|

市場調査レポート

商品コード

1849912

カロテノイド:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Carotenoids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| カロテノイド:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月10日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

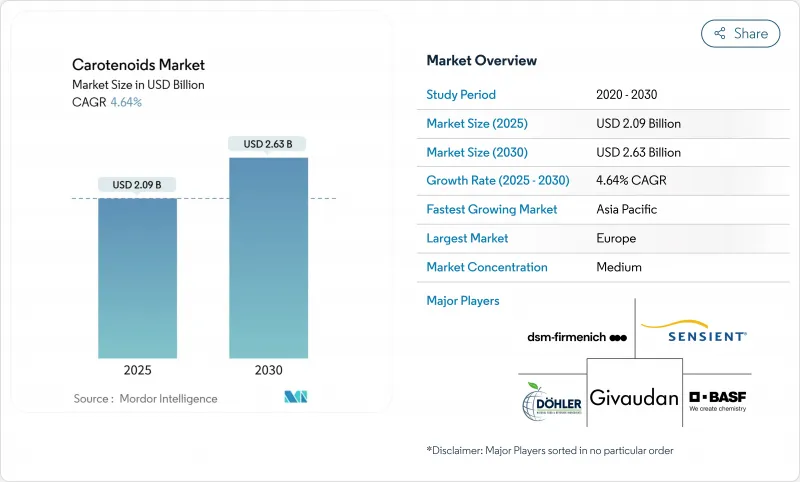

カロテノイド市場は、2025年に20億9,000万米ドル、2030年には26億3,000万米ドルに達すると予測され、予測期間中のCAGRは4.64%を記録します。

成分の透明性とクリーンラベル製品に対する消費者の需要が、カロテノイド業界を変革しています。メーカー各社は、こうした消費者の嗜好の変化に対応するため、天然成分を配合した製品の改良を進めています。業界は、持続可能で費用対効果の高いプロセスに重点を置きながら、抽出と生産方法の改善を通じて進歩を続けています。市場の成長は、飲食品、動物飼料、栄養補助食品、化粧品業界における用途の増加がさらに後押ししています。天然のカロテノイドは、その認識された健康上の利点と環境の持続可能性により、合成の代替品よりも注目を集めています。飲食品分野は、天然着色料や栄養添加物としてカロテノイドを使用するメーカーが目立つ用途分野の一つです。さらに、カロテノイドの抗酸化特性や、目の健康、免疫機能、皮膚の健康を促進する役割に対する意識の高まりが、栄養補助食品分野の需要を牽引しています。

世界のカロテノイド市場の動向と洞察

天然サプリメントとしてのベータカロチンの利用急増

予防医療への消費者シフトの高まりにより、βーカロチンのプロビタミンA特性や抗酸化作用に対する認識が広まり、βーカロチン・サプリメントの需要がかつてないほど高まっています。カナダ保健省(Health Canada)の2025年天然健康製品ガイドラインは、デュナリエラ・サリナ(Dunaliella salina)や合成由来を含む様々な供給源からのβーカロテンを、標準化された推奨摂取量とともに認めています。この規制の明確化により、サプリメントメーカーは北米全域で製品開発を拡大することができます。欧州食品安全機関(EFSA)と米国食品医薬品局(FDA)は、成分のトレーサビリティと安全用量の基準値に関する措置を実施しており、消費者の安全を優先しながら市場の成長を支えています。さらに、カロテノイドの十分な摂取と慢性疾患リスクの低減を関連付ける科学的証拠が増加していることも、この分野の利点となっているが、規制機関は特に喫煙者に対して、高用量のサプリメント摂取に関する注意を維持しています。この動向は、カロテノイド摂取量が推奨レベルを下回っている市場で特に顕著であり、ターゲットを絞った補助食品に大きな成長機会をもたらしています。

加工食品および飲料における天然着色料の需要増加

食品メーカーは、クリーン・ラベルの要件と認知可能な成分を求める消費者の需要に応えて、合成着色料から天然着色料へと移行しつつあります。この移行は、透明性と天然配合を目指す業界の幅広い動きを反映しています。欧州委員会が2024年4月にHaematococcus pluvialisの藻類から採取したアスタキサンチンを豊富に含むオレオレジンを承認したことは、食品用途における天然カロテノイドの規制当局の容認を示すものであり、食品カテゴリー全体で使用パラメータが定義されています。この承認により、メーカーは乳製品、菓子類、飲食品を含む様々な食品にこの天然着色料を取り入れることができます。植物性食肉メーカーは、従来の赤色色素が効果を発揮しない加熱加工時に色の安定性を維持するために、βーカロテンやリコピンなどの耐熱性カロテノイドを必要としています。これらのカロテノイドは、製品のライフサイクルを通して一貫した色調を提供しながら、押し出しや調理のような高温の加工方法にも耐えることができます。その他の特典として、カロテノイドは着色特性と栄養効果の両方を提供し、機能性食品の開発をサポートし、ひいては加工食品や飲食品における天然着色料の需要を促進します。

藻類・植物由来原料の価格変動

原材料コストの変動は、カロテノイド・メーカー、特に環境変動や季節的な入手可能性の影響を受けやすい藻類培養や植物抽出プロセスに依存しているメーカーにとって、根強い課題となっています。微細藻類の生産コストは、合成の代替品よりもかなり高いままであり、現在の見積もりでは、従来の植物性タンパク質と同等のコストを達成するには、規模の大幅な最適化と技術の進歩が必要であると示唆されています。ルテインの主な供給源であるマリーゴールドの栽培が気候変動によって中断されたことで、キサントフィル分野全体に価格変動をもたらす供給ボトルネックが発生しています。LED照明や制御された環境システムが生産コストの40%を占めることもあります。各社は垂直統合戦略や代替調達を通じて対応しているが、こうしたアプローチには多額の資本投資が必要であり、中小企業の市場参入を制限する可能性があります。

セグメント分析

アスタキサンチンは2024年に24.31%の市場シェアを占め、2025~2030年のCAGRは7.11%で成長予測をリードしています。シアノテック・コーポレーションは、ヘマトコッカス・プルビアリス(Haematococcus pluvialis)からの天然アスタキサンチン生産に注力しており、2024年度の純売上高2,310万米ドルの約65%を占めています。βーカロテンは、着色料とプロビタミンAの供給源としての二重機能性によって市場で大きな存在感を維持しており、ルテインとゼアキサンチンは、臨床研究に支えられた目の健康用途の拡大から利益を得ています。

新興の生産技術は、特に微生物発酵が従来の藻類培養よりも拡張性に優れていることから、製品タイプ別の競合ダイナミクスを再構築しています。リコピンの機能性食品への応用は、リコピンの摂取が心臓血管の健康に役立つという研究に支えられて拡大を続けており、カンタキサンチンは、色素沈着が要求される特殊な養殖市場でプレミアム価格を実現しています。このセグメントの成長軌道は、測定可能な健康上のメリットをもたらす、科学的に検証された天然成分に対する消費者のプレミアム支払い意欲の高まりを反映しています。

地域分析

2024年の市場シェアは欧州が34.19%を占め、天然成分を支持する規制と食品、飼料、製薬セクターからの安定した需要が牽引しています。同地域の消費者は天然成分に対する意識が高く、特に栄養補助食品と機能性食品において、健康効果が実証された製品に対して割高な価格設定を受け入れています。この地域の研究インフラと産学連携は、抽出技術とバイオアベイラビリティ手法を強化し、市場の需要をさらに押し上げています。

アジア太平洋地域は、養殖業の拡大、可処分所得の増加、天然成分への規制シフトに牽引され、2025~2030年のCAGRが5.55%と最も高い成長率を示します。この地域の養殖セクター、特にサケとエビの養殖では、製品の着色のためにアスタキサンチンとカンタキサンチンが必要です。一人当たりGDPが2020年の1,907米ドルから2023年には2,480.8米ドルに上昇することで明らかなように、インドでは中間所得層が増加しており、栄養補助食品の需要が高まっています。日本では、高齢化によってルテインとゼアキサンチンを含む目の健康と認知機能製品の消費が増加しています。この地域は、品質管理と規制基準の開発とともに、生産コストと原材料の入手が容易です。

北米は、確立された規制、情報通の消費者、高級天然カロテノイド製品を通じて市場の安定性を示しています。米国食品医薬品局(FDA)による複数の微細藻類種に対する一般に安全と認められる(GRAS)承認と明確な栄養補助食品ガイドラインは、新製品の発売を促進しています。メキシコでは、中間層の拡大と水産養殖部門が新たな市場機会を生み出しています。中東とアフリカでは、強化食品に対する需要の増加と政府の栄養プログラムが市場の成長を促進します。南米の国々、特にブラジルとチリは、豊富な天然資源と健康補助食品と輸出への関心の高まりにより、市場の拡大が見られます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 天然サプリメントとしてのベータカロチンの使用急増

- 加工食品・飲料における天然着色料の需要増加

- クリーンラベル製品における植物由来原料の採用増加

- ビーガン・ベジタリアン向けサプリメント製品の拡充

- 天然色素の動物性食品に対する消費者の嗜好がカロテノイドの使用を促進

- マイクロカプセル化と製剤安定性における技術の進歩

- 市場抑制要因

- 藻類や植物由来の原材料の価格変動

- 地域間の規制のばらつきが世界の導入を制限

- カロテノイドに関連する限られた保存期間

- 食品用途における色の一貫性維持の課題

- サプライチェーン分析

- 規制の見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- アスタキサンチン

- ベータカロテン

- カンタキサンチン

- ルテイン

- リコピン

- ゼアキサンチン

- その他のタイプ

- 形態別

- 粉

- 液体

- 用途別

- 食品・飲料

- 栄養補助食品

- 動物飼料

- パーソナルケアと化粧品

- 医薬品

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場ランキング分析

- 企業プロファイル

- BASF SE

- DSM-Firmenich AG

- Givaudan SA

- Divi's Laboratories Ltd

- Kemin Industries Inc.

- Sensient Technologies Corp.

- Dohler Group SE

- Solabia Group

- Allied Biotech Corp.

- EID-Parry(India)Ltd

- Cyanotech Corp.

- Lycored Ltd

- Guangzhou Leader Bio-Technology

- Fuji Chemical Industries

- Zhejiang NHU Co., Ltd

- Vidya Herbs Pvt Ltd

- Bio-gen Extracts Pvt Ltd

- DD Chemco

- Chenguang Biotech Group

- Archer Daniels Midland Company(ADM)