|

市場調査レポート

商品コード

1849920

バイオセラミックス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Bioceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バイオセラミックス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月13日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

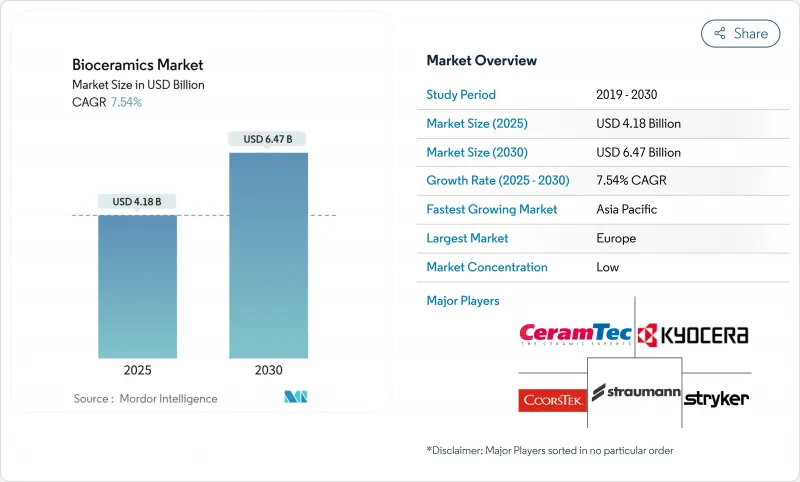

バイオセラミックス市場規模は2025年に41億8,000万米ドルと推定・予測され、予測期間(2025-2030年)のCAGRは7.54%で、2030年には64億7,000万米ドルに達すると予測されています。

筋骨格系および歯科処置の増加、3Dプリンティングによって製造される患者固有のインプラントの幅広い採用、耐久性と生体適合性の高い材料を求める高齢化社会が、バイオセラミックス市場を推進しています。欧州とアジア太平洋地域では、高度な整形外科手術と歯科治療に対する規制当局の支援、デジタルワークフローに対する病院の投資が需要をさらに加速させています。業界大手は、材料の優位性と生産効率を確保するために、買収、プロセス革新、研究機関との共同開発プログラムを追求しているため、競合の激しさは依然として高いです。

世界のバイオセラミックス市場の動向と洞察

北米における3Dプリントカスタムバイオセラミックインプラントの急速な普及

米国およびカナダの病院では現在、患者に適合した形状を最適化された空隙率で提供する高密度セラミック積層造形ラインを統合しています。層ごとの制御はオッセオインテグレーションを改善し、以前はコストのかかる機械加工が必要であった軽量格子形状を可能にします。臨床のフィードバックによると、これらの構造を採用した頭蓋顔面および脊椎インプラントの再置換率が減少しています。

欧州で加速する歯科インプラント普及がジルコニア需要を押し上げる

ドイツ、フランス、イタリアでは、患者が自然な歯列を模倣した審美性を求めているため、メタルフリーのプロトコルが急速に成長しています。ツーピース・ジルコニア・システムは、補綴物の柔軟性に関する以前の問題を解決し、軟組織の反応を犠牲にすることなく、幅広い臨床適応を可能にします。ジルコニアをベースとしたフィクスチャーの5年生存率は94~98.4%であり、チタンとほぼ同等の結果が得られています。半透明ジルコニア用のチェアサイド・ミリング・ユニットに早くから投資してきたラボは、現在、より早い納期から利益を得ています。チタンに特化したOEMは、競争力を取り戻すためにライセンシング契約や買収を通じて調整しています。

FDAのナノセラミック分散ガイドラインの厳格化により承認が遅れる

米国の規制当局は現在、ナノスケールセラミックを組み込んだ装置について、粒子の移動と凝集挙動に関する徹底的なデータを要求しています。平均審査期間は最大14ヶ月長くなり、小規模なイノベーターの資本要件を引き上げています。社内に毒物学研究所を持つ大企業は、このハードルを活用して競争力を強化し、プロトタイプが後期試験に達した後に共同開発契約を結ぶことが多いです。業界コンソーシアムは、バリデーション・サイクルを短縮する可能性のある参照標準に取り組んでいるが、2027年までに目に見える形で緩和される可能性は低いです。

セグメント分析

酸化アルミセグメントはバイオセラミックス市場規模の49%に相当します。アルミナの圧縮強度と耐摩耗性が、股関節と膝関節のベアリングにおける優位性を支えています。サブミクロン粒径の高純度グレードは、マイクロクラックを発生させることなく繰り返し荷重に耐え、人工関節の耐用年数を延ばすことができるため、人気を集めています。同時に行われる表面コーティングの研究は、アルミナインプラントを二重機能部品として位置づけ、生物活性を付加することを目的としています。2025年から2030年にかけて、この材料はCAGR 7.89%を記録し、脊椎ケージと縫合アンカーにおける新たな需要に支えられています。

2024年には粉末製品がバイオセラミックス市場シェアの48%を占める。顆粒の流動性向上により、コンティニュアス・フィード・プレスやバインダー・ジェット・プリンターが最小限の後処理でネットシェイプに近い部品を提供できるようになりました。噴霧乾燥と造粒技術の革新により、バイオセラミック粉末の流動性と圧縮性が向上し、自動製造との適合性が高まり、製造コストが削減されました。注入可能な液体は、外科医に不規則な欠陥に適合する硬化の早いペーストを提供することで、CAGR 7.75%で上昇しています。

地域分析

欧州は2024年の世界売上高の43%を占め、成熟した保険償還の枠組みと深い材料科学能力を示しています。ドイツは人工股関節置換術の技術革新を主導し、英国は歯周病再生のための生物活性ガラス研究を進めています。

アジア太平洋は2025-2030年のCAGRが8.01%と最も高いです。中国の中央集権的な調達政策は現在、現地調達に有利なものとなっており、焼結炉や噴霧乾燥ラインへの投資に拍車をかけています。日本はセラミックの伝統を活用し、皮質から海綿への移行を模倣した勾配構造を開拓します。インドと韓国はデンタル・ツーリズムを拡大し、世界的な認定基準を満たすジルコニア・インプラントを採用する医院の意欲を高めています。

北米は依然として技術革新の坩堝です。先進的な病院では、手術室に隣接する付加製造室を統合し、設計からインプラント埋入までのサイクルを72時間以内に短縮しています。ラテンアメリカと中東は、保険の適用範囲が広がるにつれて新たな収益プールを提供しているが、滅菌ロジスティクスに関わるサプライチェーンの課題により、地域ごとの流通ハブが必要とされています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 北米における3Dプリントカスタムバイオセラミックインプラントの急速な普及

- 欧州における歯科インプラント普及の加速がジルコニア需要を押し上げる

- 政府の脊椎手術拡大がリン酸カルシウムの使用を促進

- 硬組織および軟組織置換の需要増加

- OEMは関節置換において金属ベアリングから生体不活性セラミックベアリングに移行している

- 市場抑制要因

- FDAのナノセラミック分散ガイドラインの厳格化により承認が遅れる

- 代替品の脅威

- 焼結の高エネルギーコストがメーカーの利益を圧迫

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 素材タイプ別

- 酸化アルミニウム

- ジルコニア

- リン酸カルシウム

- 汎用

- ハイドロキシアパタイト

- 硫酸カルシウム

- 炭素

- ガラス

- 形態別

- 粉

- 液体(注射剤)

- その他の形式

- タイプ別

- バイオイナート

- バイオアクティブ

- 生体吸収性

- 用途別

- 整形外科

- 歯科

- バイオメディカル

- エンドユーザー業界別

- 病院と外科センター

- 歯科医院と歯科技工所

- 調査・学術機関

- バイオテクノロジーおよび製薬会社

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他のアジア

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Berkeley Advanced Biomaterials

- BoneSupport AB

- CAM Bioceramics

- CeramTec GmbH

- CGbio

- CoorsTek Inc.

- CTL Amedica

- Dentsply Sirona

- dsm-firmenich

- FKG Dentaire Sarl

- Himed

- Institut Straumann AG

- Jyoti Ceramic

- KYOCERA Corporation

- Medical Device Business Services, Inc.

- Morgan Advanced Materials

- Sagemax

- Shandong Sinocera Functional Materials Co., Ltd.

- Stryker

- TOSOH CERAMICS CO., LTD.

- Zimmer Biomet