|

|

市場調査レポート

商品コード

1937436

スペインのソーラーエネルギー:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Spain Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペインのソーラーエネルギー:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

概要

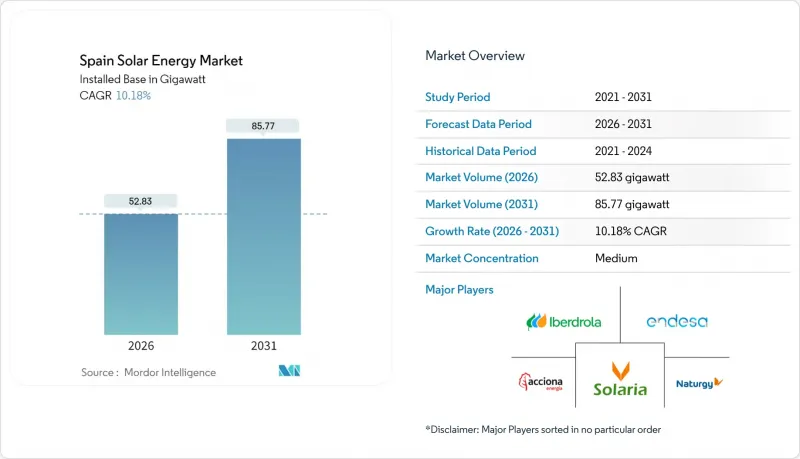

スペインのソーラーエネルギー市場は、2025年に47.95ギガワットと評価され、2026年の52.83ギガワットから2031年までに85.77ギガワットに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは10.18%と見込まれます。

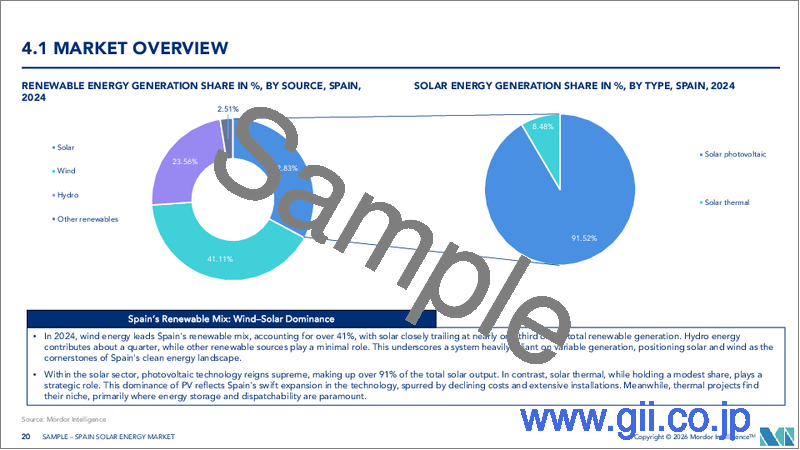

急速な容量拡大により、ソーラーエネルギーは既に国内発電量の21%を占め、欧州連合(EU)平均を大きく上回っています。これにより、改訂された国家エネルギー・気候計画に基づく76ギガワットのソーラーエネルギー目標達成に向けた明確な軌道に乗っています。モジュール価格の下落、EUの「Fit for 55」指令に沿った許可手続きの迅速化、そして企業による電力購入契約(PPA)への強い需要が、スペインのソーラーエネルギー市場全体の成長を後押ししています。特に日射量の多い地域では、出力抑制や価格競争による収益減少への対策として、ソーラーエネルギーと蓄電を組み合わせたハイブリッド構成が台頭しています。トタルエナジーズによるセビリア・クラスター(263MW)やプレニチュードのレノプール・プロジェクト(330MW)が示すように、国際的な開発業者の参入が加速する一方、送電網の混雑やナチュラ2000による土地利用制限が短期的な導入規模を抑制しています。

スペインのソーラーエネルギー市場の動向と分析

大規模太陽光モジュールのコスト低下

世界の供給過剰によりモジュール価格は下落を続けており、カスティーリャ・ラ・マンチャ州やエストレマドゥーラ州では、低品質な土地であっても競争力のある均等化発電原価(LCOE)を達成可能となりました。両面受光パネルと単軸トラッカーの組み合わせにより、現在では25%を超える設備利用率を達成可能となり、大規模地上設置型発電所の経済的余地が拡大しています。トタルエナジーズなどの国際的な電力会社は、2023年比で最大15%の設備投資(Capex)削減効果を挙げています。コストパリティの達成により、解放された資本をシステム周辺機器のアップグレードやエネルギー管理ソフトウェアに再配分できるため、蓄電池とのハイブリッド化が促進されています。現地のエンジニアリング企業からは、ケーブル損失と労働投入を削減する1,500VDCシステム設計への顕著な移行が報告されています。結果として、従来は経済的に不利な立場にあった地域においても、スペインのソーラーエネルギー市場パイプラインが拡大しています。

EU「Fit for 55」及び「REPowerEU」対応期限

2030年脱炭素化の法的拘束力のある目標は、開発業者に規制面の確実性を提供し、入札参加と資金調達可能性を加速させます。スペインは2024年に22,326MWのソーラーエネルギー建設を認可し、2025年第1四半期にはさらに3,019MWを承認しました。規制の整合性は蓄電分野にも及び、家庭用蓄電池も容量収益の対象となり、分散型資産のキャッシュフローが改善されました。地方自治体も国の方針に呼応し、アンダルシア州政府は2025年に1.4GWのプロジェクトについて送電網接続を迅速化しました。明確な政策スケジュールにより市場価格リスクが最小化され、スペイン太陽光市場への外国直接投資が促進されています。

土地利用とナチュラ2000保護区域との競合

保護区域はスペイン国土の約30%を占め、5ヘクタールを超えるプロジェクトには完全な環境影響調査が義務付けられています。ムルシア州だけで2030年までに3万ヘクタールのソーラーエネルギーを計画していますが、その60%が農協組織による組織的な反対に直面する旧耕作地に位置しています。開発業者は廃鉱山などのブラウンフィールド用地をますます対象としており、1MWあたり5万~10万ユーロの修復費用が追加されます。紛争の少ない土地への集中は、送電網の脆弱性により既に制約を受けている地域へ容量を集中させ、その結果、出力抑制リスクを増幅させています。

セグメント分析

2025年時点でソーラーエネルギーはスペインの太陽エネルギー市場の94.45%を占め、2031年までCAGR10.45%で拡大しています。一方、CSP(集光型太陽熱発電)のPNIEC目標は4.8GWに下方修正されました。リチウムイオン電池は2024年に140米ドル/kWhを下回るコストとなり、溶融塩システム比半額で2~4時間の蓄電を可能とするため、開発業者は太陽光+蓄電池ハイブリッドを優先します。これによりスペインのソーラーエネルギー市場規模は、2025年から2030年にかけて31GW以上増加する見込みです。

CSP(集光型太陽熱発電)は依然として20~50ユーロ/MWhで工業プロセス熱を供給可能であり、変動の激しい天然ガス価格よりも安価です。スペインには2.3GWの稼働プラントが存在します。しかしながら、2024年には新規のユーティリティ規模CSPプロジェクトでファイナンスクローズに至った事例はありませんでした。電力会社が資本をn型セルを用いた両面受光型ソーラーエネルギー(発電量10~15%向上)へ再配分する中、CSPのシェアはさらに縮小する見込みです。

ソーラーエネルギー市場レポートは、技術別(ソーラーエネルギーと集光型太陽熱発電)、系統接続タイプ別(系統連系型と独立型)、エンドユーザー別(大規模、商業・産業、住宅)に分類されています。市場規模と予測は、設置容量(GW)単位で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ユーティリティ規模の太陽光モジュールのコスト低下

- EU「Fit for 55」および「REPowerEU」の遵守期限

- IBEX-35企業における企業間電力購入契約(PPA)の急増

- 系統連系型蓄電池ハイブリッドシステムによるプロジェクトIRRの向上

- 干ばつ被害地域(アンダルシア、カスティーリャ・ラ・マンチャ)における農業用ソーラーエネルギー(Agri-PV)の優遇措置

- 自家消費協同組合(autoconsumo colectivo)の急増

- AI最適化による発電計画の改善がマーチャント収益の獲得を促進

- 市場抑制要因

- 土地利用とナチュラ2000保護区域との競合

- 高日照地域におけるインバーター飽和による出力抑制リスク

- 前日プールにおける不安定なカニバリゼーション割引

- 2軸トラッカーの自治体許可取得に要する長期化

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 業界間の競争

- PESTEL分析

第5章 市場規模と成長予測

- 技術別

- ソーラーエネルギー(PV)

- 集光型太陽熱発電(CSP)

- グリッドタイプ別

- オングリッド

- オフグリッド

- エンドユーザー別

- ユーティリティ規模

- 商業・産業(C&I)

- 住宅

- コンポーネント別(定性的分析)

- 太陽光モジュール/パネル

- インバーター(ストリング型、中央型、マイクロ型)

- 架台および追尾システム

- システム周辺機器および電気機器

- エネルギー貯蔵およびハイブリッド統合

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、提携、電力購入契約)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- Iberdrola SA

- Acciona Energia

- Endesa(Enel Group)

- Solaria Energia y Medio Ambiente SA

- Repsol SA

- Engie Espana

- Naturgy Renovables

- Gransolar Group

- Soltec Power Holdings

- Cobra IS(ACS Group)

- RIC Energy

- Forestalia Renovables

- Prodiel

- Powertis(SPIC)

- Q-Energy

- X-Elio

- Opdenergy

- TotalEnergies Renewables Espana

- Sonnedix

- Fit Energy