|

市場調査レポート

商品コード

1685805

アジア太平洋の医薬品受託製造機関- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Pharmaceutical Contract Manufacturing Organization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の医薬品受託製造機関- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

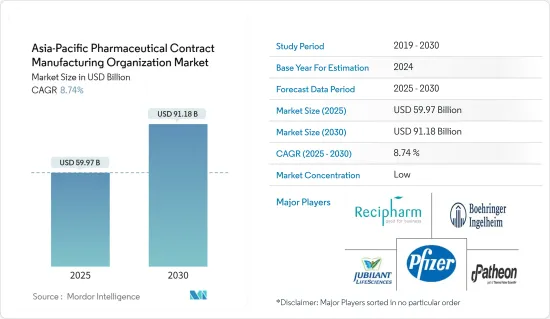

アジア太平洋の医薬品受託製造機関市場規模は、2025年に599億7,000万米ドルと推定され、予測期間中(2025年~2030年)のCAGRは8.74%で、2030年には911億8,000万米ドルに達すると予測されます。

中国は労働賃金が低い国であり、それだけで製薬会社の製造コストを30%も下げることができます。また、米国や欧州に比べて資本コストや諸経費が低く、税制優遇措置や通貨安も相まって、中国にアウトソーシングしている製薬企業にとってはコスト面で大きなメリットがあります。

主なハイライト

- 中国の医薬品CMO市場を牽引するもう1つの要因は、欧米で訓練を受けた熟練労働者です。欧米で訓練を受けた労働者の大半は就職のために中国に戻るが、これは厳格な移民政策と欧米の製薬労働者の失業が著しいためです。

- インドはまた、国内CMO市場の成長を利用し、日本の製薬業界がインドに拠点を構えることを奨励しています。この自動ルートによる100%直接投資は、国内製造に大きな弾みをつけるため、受託製造にも認められています。

- 日本のCMO市場はまだ未成熟です。しかし、日本では過去数年にわたり漸進的な成長が見られました。日本のCMO市場は、薬事法によって製販分離が認められた後、約30%の成長を遂げました。その後も成長傾向は続いています。日本では、武州製薬、ニプロファーマ、シミックのような大手CMOメーカーの数は少ないです。

- 薬価決定における政府の大規模な改革、構造変化、償還と価格決定における予測不可能性により、オーストラリアの多くの製薬会社は困難に直面しています。しかし、オーストラリアは南アジアの新興市場に近いため、医薬品輸出に関しては地理的に有利な立場にあります。

- 武漢はかつて重工業と鉄鋼で知られ、バイオ医薬品の製造拠点として急成長を遂げようとしていました。このようなアウトブレイクは医薬品供給の途絶につながる可能性があり、その場合、製造業者は米国食品医薬品局に通知することが義務付けられています。アウトブレイクが広まるにつれ、中国は原材料の主要供給国であるため、世界中の製薬工場にとって製造に必要な在庫を維持することが負担となります。

APAC医薬品受託製造市場動向

注射剤製剤が大きな市場シェアを占める

- 医薬品受託製造市場は、特にがん研究において注射薬の需要が増加していることから、拡大傾向にあると推定されます。がん治療薬やその他の高薬理活性薬(抗体結合体、ステロイド、速やかな作用発現を必要とする輸液など)の需要が堅調であることから、細胞毒性薬が注射剤製剤セグメントの主要な成長要因になると予想されます。

- 注射剤は、他の製剤と比較して高いリターンが期待できます。したがって、より高いROI、治療効率、迅速な作用発現が注射剤セグメントの成長を促進すると予想されます。

- がん治療用のパイプラインに有望な後期臨床化合物が多数あることから、堅調な成長率が期待されます。抗がん剤はパイプライン製品の50%近くを占める大きなシェアを占めています。

- 大手製薬会社が薬剤基質や製品の発見・開発に注力する一方で、生物学的製剤の大部分や充填・仕上げサービスはCMOに委託されています。その他の製剤製造では設備投資や運営コストは少ないが、利益率は無菌注射剤製剤の方が高いです。

インドは大きな市場シェアを占める

- 多国籍製薬企業の開発とインドにおけるプレゼンスの急速な拡大により、受託製造の概念は着実に進化し、製剤開発、医薬品の基礎製造、安定性試験、臨床試験の様々な段階などのサービスを包含するように急速に適応してきました。

- インドは、医療用医薬品や製品の基礎的な製造において、多くの国々に比べてはるかに優れた優位性を持っています。それは、豊富なマンパワー、知識豊富な労働力、WHO-GMPに承認された製造原則などの資源による。

- 医薬品合成のスケールアップと後期臨床試験は、この地域では収益性の高いプロトコルとなっています。それに伴い、DTAB(医薬品技術諮問委員会)は、欧米の規制市場であるインドにおける特定の医薬品の後期(フェーズIII)試験を免除することに合意しました。この優遇措置は、製薬会社にとって莫大なコスト削減につながり、インドへの注力を高めることになります。

- COVID-19の発生はインドの製薬セクターにも打撃を与えると予想されています。インドの医薬品メーカーは、医薬品原料や原薬の調達を中国に大きく依存しています。医薬品の製造に必要な主要原料の価格は、ウイルスの流行によって上昇しています。医薬品輸出促進協議会(Pharmexcil)のデータによると、主要原料のコストはすでに50~60%上昇しています。

- インドの医薬品規制当局がまとめた最新のデータでは、中国での封鎖が長期化した場合、重要な抗生物質、ビタミン剤、ホルモン剤やステロイド剤に必要な57種類の原薬が在庫切れとなる可能性があることが明らかになりました。これは、ひいては医薬品製造業界に大きな影響を与える可能性があります。

APAC医薬品受託製造業界の概要

アジア太平洋の医薬品製造受託機関市場は、非常に細分化された市場に向かっています。大手製薬会社は、製造コスト、運転資金、市場投入までの時間を削減するため、あるいは社内にない特定の専門知識を得るために、医薬品製造をCMOに委託するケースが増えています。このため、ベンダー間の競合が激化しています。ベンダーは市場シェアを拡大し、収益性を高めるために、地域を超えて拡大し、企業と戦略的・協力的なイニシアティブを形成しています。市場の最近の動向をいくつか紹介する:

- 2019年11月-Jubilant Biosys社は、機能的で統合的な創薬サービスの範囲に対する顧客需要の高まりにより、インドのグレーターノイダとベンガルールで2つの拡張プロジェクトの開始を発表しました。ジュビラント・バイオシスは、既存のグレーター・ノイダ・サイトにおいて、最新鋭のケミストリーサービス・ラボラトリーの設計と建設を開始しました。ケミストリーのFTE数は倍増し、2020年後半から稼働を開始する予定です。

- 2019年11月-ベーリンガーは、中国の生物製剤の商業生産拠点で能力拡張を計画しました。この拡張は、バイオリアクターの増設をカバーし、2.000Lのシングルユースバイオリアクター製造ライン2本のGMPオペレーションをサポートするために必要なすべてのユーティリティとインフラを含みます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 産業バリューチェーン分析

- 産業政策

- 市場促進要因

- 製薬企業によるアウトソーシング量の増加

- 市場抑制要因

- リードタイムと物流コストの増加

- 厳しい規制要件

- CMOの収益性に影響する生産能力活用の問題

- COVID-19の市場への影響評価

第5章 技術スナップショット

第6章 市場セグメンテーション

- サービスタイプ

- 原薬(API)製造

- 低分子

- 高分子

- 高活性API(HPAPI)

- 最終製剤(FDF)開発・製造

- 固形製剤

- 液体製剤

- 注射剤製剤

- 二次包装

- 原薬(API)製造

- 生産国

- 中国

- インド

- 日本

- オーストラリア

- その他のアジア太平洋

第7章 競合情勢

- 企業プロファイル

- Catalent Inc.

- Recipharm AB

- Jubilant Life Sciences Ltd

- Thermo Fisher Scientific Inc.(Patheon Inc.)

- Boehringer Ingelheim Group

- Pfizer CentreSource(Pfizer Inc)

- Aenova Group

- Famar SA

- Baxter Biopharma Solutions(Baxter International Inc)

- Lonza Group

第8章 投資分析

第9章 市場の将来

The Asia-Pacific Pharmaceutical Contract Manufacturing Organization Market size is estimated at USD 59.97 billion in 2025, and is expected to reach USD 91.18 billion by 2030, at a CAGR of 8.74% during the forecast period (2025-2030).

China is a country with low labor wages, which alone can lower the manufacturing costs of the pharmaceutical companies by as much as 30%. Along with it, low capital and overhead costs (compared to that of the United States and Europe), tax incentives, and undervalued currency combine to provide a significant cost advantage for pharmaceutical companies outsourcing to China.

Key Highlights

- Another factor driving the pharmaceutical CMO market in China is the country's Western-trained skilled workers. Majority of the workers who are trained in Western countries return to China to find work because of strict immigration policies an d significant unemployment among the European and American pharmaceutical workers.

- India is also taking advantage of the growth in the domestic CMO market, encouraging the Japanese pharmaceutical industries to setup their locations in the country, either wholly owned or in partnership with Indian companies.Additionally, India has until now allowed 100% FDI through the automatic route. This 100% FDI under the automatic route has been allowed in contract manufacturing to give a big boost to domestic manufacturing.

- The CMO market in Japan is still immature. However, the country witnessed incremental growth over the past few years. The Japanese CMO market witnessed a growth of about 30%, following the recognition to separate manufacturing and sales by the Pharmaceutical Affairs Act. The growth trend has been continuing ever since. The number of CMO manufacturers of significant size in Japan is low and includes players, like Bushu Pharmaceuticals, Nipro Pharma, and CMIC.

- With extensive governmental reforms in drug pricing, structural changes, and unpredictability in reimbursement and pricing decisions, many pharmaceutical companies in Australia are being challenged. However, the country is geographically well-placed in relation to pharmaceutical exports, owing to its proximity to the emerging markets of South Asia.

- The recent medical outbreak of COVID-19 has its epicenter in Wuhan, a Chinese city that was once known for its heavy industry and steel and was poised to become a burgeoning center for bio- pharmaceutical manufacturing. Such outbreaks may lead to the disruption of drug supply and manufacturers are required to notify the US Food and Drug Administration when that happens. As the outbreak becomes more widespread, it becomes a burden for pharmaceutical plants around the world to maintain the inventory required for manufacturing, as China is a major supplier of raw materials.

APAC Pharmaceutical Contract Manufacturing Market Trends

Injectable Dose Formulations Holds Significant Market Share

- The pharmaceutical contract manufacturing market is estimated to experience an upward trend, with the rise in demand for injectable drugs, especially in cancer research.Owing to the robust demand for oncology and other high-potency drugs (such as antibody conjugates, steroids, and IV fluids that require quick onset of action), cytotoxics are expected to be the key growth drivers for the injectable dose formulation segment.

- Injectable drugs provide higher returns, as compared to other drug formulation types. Therefore, higher ROI, therapeutic efficiency, and rapid onset of action are expected to drive the growth of the injectable formulation segment.

- Robust growth rates may be expected from the number of promising late-stage clinical compounds in the pipeline for cancer therapy. Anti-cancer drugs represent a significant share of nearly 50% of the pipeline products.

- The majority of the biologic drug product formulations as well as fill and finish services are being outsourced to CMOs, while the big pharmaceutical companies focus on the discovery and development of drug substrates and products. Although other dosage formulation manufacturing involves lesser capital investment and operating costs, the profit margins are higher for sterile injectable dose formulations.

India Occupies Significant Market Share

- With the advent of multinational pharmaceutical organizations and their rapidly growing presence in India, the concept of contract manufacturing has steadily evolved and quickly adapted to encompass services, such as formulation development, basic manufacturing of medicinal products, stability studies, and various stages of clinical trials.

- India has a far superior advantage, over many nations, in the basic manufacturing of medical drugs and products due to resources, such as large manpower, knowledgeable workforce, and WHO-GMP approved production principles.

- Scale-up of drug synthesis and late clinical trials have become a profitable protocol in this region. Along with it, DTAB (Drug Technical Advisory Board) has agreed to grant wavier to late stage (Phase III) studies of certain drugs in India, which are from the regulated markets of Europe and the United States. This incentive step translates into enormous cost savings for pharmaceutical companies, thereby increasing their focus on India.

- The COVID -19 outbreak is expected to hit India's pharmaceutical sector as well; in fact, it has already started. Indian drug manufacturers are dependent on China for sourcing their drug ingredients or active pharmaceutical ingredients (API) to a large extent. The prices of key ingredients for the manufacturing of drugs are rising on account of the virus outbreak. According to data available with the Pharmaceutical Export Promotion Council (Pharmexcil), the cost of key ingredients has gone up by 50- 60% already.

- Latest data compiled by India's drug regulatory authority revealed that 57 APIs required for crucial antibiotics, vitamins, and hormones or steroids may go out of stock, in case of a prolonged lockdown in China. This may, in turn, have a significant effect on the pharmaceutical manufacturing industry.

APAC Pharmaceutical Contract Manufacturing Industry Overview

The Asia Pacific pharmaceutical contract manufacturing organization market is moving towards highly fragmented market. The large pharmaceutical companies are increasingly outsourcing their production of drugs to CMOs, in order to reduce the cost of production, working capital requirement, and time to market, or to obtain a specific expertize not available in-house. This is increasing competition between vendors. Vendors are expanding across regions and are forming strategic and collaborative initiatives with companies to increase their market share and their profitability. Some of the recent developments in the market are:

- November 2019 - Jubilant Biosys announced commencement of two expansion projects in Greater Noida and Bengaluru India, owing to growing customer demand for its range of functional and integrated drug discovery services. It started design and construction of brand new and state-of-the-art chemistry services laboratories on the existing Jubilant Greater Noida site. The chemistry FTE capacity will be doubled, and operations are expected to commence from H2 2020.Thenewsitecanaccommodate upto500ChemistryFTE's.

- November 2019 - Boehringer planned a capacity expansion at its commercial manufacturing site for biologics in China. The expansion covers an addition al bioreactor an d includes all needed utility and infrastructure to support the GMP operations of 2x 2.000L single use bioreactor manufacturing lines.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Policies

- 4.5 Market Drivers

- 4.5.1 Increasing Outsourcing Volume by Pharmaceutical Companies

- 4.6 Market Restraints

- 4.6.1 Increasing Lead Time and Logistics Costs

- 4.6.2 Stringent Regulatory Requirements

- 4.6.3 Capacity Utilization Issues Affecting the Profitability of CMOs

- 4.7 Assessment of Impact of COVID-19 on the market

5 TECHNOLOGY SNAPSHOT

6 MARKET SEGMENTATION

- 6.1 Service Type

- 6.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

- 6.1.1.1 Small Molecule

- 6.1.1.2 Large Molecule

- 6.1.1.3 High Potency API (HPAPI)

- 6.1.2 Finished Dosage Formulation (FDF) Development and Manufacturing

- 6.1.2.1 Solid Dose Formulation

- 6.1.2.2 Liquid Dose Formulation

- 6.1.2.3 Injectable Dose Formulation

- 6.1.3 Secondary Packaging

- 6.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

- 6.2 Country

- 6.2.1 China

- 6.2.2 India

- 6.2.3 Japan

- 6.2.4 Australia

- 6.2.5 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Catalent Inc.

- 7.1.2 Recipharm AB

- 7.1.3 Jubilant Life Sciences Ltd

- 7.1.4 Thermo Fisher Scientific Inc. (Patheon Inc.)

- 7.1.5 Boehringer Ingelheim Group

- 7.1.6 Pfizer CentreSource (Pfizer Inc)

- 7.1.7 Aenova Group

- 7.1.8 Famar SA

- 7.1.9 Baxter Biopharma Solutions(Baxter International Inc)

- 7.1.10 Lonza Group