|

市場調査レポート

商品コード

1685732

バイオベースポリウレタン:市場シェア分析、産業動向、成長予測(2025年~2030年)Bio-based Polyurethane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バイオベースポリウレタン:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

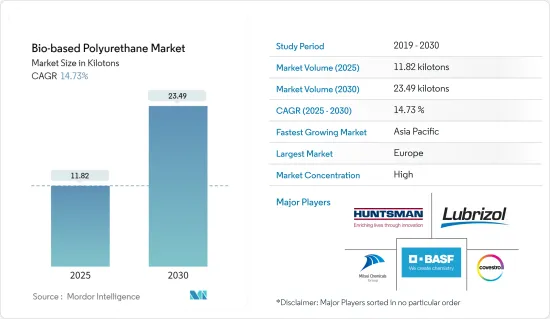

バイオベースポリウレタン市場規模は2025年に11.82キロトンと推定され、予測期間(2025年~2030年)のCAGRは14.73%で、2030年には23.49キロトンに達すると予測されます。

主なハイライト

- 市場はCOVID-19パンデミックの悪影響を受けました。パンデミックの間、建設業界は大きな影響を受け、調査対象市場の需要に影響を与えました。しかし、市場は今後数年間は成長軌道を維持すると予想されます。現在、市場はパンデミックから回復し、著しい成長率を示しています。

- 中期的には、新興国の建設業界からの需要の増加と、電子機器製造からの需要の増加が市場を牽引する主な要因です。

- しかし、バイオベースの材料はコストが高いため、市場成長の妨げになると予想されます。

- とはいえ、中東・アフリカの産業成長は、予測期間中に好機となることが予想されます。

- アジア太平洋は、中国やインドなどの国々からの消費が最も多く、世界中で最も急成長している市場になると予想されます。

バイオベースポリウレタン市場動向

輸送産業からの需要の増加

- バイオベースポリウレタンの主な用途は、自動車、鉄道、航空宇宙産業などの輸送産業です。さらに、自動車産業はバイオベースPUフォーム、コーティング、接着剤、シーラントを消費しています。具体的には、バイオベースPUフォームは座席システム(ヘッドレスト、ヘッドライナー、アームレスト、シートクッション、その他)や内装部品に使用されています。

- OCIA(Organisation Internationale des Constructeurs d'Automobiles)によると、2022年の世界の自動車生産台数は8,502万台に達しました。生産能力は2021年比で6%増加しました。2022年には、中国、米国、ドイツが自動車・商用車メーカーのトップ3となりました。

- 最大の自動車生産地域であるアジア太平洋も、2022年には7%の成長率を記録しました。生産台数はそれぞれ2021年の4,676万台から2022年には5,002万台に増加しました。同様に、アメリカとアフリカは2022年にそれぞれ10%と13%の成長率を示しました。

- 鉄道業界では、バイオベースPUは、今後数年間で従来のPU製品を大幅に置き換えることができるため、潜在的な用途があります。鉄道では、バイオベースフォームは座席のクッションや断熱用途に使用できます。

- インド鉄道は、単一経営で世界第3位の鉄道産業であったため、政府の創意工夫によって拡大すると予測されていました。インド・ブランド・エクイティ財団によると、2018年から2022年の間に、34のインフラ・サブセクターの1つである同国の鉄道に1,240億米ドル相当が投資されると予測されました。

- さらに、航空宇宙産業では、バイオベースのPUフォームとコーティングが従来のPU材料の代替となる可能性があります。ボーイング社によると、世界の航空宇宙サービス産業の規模は、2022年から2041年の間に3兆6,000億米ドルを超えると予想されており、米国とカナダがその約30%を占め、次いで欧州が23.5%を占めています。

- したがって、輸送産業における需要が、予測期間中にバイオベースポリウレタンの需要を増加させると予想されます。

アジア太平洋が急成長市場になる見込み

- アジア太平洋はバイオベースポリウレタンの最大の生産地です。

- バイオベースポリウレタンは建築に利用されています。窓やドアの形材、パイプや雨樋、セメント、床材、ガラス、シーリング材や接着剤、断熱材、建築パネル、屋根材への利用が増加しています。

- 中国は建設ブームに沸いています。同国は、この地域および世界最大の建築市場を有しており、世界の全建築投資の20%を占めています。中国政府は、2021年の3兆6,500億人民元(5,200億米ドル)から、2022年には3兆8,500億人民元(5,400億米ドル)の新規インフラ債券の年間限度額を設定すると推定しています。

- バイオPUは、バンパーやバンパースポイラー、ラテラルサイディング、ルーフ/ブーツスポイラー、ロッカーパネル、ボディパネル、ダッシュボードやダッシュボードキャリア、ドアポケットやパネル、コンソール、暖房換気空調、バッテリーカバー、エアダクト、圧力容器、スプラッシュシールドなどの自動車用途でポリプロピレンに取って代わることができます。

- OICA(Organisation Internationale des Constructeurs d'Automobiles)によると、中国では2021年に約2,612万台が生産されたのに対し、2022年には約2,702万台が生産され、約3%の成長率を記録しました。

- バイオベースのポリウレタンは、電気絶縁性、耐衝撃性、接着性などの品質に加えて、携帯電話、モバイル機器、コンピューター、テレビなどの電気・電子用途にも広く利用されています。

- 同様にインドでも、エレクトロニクス市場は需要の伸びを目の当たりにし、市場規模は急速な成長率で増加しています。電子情報技術省はインドにおける電子機器製造に関するビジョン文書の第2巻を発表し、インドの電子機器製造業は2020-21年の750億米ドルから2025-26年には3,000億米ドルに成長すると予測しました。インドと中国における電子機器・家電市場の成長は、アジア太平洋の市場成長をさらに押し上げる可能性があります。

- 前述の要因により、予測期間中にバイオベースポリウレタンの需要が増加する可能性が高いです。

バイオベースポリウレタン産業概要

バイオベースポリウレタン市場は統合型です。調査対象市場の主要メーカーは、BASF SE、Covestro AG、Huntsman International LLC、三井化学、The Lubrizol Corporationなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 新興諸国における建設産業からの需要増加。

- 電子機器製造業からの需要拡大

- その他の促進要因

- 抑制要因

- バイオベース材料のコスト高

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 用途

- フォーム

- コーティング剤

- 接着剤とシーラント

- その他の用途(ポリウレタン・バインダー、ポリウレタン・ディスパージョン)

- エンドユーザー産業

- 輸送

- 履物および繊維

- 建築

- 包装

- 家具・寝具

- エレクトロニクス

- その他のエンドユーザー産業(バイオメディカル、肥料産業)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他の欧州

- 世界のその他の地域

- ブラジル

- サウジアラビア

- 南アフリカ

- その他の国

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Arkema

- BASF SE

- Covestro AG

- Huntsman International LLC

- Miracll Chemicals Co. Ltd

- Mitsui Chemicals Inc.

- Stahl Holdings BV

- Toray Industries Inc.

- Teijin Limited

- The Lubrizol Corporation

- Woodbridge

第7章 市場機会と今後の動向

- 中東・アフリカにおける産業の成長

- バイオベース建材の開発

目次

Product Code: 46725

The Bio-based Polyurethane Market size is estimated at 11.82 kilotons in 2025, and is expected to reach 23.49 kilotons by 2030, at a CAGR of 14.73% during the forecast period (2025-2030).

Key Highlights

- The market was negatively affected by the COVID-19 pandemic. The construction industry was significantly impacted during the pandemic, which affected the demand in the market studied. However, the market is excepted to retain its growth trajectory in the coming years. Currently, the market has recovered from the pandemic and is growing at a significant rate.

- Over the mid-term, the key factors driving the market studied are the increasing demand from the construction industry in developing countries and the increasing demand from electronic appliance manufacturing.

- However, the high cost of bio-based materials is expected to hinder the growth of the market studied.

- Nevertheless, industrial growth in the Middle East and Africa is expected to act as an opportunity during the forecast period.

- The Asia-Pacific region is expected to be the fastest-growing market across the world, with the largest consumption from countries such as China and India.

Bio-based Polyurethane Market Trends

Increasing Demand from the Transportation Industry

- Bio-based polyurethane finds its key applications in the transportation industry, including the automotive, railway, and aerospace industries. Moreover, the automotive industry consumes bio-based PU foams, coatings, adhesives, and sealants. Specifically, bio-based PU foams are used in seating systems (headrests, headliners, armrests, seat cushioning, and others) and interior parts.

- According to Organisation Internationale des Constructeurs d'Automobiles (OCIA), global automotive production reached 85.02 million units in 2022. The production capacity increased by 6% compared to 2021. In 2022, China, the United States, and Germany were the top three manufacturers of cars and commercial vehicles.

- Asia-Pacific, the largest automotive production region, also witnessed a growth rate of 7% in 2022. The production increased from 46.76 million in 2021 to 50.02 million in 2022, respectively. Similarly, America and Africa witnessed 10% and 13% growth rates, respectively, in 2022.

- In the railway industry, bio-based PU has potential applications, as it can replace conventional PU products by a significant amount in the coming years. In railways, bio-based foams can be used in seat cushioning and thermal insulation applications.

- The Indian Railways were predicted to expand with government ingenuity since they were the third biggest railway industry in the world under a single management. According to the India Brand Equity Foundation, the equivalent of USD 124 billion was projected to be invested in the country's railroads between 2018 and 2022, one of 34 infrastructure sub-sectors.

- Furthermore, in the aerospace industry, bio-based PU foams and coatings can substitute conventional PU materials. According to Boeing, the size of the worldwide aerospace services industry is anticipated to exceed USD 3.6 trillion between 2022 and 2041, with the United States and Canada accounting for around 30% of that total, followed by Europe with 23.5 percent of the market.

- Therefore, the demand in the transportation industry is expected to increase the demand for bio-based polyurethane during the forecast period.

Asia-Pacific Region is Expected to be the Fastest Growing Market

- Asia-Pacific is the largest producer of bio-based polyurethane, with a high abundance of synthetic diisocyanates and a large number of bio-based polyurethane in the region.

- Bio-based polyurethane is utilized in construction. It is increasingly utilized for window and door profiles, pipes and guttering, cement, flooring, glass, sealants and adhesives, insulation, building panels, and roofing.

- China is amid a construction mega-boom. The country has the largest building market in the region and the world, making up 20% of all construction investments globally. The Chinese government is estimated to have an annual limit for new infrastructure bonds worth CNY 3.85 trillion (USD 0.54 trillion) in 2022, up from CNY 3.65 trillion (USD 0.52 trillion) in 2021.

- Bio-PU is capable of replacing polypropylene in automotive applications such as bumpers and bumper spoilers, lateral siding, roof/boot spoilers, rocker panels, body panels, dashboards and dashboard carriers, door pockets and panels, consoles, heating ventilation air conditioning, battery covers, air ducts, pressure vessels, and splash shields.

- According to Organisation Internationale des Constructeurs d'Automobiles (OICA), around 27.02 million vehicles were produced in China in 2022, compared to 26.12 million vehicles produced in 2021, witnessing a growth rate of about 3%.

- In addition to its electrical insulation, shock resistance, adhesion, and other qualities, bio-based polyurethane is also widely utilized in electrical and electronic applications such as cell phones, mobile devices, computers, and TVs.

- Similarly, in India, the electronics market witnessed a growth in demand, with market size increasing at a rapid growth rate. The Ministry of Electronics and Information Technology published the second volume of the Vision document on Electronics Manufacturing in India, which predicted that the electronics manufacturing industry in India would grow from USD 75 billion in 2020-21 to USD 300 billion by 2025-26. The growing electronics and appliances markets in India and China may push the market growth further in Asia-Pacific.

- The aforementioned factors are likely to increase the demand for bio-based polyurethane during the forecast period.

Bio-based Polyurethane Industry Overview

The bio-based polyurethane market is consolidated in nature. The major manufacturers in the market studied include BASF SE, Covestro AG, Huntsman International LLC, Mitsui Chemicals Inc., and The Lubrizol Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Construction Industry in Developing Countries

- 4.1.2 Growing Demand from Electronic Appliance Manufacturing.

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Bio-based Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Foams

- 5.1.2 Coatings

- 5.1.3 Adhesive and Sealants

- 5.1.4 Other Applications (Polyurethane Binders, Polyurethane Dispersions)

- 5.2 End-user Industry

- 5.2.1 Transportation

- 5.2.2 Footwear and Textile

- 5.2.3 Construction

- 5.2.4 Packaging

- 5.2.5 Furniture and Bedding

- 5.2.6 Electronics

- 5.2.7 Other End-user Industries (Biomedical, Fertilizer Industry)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 Saudi Arabia

- 5.3.4.3 South Africa

- 5.3.4.4 Rest of the Countries

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 BASF SE

- 6.4.3 Covestro AG

- 6.4.4 Huntsman International LLC

- 6.4.5 Miracll Chemicals Co. Ltd

- 6.4.6 Mitsui Chemicals Inc.

- 6.4.7 Stahl Holdings BV

- 6.4.8 Toray Industries Inc.

- 6.4.9 Teijin Limited

- 6.4.10 The Lubrizol Corporation

- 6.4.11 Woodbridge

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Industrial Growth in Middle-East and Africa

- 7.2 Developments in Bio-based Building Materials