民間航空宇宙訓練・シミュレーション:市場シェア分析、産業動向、成長予測(2025年~2030年)

Civil Aerospace Training And Simulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685892

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

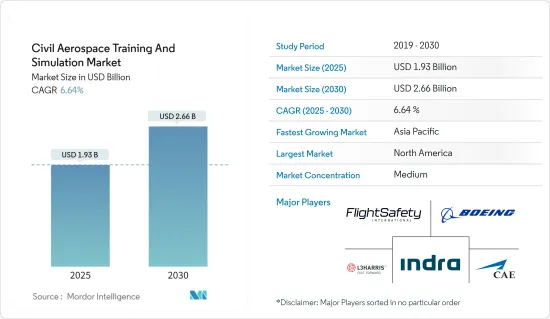

民間航空宇宙訓練・シミュレーション市場規模は、2025年に19億3,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは6.64%で、2030年には26億6,000万米ドルに達すると予測されています。

世界中の航空会社は、COVID-19パンデミックが出現する以前は、機体の拡大やネットワークの拡張計画を積極的に推進していました。しかし、COVID-19パンデミックの影響を受けて、航空会社は航空機の発注をキャンセルしたり延期したりしたほか、パンデミックの影響による損失を軽減するためにパイロットを一時解雇しました。航空業界は2022年に回復を始め、徐々にCOVID-19以前の水準に戻っています。IATA、ICAO、国際空港評議会(ACI)、国連世界観光機関(UNWTO)、世界貿易機関(WTO)、国際通貨基金(IMF)の最新情報によると、2022年の国際航空旅客輸送量は2021年に比べて改善しています。2022年の航空業界の回復に伴い、民間航空機の受注と納入が徐々に増加し、シミュレーターと訓練装置の需要も同時に増加しました。

航空産業がCOVID以前の水準に戻り、民間航空機の保有機数が増加すると予想されるため、パイロットの需要も増加すると予想されます。また現在、多くの航空会社がパイロット不足の問題に直面しており、日々の運航に影響が出ています。一般に、12時間を超えるフライトには4人のパイロットのチームが必要です。しかし、いくつかの航空会社では、パイロット不足のため、いまだに3人のパイロットでそうした長距離路線を運航しています。また、予測期間中に有人宇宙探査プログラムへの投資が計画されていることから、今後数年間は宇宙飛行士用シミュレータや訓練ソリューションの需要が見込まれます。

民間航空宇宙訓練・シミュレーション市場の動向

予測期間中、フルフライトシミュレータ(FFS)セグメントが最も高い市場シェアを占める見込み

フルフライトシミュレータ(FFS)セグメントが市場を独占しており、今後もこの傾向が続くと予想されます。フルフライトシミュレータは、一般的に飛行の動きを再現するモーションアクチュエータを装備しており、シミュレータ内で実生活に近い体験を提供することで、航空宇宙産業や航空産業の訓練生が完全な訓練体験を受けることができます。訓練された経験豊富なパイロットが不足する中、航空会社や企業はパイロット訓練プログラムに取り組んでおり、フルフライトシミュレーターの市場は拡大しています。2022年8月、CAE Inc.はカンタスグループとシドニーにおける新しいパイロット訓練センターの開発・運営に関する15年契約を締結したと発表しました。CAEは新しいA320フルフライトシミュレーターを配備し、カンタスグループからB787、A330、B737NGフルフライトシミュレーターを購入します。現在、最新鋭のFFSは、パイロットの訓練効率を向上させるため、バーチャルリアリティなどの新技術と統合されつつあります。

例えば、2022年4月、メキシコ連邦民間航空局は、アエロメヒコの2機目となるCAE 7000XRボーイング737 MAX FFSに認証を与えました。同航空会社は、旅行需要の増加と保有機の増加に伴い、訓練要件に対応するためにこのシミュレータを取得しました。2022年5月、CAEは世界航空訓練サミット(WATS)において、CAE 7000XRボーイング787およびCAE 7000XRボーイングB737 MAXフルフライトシミュレーター(FFS)を配備する目的で、トロント訓練センターを拡張すると発表しました。COVID-19の大流行後、国際線の利用が通常レベルに戻りつつあるカナダの航空会社をサポートするためだと、CAEの社長は述べています。

このような開発は、予測期間におけるフルフライトシミュレータ(FFS)分野の成長軌道を補完するものと思われます。

予測期間中、アジア太平洋が最も高い成長を記録する見込み

アジア太平洋における旅客輸送量の増加は、同地域の航空会社や航空機運航会社による新しい航空機の調達を促進しています。中国東方航空、中国南方航空、中国国際航空、インディゴ、大韓航空、全日空など、この地域の主要航空会社は、予測期間中に莫大な航空機の発注を予定しています。ボーイング社によると、アジア太平洋では今後20年間に24万4,000人以上の新規パイロットの需要があり、中国だけでも12万6,000人の需要があります。

それに伴い、中国では民間航空飛行訓練とシミュレーションに関する重要な開発が行われています。例えば、2023年4月、ボーイングは、2018年と2019年に2件の死亡事故が発生し、世界的に接地されることになったB737 MAXのパイロット訓練を中国で改善するという約束を果たすため、上海の訓練センターにB737 MAXのフライトシミュレーターを導入したと発表しました。さらに、米国の航空機メーカーは、中国の航空会社の運航をよりよくサポートするために、上海浦東国際空港の訓練ハブにB737 MAX飛行訓練装置を設置しました。インドにおけるパイロット訓練能力を高めるため、ALSIMは2021年2月、インド空港庁(AAI)から単通路機用のEASA Flight Navigation and Procedure Trainer(FNPT)マルチ・クルー・コーディネーション(MCC)レベルIIタイプのフライトシミュレータ訓練装置(FSTD)シミュレータ3機を受注しました。3台のFNPT IIシミュレータはすべて、2022年までにCATCプラヤグラージ、HTCハイデラバード、NIATAMゴンディアの訓練センターで使用開始される予定です。また、この地域の主要国は有人宇宙探査計画を加速させています。例えば、中国は現在、2022年までに完成予定の新宇宙ステーションの建設に取り組んでおり、2030年までに深宇宙有人宇宙飛行を実施する予定です。このような有人宇宙探査計画は、予測期間中に宇宙シミュレーションと訓練ソリューションの需要を促進すると予想されます。

民間航空宇宙訓練・シミュレーション産業の概要

民間航空宇宙訓練・シミュレーション市場は半固体化しています。民間航空宇宙訓練・シミュレーション市場の有力企業には、L3Harris Technologies Inc.、The Boeing Company、CAE Inc.、FlightSafety International、Indra Sistemas S.A.などがいます。

CAE Inc.は、その世界のプレゼンスとブランドイメージにより、民間航空シミュレーターで過半数のシェアを占めています。同社は、2021年度には民間航空会社向けに36台のフルフライトシミュレーターを納入したが、2022年度には30台のFFSを納入した(前年同期比6台減)。

同様に、ロッキード・マーチン社やボーイング社は、NASAの有人宇宙探査プログラムを支援している著名な企業です。訓練用の高度な機能を備えた新型シミュレータの開発に向けた各社の投資が増加していることから、今後数年間は同市場での成長機会が見込まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- シミュレータータイプ

- フルフライトシミュレータ(FFS)

- フライト訓練装置(FTD)

- その他の訓練装置

- 用途

- 民間航空

- 宇宙

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- L3Harris Technologies, Inc.

- CAE Inc.

- The Boeing Company

- FlightSafety International Inc.

- Raytheon Technologies Corporation

- Indra Sistemas S.A.

- ALSIM EMEA

- ELITE Simulation Solutions AG

- Multi Pilot Simulations BV

- Lockheed Martin Corporation

第7章 市場機会と今後の動向

- パイロット養成分野における技術の進歩

目次

The Civil Aerospace Training And Simulation Market size is estimated at USD 1.93 billion in 2025, and is expected to reach USD 2.66 billion by 2030, at a CAGR of 6.64% during the forecast period (2025-2030).

Airlines around the globe were aggressively pursuing fleet expansion and network expansion plans before the emergence of the COVID-19 pandemic. However, following the impact of the COVID-19 pandemic, the airlines have canceled and deferred aircraft orders as well as furloughed their pilots to mitigate the losses due to the impact felt by the pandemic. The aviation industry started recovering in 2022 and gradually returning to its pre-COVID-19 level. According to the latest updates from IATA, ICAO, the Airports Council International (ACI), the UN World Tourism Organization (UNWTO), the World Trade Organization (WTO), and the International Monetary Fund (IMF), the international air passenger traffic in 2022 has improved compared to that of 2021. With the recovery of the aviation industry in 2022, the orders and deliveries of commercial aircraft witnessed a gradual increase, which led to a simultaneous increase in demand for simulators and training devices.

As the aviation industry is expected to return to pre-COVID levels and the fleet of commercial aircraft is expected to increase, the demand for pilots is also expected to increase. Also, currently, many airlines are facing the issue of a pilot shortage, which is affecting their daily operations. Generally, flights longer than 12 hours require a team of four pilots. However, several airlines are still operating such long-haul routes with three pilots due to a shortage of pilots. The shortage of pilots is expected to drive demand for new simulation and training solutions.Also, the planned investments in human space exploration programs during the forecast period are anticipated to generate demand for simulators for astronauts and training solutions in the coming years.

Civil Aerospace Simulation and Training Market Trends

Full Flight Simulator (FFS) Segment Expected to Account for the Highest Market Share During the Forecast Period

The full flight simulator (FFS) segment dominated the market and is expected to continue in the coming years. The full flight simulator is generally equipped with a motion actuator that replicates flight movement, offering a real-life-like experience inside the simulator that will allow trainees in the aerospace and aviation industries to receive a complete training experience. With the lack of trained and experienced pilots, airlines and companies are working on pilot training programs, which increases the market for full-flight simulators. In August 2022, CAE Inc. announced that it had signed a 15-year contract with Qantas Group for the development and operation of a new pilot training center in Sydney. CAE will deploy a new A320 full-flight simulator and purchase B787, A330, and B737NG full-flight simulators from the Qantas Group. Currently, the new and advanced FFS is being integrated with new technologies, like virtual reality, to improve the efficiency of training pilots.

For instance, in April 2022, the Mexican Federal Civil Aviation Agency awarded certification to Aeromexico's second CAE 7000XR Boeing 737 MAX FFS. The airline acquired the simulator to cater to its training requirements as travel demand increased and its fleet grew. In May 2022, at the World Aviation Training Summit (WATS), CAE announced that it was expanding its Toronto Training Center for the purpose of deploying a CAE 7000XR Boeing 787 and a CAE 7000XR Boeing B737 MAX full-flight simulators (FFS). The president of CAE has said that this is to support Canadian airlines as international air travel is returning to normal levels after the COVID-19 pandemic.

Such developments in the market are likely to supplement the growth trajectory of the full flight simulator (FFS) segment over the forecast period.

Asia-Pacific is Anticipated to Register the Highest Growth During the Forecast Period

The increasing passenger traffic in the Asia-Pacific region is propelling the procurement of new aircraft by the airlines and aircraft operators in the region. Major airlines in the region, like China Eastern Airlines, China Southern Airlines, Air China, Indigo, Korean Air, and All Nippon Airways, have huge aircraft orders planned to be delivered during the forecast period. According to Boeing, there will be a demand for more than 244,000 new pilots in the Asia-Pacific region during the next two decades, with a demand for 126,000 pilots from China alone.

Accordingly, there have been significant developments concerning Civil Aviation Flight Training and Simulation in China. For instance, in April 2023, Boeing announced that they had brought its B737 MAX flight simulator to its Shanghai training center to fulfill the promise of improving pilot training for the aircraft in China after two fatal crashes in 2018 and 2019 led to it being grounded worldwide. Moreover, the United States plane maker has installed the B737 MAX Flight Training Device at its training hub at Shanghai Pudong International Airport to better support the operations of Chinese airlines. To increase the pilot training capacity in India, ALSIM was awarded a contract by the Airports Authority of India (AAI) in February 2021 to deliver three Flight Simulator Training Device (FSTD) simulators of EASA Flight Navigation and Procedure Trainer (FNPT) Multi Crew Coordination (MCC) level II types for single-aisle aircraft. All three FNPT II simulators are scheduled to enter service by 2022 at its training centers, namely, CATC Prayagraj, HTC Hyderabad, and NIATAM Gondia. Also, major countries in the region are accelerating their human space exploration programs. For instance, China is currently working to build its new space station, which is expected to be completed by 2022, and conducts deep-space human spaceflight by 2030. Such human space exploration plans are anticipated to propel the demand for space simulation and training solutions during the forecast period.

Civil Aerospace Simulation and Training Industry Overview

The civil aerospace training and simulation market is semi-consolidated. Some of the prominent players in the market for civil aerospace simulation and training are L3Harris Technologies Inc., The Boeing Company, CAE Inc., FlightSafety International, and Indra Sistemas S.A.

CAE Inc. has a majority share in commercial aviation simulators due to its global presence and brand image. In FY2021, the company delivered 36 full-flight simulators to its civil aviation customers, and in FY2022, the company delivered 30 FFS (a decrease of six simulators compared to the same period in FY2021).

Similarly, Lockheed Martin Corporation and The Boeing Company are some of the prominent companies that support NASA human space exploration programs. The increasing investments of the companies in developing new simulators with advanced features for training are anticipated to provide them with growth opportunities in the market in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Simulator Type

- 5.1.1 Full Flight Simulator (FFS)

- 5.1.2 Flight Training Devices (FTD)

- 5.1.3 Other Training Devices

- 5.2 Application

- 5.2.1 Commercial Aviation

- 5.2.2 Space

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Turkey

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 L3Harris Technologies, Inc.

- 6.2.2 CAE Inc.

- 6.2.3 The Boeing Company

- 6.2.4 FlightSafety International Inc.

- 6.2.5 Raytheon Technologies Corporation

- 6.2.6 Indra Sistemas S.A.

- 6.2.7 ALSIM EMEA

- 6.2.8 ELITE Simulation Solutions AG

- 6.2.9 Multi Pilot Simulations BV

- 6.2.10 Lockheed Martin Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in the field of Pilot Training

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日