|

市場調査レポート

商品コード

1685896

ベトナムのペットフード:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Vietnam Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ベトナムのペットフード:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 279 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

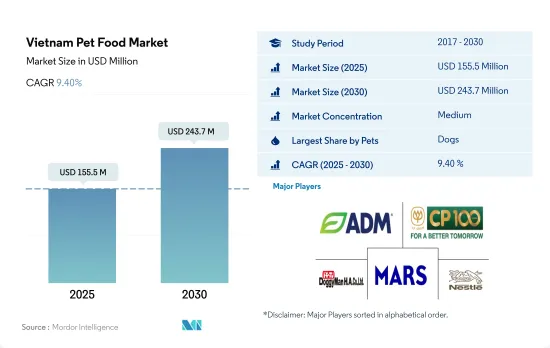

ベトナムのペットフード市場規模は2025年に1億5,550万米ドルと推定され、2030年には2億4,370万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは9.40%で成長する見込みです。

犬は他のペットに比べて人口が多く、一人当たりの消費量も多いため、ベトナムのペットフード市場を席巻

- ベトナムはペットフード産業が急成長している国の一つであり、ペットの親として若年層やティーンエイジャーが多く存在することも、ベトナムのペットフード市場を牽引するいくつかのユニークな要因の一つです。2022年、ベトナムのペットフード市場はアジア太平洋ペットフード市場の0.4%を占めたが、若年層のサラリーマン化に伴い、同国のシェアは今後数年で急速に拡大すると予想されます。このため、同国では今後数年間、高品質のペットフード製品に対する需要が高まると予測されます。

- 過去の期間において、同国のペットフード市場は2017年から2021年の間に81%増加しました。この期間の市場の成長は、市販のペットフード製品の使用量の増加と国内のペット数の増加によるものです。

- ベトナムのペットフード市場では犬が主要なペットセグメントを占めており、そのシェアは2022年に7,640万米ドルに達します。犬のシェアが高いのは、ペット全体の中でも人口が多く、ペットフードの消費量が比較的多いためです。犬は2022年の国内ペット数の45.1%を占めています。

- 猫およびその他の動物は、犬に次いでベトナムのペットフード市場の主要シェアを占めており、2022年にはそれぞれ38%、16.9%のシェアを占める。しかし、猫が市場で最も急成長しているペット・セグメントを構成しており、予測期間中にCAGR 10.7%を記録すると予想され、ペット所有者の可処分所得の増加が、手作りフードから市販フードへのシフトを促進しています。

- 業務用ペットフードの利用増加や若年層におけるペット飼育の増加は、予測期間中、同国のペットフード市場を牽引すると予測されます。

ベトナムのペットフード市場動向

ベトナムの文化では猫は幸運の動物と考えられており、これが同国でのペットとしての猫の飼育を促進すると予想されます。

- ベトナムでは、ペットとして猫を飼う人気が高まっています。そのため、猫の飼育数は2019年から2022年の間に28.5%も大幅に増加しています。主に中間層の増加がこの動向を後押ししています。また、猫の独特な性格や行動に対する嗜好の変化も、猫の飼育を促進しています。ベトナムの文化では、猫は縁起の良い動物とされ、猫を飼う家庭に幸運をもたらすと信じられています。

- 同国における猫の飼育数は、犬の飼育数に比べて伸び悩んでいます。猫を飼う世帯数は2016年の11.3%から2020年には12.4%に増加します。2022年時点で、ベトナムのペット総飼育数に占める猫の割合は約38.0%です。このように猫がかなりの割合を占めるようになったのは、主に若い世代を中心に飼い猫が増加傾向にあるためです。

- ベトナムのペット猫の飼育数はかなり多いにもかかわらず、ベトナムのペット猫の飼育数は、違法、非人道的、危険な猫肉取引による深刻な脅威に直面しています。毎日、何千匹ものペットの猫が、横行する盗難によって姿を消しています。しかし、ベトナム政府は猫の食肉取引を禁止するために厳しい措置をとっています。政府と非政府組織の両方が、猫の養子縁組を促進し、国内で責任ある猫の飼い方を訓練しています。オフラインやオンライン小売店を通じてペット用猫製品へのアクセスが容易であること、猫カフェや公園への関心が高まっていることが、全国的に猫の飼育や所有が増加している要因です。このような要因により、予測期間中に猫のペット数が増加すると予想されます。

ベトナムでは中価格帯のペットフードが最も需要の高い食品であり、ペットの健康に対する意識の高まりがベトナムでのペット支出を促進しています。

- ベトナムでは、ペットフード製品の価格上昇や、ペットの親がカスタマイズされた食事を好むことから、ペット支出が増加する傾向が見られます。犬は糖尿病や肥満などの病気にかかりやすいため、他のペットに比べて大量のペットフードを必要とします。このような要因により、ペット支出における犬のシェアが高まり、2022年には39%を占めるようになりました。

- ベトナムのペット保護者は、インド、中国、韓国、オーストラリアなどの他のアジア太平洋諸国と比較して所得が低いため、高価格のペットフードに比べ、中価格のペットフードを購入し続けると予想されます。中価格帯のペットフードは、特殊なペットフードに対する認識が高まっているため、ペットにより多く与えられると予想されます。ミレニアル世代のペットの親はペットと過ごす時間を増やし、より多くのブランドペットフードを購入すると予想されるため、カテゴリーがさらに開発され、ペットフードへの支出が増加します。

- ペットフードの販売は主にペットショップや食料品小売店を通じて行われているが、オンライン小売店を通じての販売も増加しています。例えば、2020年には、食料品専門店以外を通じたペットフードの売上が国内のペットフード売上の72.8%を占めたのに対し、eコマースを通じた売上は3.1%であり、予測期間中のCAGRは7.7%を記録すると予想されます。健康上の懸念に対する意識の高まりや、ペットの親が購入する中価格帯の製品の増加は、予測期間中に同国でペットの支出を増加させる要因になると予想されます。

ベトナムのペットフード産業概要

ベトナムのペットフード市場は適度に統合されており、上位5社で61.44%を占めています。この市場の主要企業は以下の通りです。ADM, Charoen Pokphand Group, DoggyMan H. A., Mars Incorporated and Nestle(Purina)(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他のペット

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品/サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用おやつ

- サブ製品別

- クランキートリーツ

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&チューイートリーツ

- その他のおやつ

- ペット用獣医食

- サブ製品別

- 糖尿病

- 消化器過敏症用

- オーラルケア

- 腎臓

- 尿路疾患

- その他の獣医食

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンライン・チャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Alltech

- Charoen Pokphand Group

- DoggyMan H. A. Co., Ltd.

- EBOS Group Limited

- Mars Incorporated

- Nestle(Purina)

- Schell & Kampeter Inc.(Diamond Pet Foods)

- Vafo Praha, s.r.o.

- Virbac

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 49083

The Vietnam Pet Food Market size is estimated at 155.5 million USD in 2025, and is expected to reach 243.7 million USD by 2030, growing at a CAGR of 9.40% during the forecast period (2025-2030).

Dogs dominated the Vietnamese pet food market due to their larger population and higher per capita consumption compared to other pets

- Vietnam is home to one of the fastest-growing pet food industries, and the significant presence of younger adults and teenagers as pet parents in the country is also one of several unique factors driving the country's pet food market. In 2022, the Vietnamese pet food market accounted for 0.4% of the Asia-Pacific pet food market, but the country's share is anticipated to grow faster in the coming years as younger adults become salaried. This is projected to increase the demand for high-quality pet food products in the country over the coming years.

- During the historical period, the pet food market in the country increased by 81% between 2017 and 2021. The growth in the market during the period was because of the increasing usage of commercial pet food products and the rising pet population in the country.

- Dogs comprise the major pet segment in the Vietnamese pet food market, with its share amounting to USD 76.4 million in 2022. The higher share of these pets was because of their larger population among all pets and comparatively higher consumption of pet food. Dogs accounted for 45.1% of the pet population in the country in 2022.

- Cats and other animals occupied the major share of the Vietnamese pet food market after dogs, with shares of 38% and 16.9%, respectively, in 2022. However, cats comprise the fastest-growing pet segment in the market, expected to register a CAGR of 10.7% during the forecast period, with increasing disposable incomes of pet owners driving the shift from homemade foods to commercial foods.

- The increasing usage of commercial pet food products and growing pet adoption among younger adults are estimated to drive the pet food market in the country during the forecast period.

Vietnam Pet Food Market Trends

Cats are considered lucky in Vietnamese culture which is anticipated to drive the cat adoption as pets in the country

- In Vietnam, owning a cat as a pet has become increasingly popular. Thus, the cat population has significantly increased by 28.5% between 2019 and 2022. The growing middle class mainly drives this trend. The changing preference toward cat ownership for their distinct personalities and behavior is also enhancing the adoption of cats. In Vietnamese culture, cats are considered lucky animals and are believed to bring good fortune to households that own them.

- Cat ownership in the country is growing at a slower rate compared to dog ownership. The number of households owning cats increased from 11.3% in 2016 to 12.4% in 2020. As of 2022, the pet cat population accounted for about 38.0% of the total pet population in Vietnam. This considerable share of cats is mainly because of the increasing trend in pet cat ownership, particularly among young age people.

- Despite the significant pet cat population in the country, the pet cat population in Vietnam is facing a serious threat from the illegal, inhumane, and hazardous cat meat trade, which has resulted in cat owners living in constant fear of their pets being stolen and slaughtered for human consumption. Every day, thousands of pet cats are disappearing due to rampant theft. However, the Vietnamese government has taken stringent measures to ban the cat meat trade. Both government and non-government organizations promote the adoption of cats and train responsible cat ownership in the country. Easy accessibility to pet cat products through offline and online retail stores and growing interest in cat cafes and parks are the factors contributing to the increasing adoption or ownership of cats across the country. Such factors are anticipated to rise in the overall pet cat population during the forecast period.

Mid-priced pet foods are the most demanded food products in the country, and increasing awareness of pet health is driving pet expenditure in Vietnam

- In Vietnam, a trend of increasing pet expenditure has been witnessed due to an increase in the prices of pet food products and pet parents preferring customized diets. Dogs are more prone to diseases such as diabetes and obesity; thus, they require large quantities of pet food as compared to other pets. These factors increased the share of dogs in the pet expenditure and attained a higher share in the pet expenditure as they accounted for 39% in 2022.

- Pet parents in Vietnam are expected to continue purchasing pet food that is mid-priced as compared to high-priced pet food due to low income compared to other Asia-Pacific countries such as India, China, South Korea, and Australia. Mid-priced pet food is expected to be given more to pets as there is growing awareness about specialized pet food. Millennial pet parents are expected to spend more time with pets and purchase more branded pet food, which expands further category development and increases expenditure on pet food.

- Sales of pet foods are mostly through pet shops and grocery retailers, whereas there is an increase in the sales of pet food through online retailers. For instance, in 2020, pet food sales through non-grocery specialist stores accounted for 72.8% of the pet food sales in the country, whereas sales through e-commerce accounted for 3.1%, which is expected to register a CAGR of 7.7% during the forecast period. The growing awareness about health concerns and the rise in mid-priced products purchased by pet parents are the factors expected to help in increasing pet expenditure in the country during the forecast period.

Vietnam Pet Food Industry Overview

The Vietnam Pet Food Market is moderately consolidated, with the top five companies occupying 61.44%. The major players in this market are ADM, Charoen Pokphand Group, DoggyMan H. A. Co., Ltd., Mars Incorporated and Nestle (Purina) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Alltech

- 6.4.3 Charoen Pokphand Group

- 6.4.4 DoggyMan H. A. Co., Ltd.

- 6.4.5 EBOS Group Limited

- 6.4.6 Mars Incorporated

- 6.4.7 Nestle (Purina)

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 Vafo Praha, s.r.o.

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms