|

|

市場調査レポート

商品コード

1938978

サイバーセキュリティ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サイバーセキュリティ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

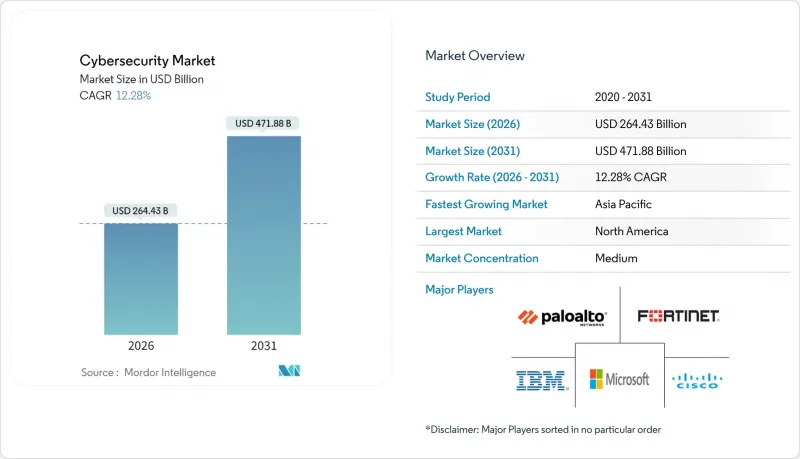

2026年のサイバーセキュリティ市場規模は2,644億3,000万米ドルと推定され、2025年の2,355億米ドルから成長が見込まれます。

2031年の予測では4,718億8,000万米ドルに達し、2026年から2031年にかけてCAGR12.28%で拡大する見通しです。

この拡大の主な要因は、ゼロトラストアーキテクチャへの支出増加、ITと運用技術(OT)の防御統合、量子耐性暗号化への準備です。北米は支出面で主導権を維持する一方、アジア太平洋地域では企業がワークロードをクラウドファースト環境に移行するにつれ、最も急速な伸びを示しています。また、サイバー保険引受会社が検証可能な管理策を要求する中、予算配分も増加しており、監視を簡素化する統合セキュリティプラットフォームへの移行を組織に促しています。同時に、ベンダー各社が新たな脅威ベクトルへの対応を競う中、合併・買収によるプラットフォーム統合の動きも活発化しています。

世界のサイバーセキュリティ市場の動向と洞察

加速するクラウドファーストのデジタルトランスフォーメーション

クラウド移行は、分散環境において境界制御が機能しなくなるため、セキュリティ投資の優先順位を再構築しています。クラウド導入は拡大を続け、オンプレミス環境の割り当てを上回り、アイデンティティ、ワークロード、データ保護機能を統合するクラウドネイティブアプリケーション保護プラットフォームの需要を牽引しています。企業はツールの乱立を削減する統合コンソールを求めており、ベンダーはハイブリッド環境全体でテレメトリを相関させるプラットフォームを提供することで、可視性と対応効率の向上に応えています。

重要インフラにおけるIT-OTセキュリティの融合

インダストリー4.0の進展により、従来エアギャップで保護されていたシステムがオンライン化され、レガシー制御ネットワークがIT資産を標的とする同じ攻撃者に晒されるようになりました。これによりサイバーセキュリティ市場での需要が高まっています。ISA/IEC 62443などの規制枠組みは、生産現場からデータセンターまでをカバーする統合防御を義務付けており、専門的なOT脅威検知・セグメンテーションツールへの投資を促進しています。国家レベルの攻撃主体が電力網の脆弱性を探る中、エネルギー事業者が導入を主導しており、OT特化型セキュリティ施策のリスク低減効果は、同等のITプロジェクトを上回る投資対効果をもたらしています。

サイバーセキュリティ人材不足と賃金上昇

クラウド、OT、AI駆動型防御といった希少スキルに対する給与上昇に伴い、340万人の専門家不足が予算を圧迫しています。この制約は、運用に必要な専門要員が少ないプラットフォームへの市場統合を促進すると同時に、マネージドセキュリティサービスやAI搭載自動化ツールを提供するベンダーに機会を生み出しています。この状況は高い離職率によってさらに悪化しており、サイバーセキュリティ専門家の64%が業務負荷のストレスを理由に転職を検討しています。これにより、組織のセキュリティ予算に影響を与える採用と研修コストの継続的なサイクルが生じています。

地域別分析

北米は成熟した規制環境と主要ベンダーの存在を背景に、2025年のサイバーセキュリティ市場収益の43.20%を占めました。大統領令14028号による広範なゼロトラスト移行の義務化を受け、同地域の支出は2027年までに1,376億米ドルを超える見込みです。米国では2023年に9,036件のサイバーインシデントが発生し、欧州の2,557件を大きく上回りました。これにより高度な脅威インテリジェンスフィードやマネージドSOCサービスへの需要が持続しています。カナダとメキシコは、越境的な侵害報告とインシデント対応を調和させる官民共同プログラムを通じて成長に貢献しています。

アジア太平洋地域は16.85%のCAGRで最も急速に成長しており、国家主導のデジタル国家計画によりセキュリティが重要インフラの地位に格上げされています。中国、インド、日本、韓国は国家サイバー戦略に複数年予算を割り当てており、オーストラリアとニュージーランドはインシデント開示を義務付ける包括的なレジリエンス枠組みを実施しています。地域の購入者は、当初からクラウドネイティブセキュリティを採用することで従来の制御を飛び越えることが多く、アイデンティティ中心およびAI駆動型分析の導入を加速させています。

欧州地域の成長は、GDPRの施行と、より多くのセクターへの適用範囲拡大を定めるNIS2指令の施行が推進しています。ドイツ、英国、フランスが支出を牽引する一方、中東欧市場はEU要件への適合に伴い、小規模な基盤から成長しています。フランスとスペインにおけるソブリンクラウド構想は、国内でホストされるセキュリティスタックの需要を刺激し、国境を越えたデータ転送制限は、プライバシー強化型暗号化技術の採用を加速させています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 市場定義と調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- クラウドファーストによるデジタル変革の加速

- 重要インフラにおけるIT-OTセキュリティの融合

- ハイブリッドワークフォースにおけるゼロトラストアーキテクチャの要件

- サイバー保険引受要件の急増

- デジタル主権規制が推進する地域特化型セキュリティスタック

- 量子耐性暗号化移行のタイムライン

- 市場抑制要因

- サイバーセキュリティ人材不足と賃金上昇

- レガシーインフラとの統合の複雑性

- APIの拡散による攻撃対象領域の複雑化

- SOCアラート疲労と誤検知過多によるROIの制限

- バリューチェーン分析

- 重要規制枠組みの評価

- 主要利害関係者への影響評価

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主要な使用事例と事例研究

- 価格設定および価格モデルの分析

- サイバーセキュリティ研修の動向

- マクロ経済的要因の影響

第5章 市場規模と成長予測

- 提供別

- ソリューション

- アプリケーションセキュリティ

- クラウドセキュリティ

- データセキュリティ

- アイデンティティおよびアクセス管理

- インフラ保護

- 統合リスク管理

- ネットワークセキュリティ

- エンドポイントセキュリティ

- サービス

- プロフェッショナルサービス

- マネージドサービス

- ソリューション

- 展開モード別

- クラウド

- オンプレミス

- エンドユーザー業界別

- BFSI

- ヘルスケア

- ITおよび通信

- 産業および防衛

- 小売業および電子商取引

- エネルギー・公益事業

- 製造業

- その他

- エンドユーザー別企業規模

- 大企業

- 中小企業(SMEs)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリアおよびニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- IBM Corporation

- Microsoft Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- CrowdStrike Holdings, Inc.

- Trend Micro Incorporated

- Zscaler, Inc.

- Okta, Inc.

- Gen Digital Inc.(formerly NortonLifeLock Inc.)

- Sophos Limited

- Proofpoint, Inc.

- McAfee LLC

- Darktrace plc

- Rapid7, Inc.

- SentinelOne, Inc.

- Imperva, Inc.

- Qualys, Inc.

- Trellix Holdings LLC

- Splunk Inc.

- Elastic N.V.

- Akamai Technologies, Inc.

- Broadcom Inc.(Symantec Enterprise Division)

- VMware, Inc.

- Cybereason

- Ivanti, Inc.

- Tenable Holdings, Inc.

- CyberArk Software Ltd.

第7章 市場機会と将来の動向

- 空白領域と未充足ニーズの評価