、政府の取り組みが重要な役割を果たしています。政府は、ワクチンへの一般市民のアクセスを向上させるため、ワクチン接種キャンペーンを実施したり、補助金を支給したり、予防接種ガイドラインを策定したりすることが多いです。例えば、2024年6月、Gaviは、エボラ出血熱、定期多価髄膜炎、ヒト狂犬病、B型肝炎の出生時投与に対する予防措置をターゲットとした新しいワクチン接種イニシアチブを発表しました。同出典によると、Gaviは低所得国への支援を拡大し、多価髄膜炎菌結合型ワクチンやB型肝炎出生用量ワクチンと並んで、曝露後予防のためのヒト狂犬病ワクチンの定期投与を促進しています。

そのため、A型肝炎、B型肝炎、C型肝炎の負担が増加していることや、肝炎予防ワクチンを後押しする政府の取り組みが増加していることなどの要因から、このセグメントは予測期間中に成長すると予想されます。

予測期間中、北米が大きな市場シェアを占める見込み

北米の予防ワクチン市場は、感染症の流行増加、ワクチン需要の増加、感染症を発症しやすい高齢者人口の増加、主要市場企業の存在などの要因により、予測期間中に成長すると予想されます。

COVID-19のような感染症の負担増は、ワクチン需要を大幅に増加させ、予防ワクチン市場を牽引しています。蔓延するアウトブレイクを抑制する緊急の必要性は、ワクチン開発を加速させ、利用可能なワクチンの範囲を広げています。このような需要の高まりは、研究への投資、ワクチン流通の改善、ワクチン接種の義務化につながります。例えば、世界保健機関(WHO)が2024年8月に発表したデータによると、メキシコでは約760万人のCOVID-19確定症例が報告されています。また、同国では2024年8月までに2億2,223万回分のワクチンが接種されました。

同じ情報源によると、米国では2024年8月までに国内で7億1,181万回分のワクチンが接種されています。従って、COVID-19のような感染症の発生は、需要を押し上げ、市場開拓を加速し、ワクチンの入手可能性を拡大することによって予防ワクチン市場を刺激し、予測期間中の市場の成長を促進すると予想されます。

予防接種プログラムの実施に政府が注力するようになったことも、市場の成長に寄与しています。例えば、2023年12月、オンタリオ州民およびその他のカナダ人は、万国共通インフルエンザ予防接種プログラム(UIIP)の下でインフルエンザワクチンを無料で利用できるようになりました。就労または就学している生後6ヵ月以上のオンタリオ州民がインフルエンザ・ワクチンの接種資格を得た。さらに、2023年2月、カナダ政府の予防接種プログラムでは、子どもは2、4、18ヵ月にポリオワクチンを接種し、その後4歳から6歳の間にブースター接種を受けるべきであると勧告しました。便宜上、DTapとHibと一緒にIPVを6ヶ月に追加接種することもできます。従って、政府主導の予防接種プログラムは、ワクチンへのアクセスを拡大し、国民の参加を促し、ワクチン開発への投資を促進することによって予防ワクチン市場を牽引しており、北米での市場開拓の原動力となっています。

また、国内での予防ワクチン開発を加速させるための政府や国際機関からの資金開拓も、市場の成長を後押しすると予想されます。例えば、米国国立衛生研究所によると、2024年3月、米国政府は2022年の3億5,900万米ドルに続き、2023年には3億6,400万米ドルを肝炎対策に割り当てた。したがって、肝炎に対する政府資金の増加は、研究の支援、生産能力の強化、ワクチン接種プログラムの拡大により、予防ワクチン市場を推進しています。このような投資は、より広範なワクチンの入手可能性と利用しやすさを促進し、最終的には肝炎の制御と予防に対する世界の取り組みを強化します。

提携、拡大、上市など、様々な事業戦略を採用する企業の注目度が高まっていることから、同市場では予防ワクチンの入手機会が創出されると予想されます。このことは、予測期間中の市場の成長を促進すると予想されます。例えば、2023年10月、ファイザーはPENBRAYAについて米国食品医薬品局(FDA)の承認を取得し、青少年および若年成人における髄膜炎菌感染症の最も一般的な5つの血清群に対する最初で唯一のワクチンとなりました。

さらに2023年8月、ファイザー社はABRYSVOの米国FDA承認を取得しました。この承認は、新生児を呼吸器合胞体ウイルス(RSV)から守るため、妊娠32週から36週の妊婦への予防接種という特定の使用事例に対するものでした。これは、出生時から生後6ヵ月までの乳児をRSVによる下気道疾患(LRTD)および重症LRTDから守るための母親用ワクチンとして、米国初で唯一の承認でした。

そのため、感染症の罹患率の高さ、予防接種プログラムやキャンペーンの増加、予防ワクチン開発のための政府資金の増加、企業活動の活発化などの要因により、予測期間中に市場は成長すると予想されます。

予防ワクチン産業の概要

予防ワクチン市場は細分化されており、複数の主要企業が参入しています。現在、市場を独占している主な企業は、GSK PLC、Johnson &Johnson Services Inc.、Merck &Co.、Pfizer Inc.、Sanofiなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 感染症の流行拡大

- ワクチン開発における革新的技術

- 政府および国際機関からの資金提供の増加

- 予防接種プログラムに対する政府の関心の高まり

- 市場抑制要因

- 副作用のリスク

- ワクチン開発コストの高さ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- ワクチンタイプ別

- 生ワクチン/弱毒化ワクチン

- 不活化ワクチン

- サブユニットワクチン

- トキソイドワクチン

- mRNAワクチン

- その他のワクチン

- 疾患タイプ別

- 肺炎球菌

- ポリオウイルス

- 肝炎

- インフルエンザ

- はしか、おたふくかぜ、風疹(MMR)

- COVID-19

- その他の疾患

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- AstraZeneca PLC

- Emergent BioSolutions Inc.

- Daiichi Sankyo Company Limited

- GSK plc

- Johnson & Johnson Services, Inc.

- Merck & Co.

- Novavax Inc.

- Pfizer Inc.

- Sanofi

- Takeda Pharmaceutical Co. Ltd

第7章 市場機会と今後の動向

目次

The Preventive Vaccines Market size is estimated at USD 90.78 billion in 2025, and is expected to reach USD 97.41 billion by 2030, at a CAGR of 1.42% during the forecast period (2025-2030).

Factors such as the growing prevalence of infectious diseases, innovative technology in vaccine development, increased funding from government and international organizations, and the increasing government focus on immunization programs are boosting the market's growth.

The rising incidences of infectious diseases are the key factor expected to drive the demand for preventive vaccines over the forecast period. For instance, according to the World Health Organization data published in November 2023, tuberculosis was the second most deadly infectious disease globally, following COVID-19. In 2022, an estimated 10.6 million individuals globally contracted tuberculosis (TB), comprising 5.8 million men, 3.5 million women, and 1.3 million children. Additionally, per the Centers for Disease Control and Prevention (CDC), the US TB rate climbed by 15% in March 2024, from 2.5 per 100,000 individuals in 2022 to 2.9 in 2023.

Thus, the rising burden of tuberculosis among the population increases the need for its prevention, which, in turn, is anticipated to propel the market's growth over the forecast period. Additionally, according to data published by the World Health Organization (WHO) in July 2023, globally, an estimated 58 million people had chronic hepatitis C virus, and about 1.5 million new infections occur annually. According to the same source, the hepatitis C virus is a blood-borne pathogen, and the most common form of the disease is exposure to small amounts of blood. Thus, the increasing burden of hepatitis is propelling the growth of the market.

The rapid advancements in vaccine technology are fueled by the introduction of genetic engineering, vaccine-delivering technology, and proteomics. For instance, in January 2024, the National Medical Products Administration of China granted regulatory approval for CSPC Pharmaceutical Group's candidate vaccine for the respiratory syncytial virus (RSV) to commence human clinical trials. This is expected to increase the development of preventive vaccine products, bolstering the market's growth.

Rising government initiatives in organizing immunization programs to prevent the spread of infectious diseases and the need for vaccination are expected to increase the market's growth over the forecast period. For instance, in February 2024, the Government of India initiated a vaccination program targeting girls aged 9 to 14 aimed at preventing cervical cancer. Furthermore, the government is actively promoting this vaccination among the eligible age group. Therefore, owing to these factors, the market is expected to grow over the forecast period. However, the risk of adverse effects and the high cost of vaccine development will likely impede the market's growth over the forecast period.

Preventive Vaccines Market Trends

The Hepatitis Segment is Expected to Witness Significant Growth Over the Forecast Period

Hepatitis, characterized by liver inflammation, can arise from various sources, including viruses, alcohol, and drugs. The predominant strains are hepatitis A, B, and C, each stemming from distinct viruses. Common symptoms encompass jaundice, fatigue, and abdominal discomfort. Treatment strategies hinge on the underlying cause and the condition's severity.

The rise in hepatitis cases is likely to drive the growth of the preventive vaccines market due to increasing demand for effective vaccination solutions. As hepatitis remains a significant global health issue, especially in areas with high infection rates, both public health initiatives and individual awareness are leading to more substantial investment in vaccine development and distribution. For instance, according to the World Health Organization data updated in 2024, in 2022, 304 million individuals globally were diagnosed with chronic viral hepatitis B and C. Further, 2.2 million new infections of these chronic viral hepatitis strains occurred in 2022. Therefore, as the demand for effective vaccination solutions increases to combat the rising number of hepatitis cases, there is a stronger emphasis on developing and distributing vaccines. This heightened focus on prevention and public health drives investment and innovation in the segment.

Government initiatives play a crucial role in driving the preventive vaccines market by promoting vaccination programs, funding research, and implementing public health policies. Governments often launch vaccination campaigns, provide subsidies, and establish immunization guidelines to enhance public access to vaccines. For instance, in June 2024, Gavi unveiled new vaccination initiatives targeting preventive measures against Ebola, routine multivalent meningitis, human rabies, and the hepatitis B birth dose. As per the same source, Gavi is extending its support to lower-income nations, facilitating the routine administration of the human rabies vaccine for post-exposure prophylaxis alongside the multivalent meningococcal conjugate and hepatitis B birth dose vaccines.

Therefore, the segment is expected to grow over the forecast period due to factors such as the rising burden of hepatitis A, B, and C and increasing government initiatives to boost the preventive vaccines for hepatitis.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

The preventive vaccines market in North America is expected to grow over the forecast period owing to factors such as the rising prevalence of infectious diseases, increasing demand for vaccines, growing geriatric population prone to develop infectious diseases, and the presence of key market players.

The rising burden of infectious diseases, such as COVID-19, drives the preventive vaccines market by significantly increasing vaccine demand. The urgent need to control widespread outbreaks accelerates vaccine development and broadens the range of available vaccines. This heightened demand leads to more significant investment in research, improved vaccine distribution, and the implementation of vaccination mandates. For instance, according to data published by the World Health Organization (WHO) in August 2024, about 7.6 million confirmed cases of COVID-19 were reported in Mexico. In addition, 222.23 million vaccine doses had been administered in the country by August 2024.

According to the same source, 711.81 million vaccine doses had been administered in the country by August 2024 in the United States. Therefore, the outbreak of infectious diseases like COVID-19 stimulates the preventive vaccines market by boosting demand, accelerating development, and expanding vaccine availability, which is expected to fuel the market's growth over the forecast period.

Increasing government focus on organizing immunization programs also contributes to the market's growth. For instance, in December 2023, Ontarians and other Canadians accessed free influenza vaccines under the Universal Influenza Immunization Program (UIIP). Ontario residents aged six months and older who work or attend school qualified for the influenza vaccine. Additionally, in February 2023, the Canadian government's immunization program advised that children should receive the polio vaccine at 2, 4, and 18 months, followed by a booster dose between the ages of 4 and 6. An extra dose of IPV can be given at six months, alongside DTap and Hib, for convenience. Therefore, government-led immunization programs drive the preventive vaccines market by expanding vaccine access, increasing public participation, and fostering investment in vaccine development, which will drive market growth in North America.

Growing funding from government and international organizations to accelerate the development of preventive vaccines in the country is also expected to boost the market's growth. For instance, according to the National Institute of Health, in March 2024, the US government allocated USD 364 million to combat hepatitis in 2023, following a USD 359 million investment in 2022. Therefore, increasing government funding for hepatitis propels the preventive vaccines market by supporting research, enhancing production capabilities, and expanding vaccination programs. Such investments foster broader vaccine availability and accessibility, ultimately strengthening global efforts to control and prevent hepatitis.

The rising focus of companies on adopting various business strategies, such as collaboration, expansion, and launches, is expected to create opportunities for the availability of preventive vaccines in the market. This is anticipated to fuel the market's growth over the forecast period. For instance, in October 2023, Pfizer received US Food and Drug Administration (FDA) approval for PENBRAYA, making it the first and only vaccine against the five most common serogroups of meningococcal disease in adolescents and young adults.

In addition, in August 2023, Pfizer received US FDA approval for ABRYSVO. This approval was for a specific use case: immunization of pregnant women between 32 and 36 weeks of gestation to protect their newborns from respiratory syncytial virus (RSV). It was the first and only US approval for a maternal vaccine to help protect infants at birth through six months of life from lower respiratory tract disease (LRTD) and severe LRTD due to RSV.

Therefore, the market is expected to grow over the forecast period due to factors such as the high incidences of infectious diseases, increasing immunization programs and campaigns, growing government funding for developing preventive vaccines, and increasing company activities.

Preventive Vaccines Industry Overview

The preventive vaccines market is fragmented and consists of several major players. A few of the major players currently dominating the market in terms of market share include GSK PLC, Johnson & Johnson Services Inc., Merck & Co., Pfizer Inc., and Sanofi.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence of Infectious Diseases

- 4.2.2 Innovative Technology in Vaccine Development

- 4.2.3 Increased Funding from Government and International Organizations

- 4.2.4 Increasing Government Focus on Immunization Programs

- 4.3 Market Restraints

- 4.3.1 Risk of Adverse Effects

- 4.3.2 High Cost of Vaccine Development

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Vaccine Type

- 5.1.1 Live/Attenuated Vaccines

- 5.1.2 Inactivated Vaccines

- 5.1.3 Subunit Vaccines

- 5.1.4 Toxoid Vaccines

- 5.1.5 mRNA Vaccines

- 5.1.6 Other Vaccine Types

- 5.2 By Disease Type

- 5.2.1 Pneumococcal

- 5.2.2 Poliovirus

- 5.2.3 Hepatitis

- 5.2.4 Influenza

- 5.2.5 Measles, Mumps, and Rubella (MMR)

- 5.2.6 COVID-19

- 5.2.7 Other Disease Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AstraZeneca PLC

- 6.1.2 Emergent BioSolutions Inc.

- 6.1.3 Daiichi Sankyo Company Limited

- 6.1.4 GSK plc

- 6.1.5 Johnson & Johnson Services, Inc.

- 6.1.6 Merck & Co.

- 6.1.7 Novavax Inc.

- 6.1.8 Pfizer Inc.

- 6.1.9 Sanofi

- 6.1.10 Takeda Pharmaceutical Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 105 Pages

- 納期

- 2~3営業日