シアン化水素-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Hydrogen Cyanide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685673

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

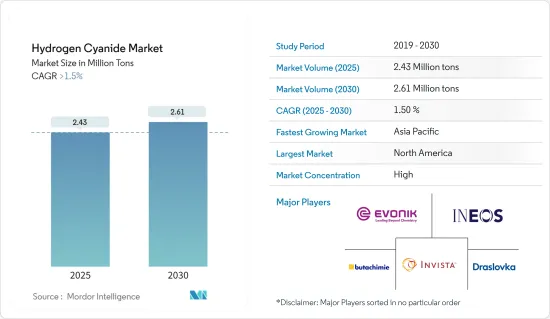

シアン化水素の市場規模は2025年に243万トンと推定され、予測期間(2025年~2030年)のCAGRは1.5%を超え、2030年には261万トンに達すると予測されます。

製造されるシアン化水素の大部分はアジポニトリル製造の原料として使用され、繊維やプラスチック製造用のナイロン66の製造に使用されます。アジポニトリル(AND)はヘキサメチレンジアミン(HMDA)の製造に使用され、その大部分(約92%)はナイロン6,6繊維や樹脂の製造に使用されます。

中期的には、シアン化ナトリウムとシアン化カリウムの需要の高さと、アジポニトリルの製造におけるシアン化水素の使用の増加が、市場成長を促進する主な要因でした。

反面、シアン化水素は毒性が強いため、市場成長の妨げとなっています。

未開拓の市場におけるキレート剤の生産におけるシアン化水素の使用は、将来的に機会をもたらす可能性が高いです。

北米は世界のシアン化水素市場を独占すると予想され、アジア太平洋地域は予測期間中に最も急成長する市場になると予想されます。

シアン化水素市場の動向

シアン化ナトリウムとカリウムの用途が最も急成長するセグメントへ

- シアン化ナトリウムとシアン化カリウムの前駆体であるシアン化水素は、電気メッキや銀・金などの金属採掘に一般的に使用されます。

- 湿式法では、シアン化ナトリウム(NaCN)またはシアン化水素を水酸化ナトリウムで中和して製造します。シアン化水素は気体または液体の形で添加され、NaOHは水溶液として添加され、NaCN水溶液を形成します。さらに、NaCN水溶液の蒸発中に固体のNaCN結晶が形成されることもあります。

- シアン化カリウム(KCN)は、シアン化水素を水酸化カリウム水溶液で治療し、その溶液を真空蒸発させることで生成します。

- シアン化ナトリウムとシアン化カリウムの両方は、金抽出、電気めっき、化学製造など、さまざまな工業プロセスで使用される重要な化学物質です。

- シアン化ナトリウムとシアン化カリウムは、低品位の鉱石から金と銀を抽出する際に主に使用されます。

- シアン化カリウムとシアン化ナトリウムは、ニトリルやカルボン酸の製造にも広く使われています。

- 米国地質調査所によると、2022年の世界金生産量は3,100トンに達しました。中国が世界の金鉱山生産をリードし、2022年の推定生産量は330トン、次いでオーストラリアが同年に約320トンを生産します。

- 推定金埋蔵量が最も多い国は、オーストラリア、ロシア、南アフリカです。さらに、カナダの鉱業は世界最大のカリ生産国であり、金の生産国トップ5に入っています。カナダで最も新しい金鉱山であるオンタリオ州のピュアゴールド・レッドレイク鉱山プロジェクトは、2021年8月に商業運転を開始し、年間87.8コースの金を追加すると推定されました。

- ロシアのウクライナ侵攻に続き、化学業界は2022年、エネルギーと原材料コストの上昇、パンデミック、経済の不確実性、政治的混乱によってすでに緊張状態にある世界・サプライ・チェーンにさらなるボトルネックが発生する1年を経験しました。

- BASFが発表した報告書2022によると、2023年の世界の化学品生産量(医薬品を除く)は、2022年から前年比2.0%増、前年比2.2%増が見込まれています。

- 世界最大の化学市場である中国では、2023年には化学生産の伸びがやや鈍化すると予想されています。同国の化学生産は2022年に5.9%増加しました。中国経済の開放は、特に消費財と健康・栄養分野での中国内需の成長を後押しし、業界のプラス成長に寄与すると予想されます。

- これらすべての要因を考慮すると、市場全体は予測期間中にプラス成長を示すと予想されます。

市場を独占する北米

- ITC貿易地図によると、米国は2022年に約87トンのシアン化水素を輸出する最大の輸出国です。

- 現在、シアン製品禁止に関する国全体の大きな規制はないです。しかし、モンタナ州、コロラド州、ウィスコンシン州などでは、国内での特定のシアン化物使用を防止するいくつかの規制があります。

- この地域におけるシアン化水素の需要は、ナイロンやポリアミドの生産に使用されるアジポニトリルの生産、塗料やコーティング剤に使用されるアクリル・プラスチック用のアセトンシアノヒドリンの生産、金回収用のシアン化ナトリウムやシアン化カリウムの生産、農薬やその他の農業製品用の塩化シアヌルなどの用途によって牽引されています。

- 同国は世界有数の金と銀の産出国です。米国地質調査所によると、2022年、同国は世界第5位の金生産国で、総生産量は約170トンでした。

- シルバー・インスティテュートによると、2022年の米国の銀生産量は世界第9位で、4,110万オンス(~1,165.17トン)と、2021年の生産量を6%上回りました。

- 上記の用途とともに、シアン化水素を使用して製造される塩化シアヌルは農薬やその他の農産物の製造にも使用されるため、同国で調査された市場の需要は同国の農業産業によっても牽引されています。

- プラスチック産業によるアセトンシアノヒドリンの需要は、さらに市場の消費に拍車をかけています。

- プラスチック産業の成長は現在、大量のプラスチック廃棄物による環境汚染の増加に影響を受けています。カナダ政府によると、同国では年間約150億枚のレジ袋と約5,700万本のプラスチックストローが使用されています。

- シアン化水素を主成分とする化学薬品、すなわちシアン化ナトリウムやシアン化カリウムは、金や銀の採掘プロセスで重要な用途を見出しています。

- USGSによると、同国は中国、オーストラリア、ロシアに次ぐ第4位の金生産国で、2022年の金生産量は約220トン。

- また、銀の主要生産国トップ15にも入っています。シルバー・インスティテュートによると、政府の銀生産量は約870万オンス(246.64トン)で、2021年と比較すると約5%減少しています。

- 農業による殺虫剤などの需要も、同国のシアン化水素の大量消費に貢献しています。

- 農業はカナダ経済に大きく貢献しています。カナダ農業食糧省(AAFC)によると、2022年、カナダは世界第5位の農産物輸出国になりました。

- こうした動向はすべて、予測期間中の市場需要に影響を与えそうです。

シアン化水素業界の概要

世界のシアン化水素市場は部分的に統合されています。主要企業には(順不同)インビスタ、エボニック・インダストリーズ、INEOS、Butachimie Chalampe、Drasslok、旭化成などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- シアン化ナトリウムとシアン化カリウムの製造に対する有利な需要

- アジポニトリル製造におけるシアン化水素の使用量の増加

- 抑制要因

- シアン化水素の高い毒性

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 構造タイプ

- シアン化水素液体

- シアン化水素ガス

- 用途

- シアン化ナトリウムおよびシアン化カリウム

- アジポニトリル

- アセトンシアノヒドリン

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ロシア

- トルコ

- 北欧諸国

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Air Liquide

- Asahi Kasei Corporation

- Ascend Performance Materials

- Butachimie

- Draslovka

- Evonik Industries AG

- Hindusthan Chemicals Company

- INEOS

- INVISTA

- Kuraray Co. Ltd

- Matheson Tri-Gas Inc.

- Sumitomo Chemical Co. Ltd

- Taekwang Industrial Co. Ltd

第7章 市場機会と今後の動向

目次

The Hydrogen Cyanide Market size is estimated at 2.43 million tons in 2025, and is expected to reach 2.61 million tons by 2030, at a CAGR of greater than 1.5% during the forecast period (2025-2030).

The majority of the hydrogen cyanide manufactured is used as a raw material for adiponitrile production, which is used in producing nylon 66 for fiber and plastic production. Adiponitrile (AND) is used to make hexamethylene diamine (HMDA), the majority of which (approximately 92%) is used to make nylon 6,6 fibers and resins.

Over the medium term, the major factors driving market growth were the high demand for sodium and potassium cyanide and the increasing use of hydrogen cyanide in producing adiponitrile.

On the flip side, the highly toxic nature of hydrogen cyanide hampers the market's growth studied.

Its use in the production of chelating agents in untapped markets is likely to present opportunities in the future.

North America is expected to dominate the global hydrogen cyanide market, while the Asia-Pacific region is expected to be the fastest-growing market during the forecast period.

Hydrogen Cyanide Market Trends

Sodium and Potassium Cyanide Application to be the Fastest Growing Segment

- Hydrogen cyanide, as a precursor of sodium cyanide and potassium cyanide, is commonly used for electroplating and mining of metals such as silver and gold.

- The wet process produces sodium cyanide (NaCN) or the neutralization of hydrogen cyanide with sodium hydroxide. The HCN is added both in the form of a gas or liquid, and NaOH is added as an aqueous solution to form an aqueous NaCN solution. Furthermore, solid NaCN crystals can be formed during evaporation of the aqueous NaCN solution.

- Potassium cyanide (KCN) is formed by the treatment of hydrogen cyanide with an aqueous potassium hydroxide solution, followed by the vacuum evaporation of the solution.

- Both sodium cyanide and potassium cyanide are important chemicals used in various industrial processes, including gold extraction, electroplating, and chemical manufacturing.

- Sodium cyanide and potassium cyanide are majorly used in the extraction of gold and silver from low-grade ores.

- Potassium cyanide and sodium cyanide are also widely used for the production of nitriles and carboxylic acids.

- According to the US Geological Survey, in 2022, global gold production reached 3,100 metric tons. China led global gold mine production, with an estimated 330 metric tons produced in 2022, followed by Australia, producing about 320 metric tons in the same year.

- The countries with the largest estimated gold reserves are Australia, Russia, and South Africa. Furthermore, Canada's mining industry is the world's biggest producer of potash and is in the top five producers of gold. The Pure Gold Red Lake Mine project in Ontario, Canada's newest gold mine, began commercial operations in August 2021 and was estimated to add 87.8 koz of gold yearly.

- Following Russia's invasion of Ukraine, the chemical industry experienced a year marked by further bottlenecks in global supply chains already strained by rising energy and raw material costs, a pandemic, economic uncertainty, and political turmoil in 2022.

- According to a report published by BASF 2022, global chemical production (excluding pharmaceuticals) is expected to increase by 2.0% in 2023, with a Y-o-Y increase of 2.2% from 2022.

- In China, the world's largest chemicals market, a slight slowdown in chemical production growth is expected in 2023. The country's chemical production grew by 5.9% in 2022. The opening up of the Chinese economy is expected to boost domestic demand growth in China, especially in the consumer goods and health and nutrition sectors, and contribute to positive growth in the industry.

- With the consideration of all these factors, the overall market is expected to witness positive growth during the forecast period.

North America to Dominate the Market

- According to the ITC trade map, the United States was the largest exporter of hydrogen cyanide in the year 2022, exporting about 87 tons of hydrogen cyanide in 2022.

- Currently, there are no major country-wide regulations regarding the cyanide product ban. However, states such as Montana, Colorado, and Wisconsin have some restrictions preventing specific cyanide usage in the country.

- The demand for hydrogen cyanide in the region is driven by applications such as the production of adiponitrile, which is used for nylon and polyamides production; the production of acetone cyanohydrin for acrylic plastics, which is further used in paints and coatings; for production of sodium cyanide and potassium cyanide for gold recovery, and cyanuric chloride for pesticides and other agriculture products.

- The country is among the world's major producers of gold and silver. According to the US Geological Survey, in 2022, the country was the 5th largest producer of gold globally, with a total production of about 170 metric tons.

- According to the Silver Institute, the United States was the world's ninth-largest producer of silver in 2022, producing 41.1 million ounces (~1,165.17 metric tons) of silver, which is 6% more than the production in 2021.

- Along with the abovementioned applications, the demand for the market studied in the country is also driven by the agricultural industry in the country, as cyanuric chloride produced using hydrogen cyanide is also used for the production of pesticides and other agricultural products.

- Plastic industries' demand for acetone cyanohydrin further adds to the market's consumption.

- The plastic industry's growth is currently affected by increasing environmental pollution due to the huge amount of plastic waste. According to the Canadian government, about 15 billion plastic bags and about 57 million plastic straws are used annually in the country.

- Hydrogen cyanide-based chemicals, i.e., sodium cyanide and potassium cyanide, find significant applications in the mining process of gold and silver.

- According to USGS, the country is 4th largest producer of gold after China, Australia, and Russia, with gold production of about 220 tons in the year 2022.

- The country is also among the top 15 major silver-producing nations in the world. According to the Silver Institute, the government has produced about 8.7 million ounces of silver (246.64 metric tons ), a decline of about 5% compared to 2021.

- The agriculture industry's demand for pesticides and other products also contributes to the country's significant consumption of hydrogen cyanide.

- The agriculture industry is a significant contributor to the Canadian economy. Agriculture and Agri-Food Canada (AAFC) said that in 2022, Canada was the world's fifth largest agricultural exporter.

- All such trends are likely to impact the market demand over the forecast period.

Hydrogen Cyanide Industry Overview

The global hydrogen cyanide market is partially consolidated. The major companies include (not in a particular order) INVISTA, Evonik Industries, INEOS, Butachimie Chalampe, Drasslok, and Asahi Kasei Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Favorable Demand for Manufacturing of Sodium Cyanide and Potassium Cyanide

- 4.1.2 Increasing Usage of Hydrogen Cyanide for the Production of Adiponitrile

- 4.2 Restraints

- 4.2.1 Highly Toxic Nature of Hydrogen Cyanide

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Structure Type

- 5.1.1 Hydrogen Cyanide Liquid

- 5.1.2 Hydrogen Cyanide Gas

- 5.2 Application

- 5.2.1 Sodium Cyanide and Potassium Cyanide

- 5.2.2 Adiponitrile

- 5.2.3 Acetone Cyanohydrin

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Malaysia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%)** /Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Asahi Kasei Corporation

- 6.4.3 Ascend Performance Materials

- 6.4.4 Butachimie

- 6.4.5 Draslovka

- 6.4.6 Evonik Industries AG

- 6.4.7 Hindusthan Chemicals Company

- 6.4.8 INEOS

- 6.4.9 INVISTA

- 6.4.10 Kuraray Co. Ltd

- 6.4.11 Matheson Tri-Gas Inc.

- 6.4.12 Sumitomo Chemical Co. Ltd

- 6.4.13 Taekwang Industrial Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日