ナノ衛星・マイクロ衛星:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Nano and Microsatellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 193 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685775

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

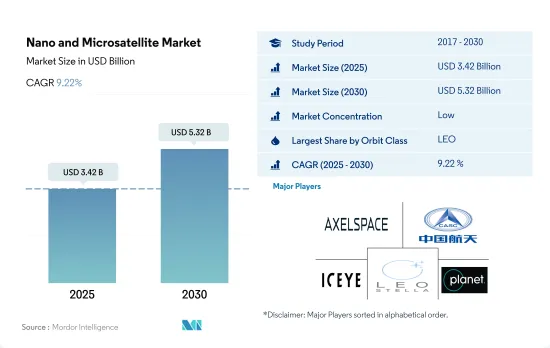

ナノ衛星・マイクロ衛星市場規模は2025年に34億2,000万米ドルと推定・予測され、2030年には53億2,000万米ドルに達し、予測期間中(2025年~2030年)のCAGRは9.22%で成長すると予測されています。

LEO衛星が市場の需要を牽引

- 打ち上げの際、衛星や宇宙船は通常、地球を周回する多くの特別な軌道の1つに配置されます。地球周回軌道には基本的に静止軌道(GEO)、中軌道、低軌道の3種類があります。多くの気象衛星や通信衛星は、地上から最も遠い地球高軌道をとる傾向があります。地球中周回軌道にある衛星には、特定の地域を監視するために設計された航法衛星や特殊衛星が含まれます。NASAの地球観測システムを含むほとんどの科学衛星は、地球低軌道にあります。

- ナノ衛星・マイクロ衛星市場は、通信、航法、地球観測、軍事偵察、科学ミッションに使用されるLEO衛星の需要拡大に牽引され、力強い成長を遂げています。2017年から2022年の間に、北米だけで約2,900機の小型LEO衛星が製造され、主に通信用途で打ち上げられました。このため、SpaceX、OneWeb、Amazonなどの主要企業は、LEOへの何千もの衛星の打ち上げを計画しています。

- 近年では、信号強度の向上、通信・データ転送能力の向上、カバーエリアの拡大などの利点から、MEO衛星やGEO衛星の軍事利用が拡大しています。例えば、レイセオン・テクノロジーズ社とボーイング社のミレニアム・スペース・システムズ社は、米国宇宙軍向けに極超音速ミサイルを探知・追跡するためのMissile Track Custody(MTC)MEO OPIRペイロードの最初のプロトタイプを開発しています。

アジア太平洋は著しい成長を遂げるだろう

- 世界のナノ衛星・マイクロ衛星市場は、さまざまな産業における高速インターネット、通信サービス、データ転送の需要増加を背景に、今後数年間で大きく成長すると予想されます。同市場は、市場シェアと収益創出という観点から、主要地域である北米、欧州、アジア太平洋に関して分析することができます。2017年~2022年の間に、800機以上のナノ衛星・マイクロ衛星が製造され、このセグメントの様々な事業者によって打ち上げられました。

- 北米は、Planet Labs社、Swarm Technologies社、SpaceX社など、同地域の有力な市場企業が複数いるため、世界のジオ衛星市場を独占すると予想されています。米国政府も先進衛星技術の開発に多額の投資を行っており、北米の市場開拓をさらに促進すると期待されています。2017年~2022年の間、この地域は製造されたナノ衛星・マイクロ衛星全体の61%を占めています。

- 欧州のナノ衛星・マイクロ衛星市場は、高速インターネットや通信サービスの需要増加により、大きな成長が見込まれています。欧州宇宙機関(ESA)は先進的な衛星技術の開発に多額の投資を行っており、同地域の市場成長をさらに促進すると期待されています。2017年~2022年の間、この地域は製造・打ち上げられた超小型衛星全体の5%を占めています。

- アジア太平洋は、中国、インド、日本などの国々で衛星ベースの通信サービスやナビゲーションシステムの需要が増加していることから、ナノ衛星・マイクロ衛星市場で大きな成長が見込まれています。

世界のナノ衛星・マイクロ衛星市場の動向

より良い燃料と運用効率へのニーズの高まりが市場成長を後押し

- 衛星製造業界は、軍事監視、通信、ナビゲーションから地球観測に至るまで、多くの用途における衛星の需要によって牽引されています。人工衛星の製造に必要とされる精巧さのレベルは非常に高いため、市場は米国、ロシア、中国、フランス、日本などの技術先進国で顕著です。

- ナノ衛星・マイクロ衛星の出現は、衛星製造市場に根本的な影響を及ぼしています。衛星メーカーは生産プロセスを強化する機会を探っています。人工衛星の積極的な納品スケジュールに対応するため、RUAGグループは2022年に、人工衛星の生産能力を増強するために他業界の技術を採用すると発表しました。ボーイング社もまた、衛星プログラムを強化するため、航空機製造業界で普及している技術の統合に注力しています。両社とも、年間生産量を増やすために衛星製造ラインに自動化を導入し、リードタイムを短縮するために特定の商用オフザシェルフ(COTS)コンポーネントのマルチソーシング戦略を採用しています。

- 衛星は質量によって分類されます。質量が10kgから100kgの衛星は超小型衛星とされ、1kgから10kgの衛星は超小型衛星とされます。2017年から2022年にかけて、世界全体で約1,200機の小型衛星が打ち上げられました。小型衛星は開発期間が短く、ミッション全体のコストを削減できるため、関心が高まっています。これらの衛星により、科学的・技術的成果を得るために必要な時間を大幅に短縮することが可能になりました。

さまざまな機関による宇宙開発費の増加は、超小型衛星のカテゴリーにプラスの影響を与えると予想されます。

- ナノ衛星・マイクロ衛星の出現は、衛星製造市場に強い影響を与えています。衛星メーカーは製造プロセスを改善する機会を模索しています。世界各国の政府は、科学研究、環境監視、国家安全保障など様々な目的で小型衛星技術に投資しています。衛星の製造に必要な複雑さのレベルは非常に高いため、米国、ロシア、中国、フランス、日本など、高度な技術を持つ国で市場が大きくなっています。

- 北米では、宇宙計画のための世界政府支出が2021年に約1,030億米ドルと過去最高を記録しました。この地域は、世界最大の宇宙機関であるNASAの存在により、宇宙イノベーションと研究の震源地となっています。2022年、米国政府は宇宙プログラムに約620億米ドルを費やし、世界で最も宇宙開発費を投じる国となりました。米国では、NASAのような連邦機関は毎年政府から資金援助を受けています。2023年、NASAは子会社に対して323億3,000万米ドルを受け取りました。

- 欧州では、英国宇宙庁が英国の宇宙産業を後押しする18のプロジェクトを支援するために650万ユーロを資金援助すると発表しました。この資金は、インパクトのある地元主導の計画や宇宙クラスター開発マネージャーを支援することで、英国の宇宙産業の成長を刺激します。18のプロジェクトは、公共サービスを強化するための地球観測(EO)データの活用など、地域の問題に立ち向かうためのさまざまな革新的宇宙技術を開拓することが期待されています。2022年11月、スペイン政府は、スペインの宇宙におけるリーダーシップを強化することを目的として、今後5年間で15億ユーロを欧州宇宙機関に割り当てると発表しました。

ナノ衛星・マイクロ衛星産業の概要

ナノ衛星・マイクロ衛星市場は断片化されており、上位5社で35.53%を占めています。この市場の主要企業は以下の通り。 Axelspace Corporation, China Aerospace Science and Technology Corporation(CASC), ICEYE Ltd., LeoStella and Planet Labs Inc..

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の質量

- 宇宙開発への支出

- 規制の枠組み

- 世界

- オーストラリア

- ブラジル

- カナダ

- 中国

- フランス

- ドイツ

- インド

- イラン

- 日本

- ニュージーランド

- ロシア

- シンガポール

- 韓国

- アラブ首長国連邦

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 用途

- 通信

- 地球観測

- ナビゲーション

- 宇宙観測

- その他

- 軌道クラス

- GEO

- LEO

- エンドユーザー

- 商業

- 軍事・政府

- その他

- 推進技術

- 電気式

- ガス

- 液体燃料

- 地域

- アジア太平洋

- 欧州

- 北米

- 世界のその他の地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Astrocast

- Axelspace Corporation

- Capella Space Corp.

- China Aerospace Science and Technology Corporation(CASC)

- German Orbital Systems

- GomSpaceApS

- ICEYE Ltd.

- LeoStella

- Planet Labs Inc.

- Satellogic

- SpaceQuest Ltd

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Nano and Microsatellite Market size is estimated at 3.42 billion USD in 2025, and is expected to reach 5.32 billion USD by 2030, growing at a CAGR of 9.22% during the forecast period (2025-2030).

LEO Satellites Are Leading Market Demand

- During launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. There are basically three types of Earth orbits, namely geostationary orbit (GEO), medium Earth orbit, and low Earth orbit. Many weather and communication satellites tend to have high Earth orbits, which are farthest from the surface. Satellites in medium Earth orbit include navigational and specialized satellites that are designed to monitor a specific area. Most science satellites, including NASA's Earth Observation System, are in low Earth orbit.

- The nano and microsatellite market is experiencing strong growth, driven by the growing demand for LEO satellites, which are used for communication, navigation, Earth observation, military reconnaissance, and scientific missions. Between 2017 and 2022, around 2,900 small LEO satellites were manufactured and launched from North America alone, primarily for communication applications. This has led companies such as SpaceX, OneWeb, and Amazon to plan the launch of thousands of satellites into LEO.

- In recent years, the military's use of MEO and GEO satellites has grown due to their advantages, including increased signal strength, improved communications and data transfer capabilities, and greater coverage area. For instance, Raytheon Technologies' and Boeing's Millennium Space Systems are developing the first prototype Missile Track Custody (MTC) MEO OPIR payloads to detect and track hypersonic missiles for the US Space Force.

Asia-Pacific will witness significant growth

- The global nano and microsatellite market is expected to grow significantly in the coming years, driven by increasing demand for high-speed internet, communication services, and data transfer across different industries. The market can be analyzed concerning North America, Europe, and Asia-Pacific, the major regions in terms of market share and revenue generation. During 2017-2022*, more than 800 nano and microsatellites were manufactured and launched by various operators in this segment.

- North America is expected to dominate the global geo satellite market due to several leading market players in the region, such as Planet Labs, Swarm Technologies, and SpaceX. The US government has also invested heavily in developing advanced satellite technology, which is expected to drive market growth in North America further. During 2017-2022*, the region accounted for 61% of the total nano and microsatellites manufactured.

- The nano and microsatellite market in Europe is expected to grow significantly due to the increasing demand for high-speed internet and communication services. The European Space Agency (ESA) has been investing heavily in developing advanced satellite technology, which is expected to further drive market growth in the region. During 2017-2022*, the region accounted for 5% of the total nano and microsatellites manufactured and launched.

- Asia-Pacific is expected to witness significant growth in the nano and microsatellite market due to the increasing demand for satellite-based communication services and navigation systems in countries such as China, India, and Japan.

Global Nano and Microsatellite Market Trends

Rising need for better fuel and operational efficiency boosting market growth

- The satellite manufacturing industry is driven by the demand for satellites in a plethora of applications, ranging from military surveillance, communications, and navigation to Earth observation. The level of sophistication required for manufacturing satellites is very high, and hence, the market is more prominent in technologically advanced nations, such as the United States, Russia, China, France, and Japan.

- The advent of small and nanosatellites has radically affected the satellite manufacturing market. Satellite manufacturers are exploring opportunities to enhance their production processes. In order to meet the aggressive delivery schedules for satellites, in 2022, RUAG Group announced that it was adopting technologies from other industries to augment its satellite production capacity. Boeing is also focusing on integrating technologies prevalent in the aircraft manufacturing industry to bolster its satellite programs. Both companies have integrated automation in their satellite production lines to boost their annual output and adopted a multi-sourcing strategy for certain commercial off-the-shelf (COTS) components to reduce lead time.

- Satellites are classified according to mass. Satellites with a mass between 10 kg and 100 kg are considered microsatellites, while satellites between 1 and 10 kg are considered nanosatellites. Around 1,200 small satellites were launched globally during 2017-2022. There is a growing interest in small satellites because of their shorter development time, which can reduce overall mission costs. These satellites have made it possible to significantly reduce the time required to obtain scientific and technological results.

Increasing space expenditure by different agencies are expected to positively impact the nano and microsatellites categories

- The advent of small and nanosatellites has strongly influenced the satellite manufacturing market. Satellite manufacturers are exploring opportunities to improve their manufacturing processes. Governments worldwide are investing in small satellite technology for various purposes, including scientific research, environmental monitoring, and national security. The level of complexity required to manufacture satellites is very high, and thus, the market is larger in countries with advanced technologies, such as the United States, Russia, China, France, and Japan.

- In North America, global government expenditure for space programs hit a record of approximately USD 103 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space in the world. In the United States, federal agencies such as NASA receive aid from the government every year, known as funding. In 2023, NASA received USD 32.33 billion for its subsidiaries.

- In Europe, the UK Space Agency announced that it would be funding EUR 6.5 million to support 18 projects to boost the UK space industry. The funding will stimulate growth in the UK space industry by supporting high-impact, locally-led schemes and space cluster development managers. The 18 projects are expected to pioneer a range of innovative space technologies to combat local issues, such as by utilizing Earth observation (EO) data to enhance public services. In November 2022, the Government of Spain announced that it would allocate EUR 1.5 billion to the European Space Agency over the next five years, aimed at reinforcing Spain's leadership in space.

Nano and Microsatellite Industry Overview

The Nano and Microsatellite Market is fragmented, with the top five companies occupying 35.53%. The major players in this market are Axelspace Corporation, China Aerospace Science and Technology Corporation (CASC), ICEYE Ltd., LeoStella and Planet Labs Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

- 4.3 Regulatory Framework

- 4.3.1 Global

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 France

- 4.3.7 Germany

- 4.3.8 India

- 4.3.9 Iran

- 4.3.10 Japan

- 4.3.11 New Zealand

- 4.3.12 Russia

- 4.3.13 Singapore

- 4.3.14 South Korea

- 4.3.15 United Arab Emirates

- 4.3.16 United Kingdom

- 4.3.17 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.3.3 Other

- 5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

- 5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Astrocast

- 6.4.2 Axelspace Corporation

- 6.4.3 Capella Space Corp.

- 6.4.4 China Aerospace Science and Technology Corporation (CASC)

- 6.4.5 German Orbital Systems

- 6.4.6 GomSpaceApS

- 6.4.7 ICEYE Ltd.

- 6.4.8 LeoStella

- 6.4.9 Planet Labs Inc.

- 6.4.10 Satellogic

- 6.4.11 SpaceQuest Ltd

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 193 Pages

- 納期

- 2~3営業日