航空宇宙・防衛MLCC-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Aerospace and Defence MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 234 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684037

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

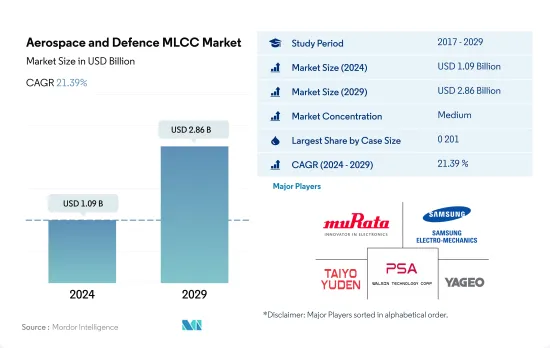

航空宇宙・防衛MLCC市場規模は、2024年に10億9,000万米ドルと推定され、2029年には28億6,000万米ドルに達すると予測され、予測期間(2024年~2029年)のCAGRは21.39%で成長します。

最適化されたアビオニックMLCCの選択が航空宇宙・防衛システムを強化

- 航空宇宙・防衛産業は、AI、IoT、5G通信を含む高度なアビオニクス技術の採用が進む中で、急速な変貌を遂げています。このような動向は、航空機の最先端電子システムをサポートするために、より高い静電容量、より低いESR、および信頼性の向上を備えたMLCCの必要性を後押ししています。ケースサイズ0 201および0 402のMLCCは、アビオニクスの小型・軽量の電子回路に人気があります。小型のフォームファクターと高い静電容量により、UAVやその他の小型航空機に搭載される飛行制御システム、ナビゲーションシステム、通信機器などの小型化デバイスに最適です。航空電子機器の小型化・軽量化の動向は、ケースサイズ0 201および0 402 MLCCの需要を牽引しています。

- ケースサイズ0 603および1 005のMLCCは、小型化と静電容量のバランスが取れており、さまざまな航空電子機器用途で汎用性の高い部品となっています。これらは一般的に、コックピット・ディスプレイ、センサー・システム、および有人・無人航空機の配電ネットワークで使用されています。最新の航空機では高度なアビオニクス・システムの採用が増加しており、ケースサイズ0 603および1 005 MLCCの需要が高まっています。

- ケースサイズ1 210のMLCCは、より高い静電容量値を提供し、航空電子機器の電力管理、エネルギー貯蔵、およびフィルタリング用途に適しています。これらの大型MLCCは、レーダーシステム、衛星通信、高度アビオニクス制御ユニットなどの重要なアビオニクス・システムで一般的に利用されています。より強力で洗練されたアビオニクス技術へのニーズの高まりが、ケースサイズ1 210およびその他のMLCCの需要に寄与しています。UAVやMAVの需要は伸びており、MLCCは安定した効率的な電子部品の動作を保証する重要な役割を担っています。

防衛費の増加と地政学的ダイナミクスの中で航空宇宙・防衛MLCC市場は世界的に成長

- 航空宇宙・防衛MLCC市場は世界的に堅調な成長を遂げています。中国とインドが牽引するアジア太平洋地域では、2022年に3億6,203万米ドルの売上を記録し、2028年には10億6,000万米ドルに急増すると予測され、2023年から2028年までのCAGRは20.37%と堅調な伸びを示しました。2023~24年度の予算が59.4億インドルピーに上るインドは、MLCCが特に無人航空機(UAV)の防衛能力を向上させる上で極めて重要な役割を担っていることを強調しています。

- 欧州は、防衛費の顕著な増加を示し、2020年から2021年にかけての3%増を反映して、2021年までに1億1,605万米ドルに達しました。2022年にロシアとウクライナの紛争が発生する中、欧州は防衛力を強化し、その結果、防衛費は14%増の3,450億米ドルに急増しました。MLCCはこのような状況下で重要な役割を果たし、軍用機や防衛システムにおける信号の完全性を確保し、2028年までに3億3,116万米ドルというこの分野の想定収益目標に貢献しています。

- 北米は世界の軍事費の支配的勢力として防衛に多額の投資を行っており、2022年の累積支出は9,120億米ドルに達します。特に米国の航空宇宙・防衛部門は3,910億米ドルの経済貢献をしており、MLCCは軍用機や電子戦防衛システムの確実な運用に極めて重要な役割を果たしています。

- 中東・アフリカ、南米を含む世界のその他の地域は、地政学的課題、テロの脅威、国防支出の増加に取り組んでいます。これらの地域全体で、航空宇宙・防衛MLCC市場は経済力学、地政学的影響、防衛の優先事項の収束を反映しており、MLCCは航空宇宙・防衛システムの信頼性と効率を確保する重要な部品として浮上しています。

世界の航空宇宙・防衛MLCC市場動向

監視ソリューション改善への需要の高まりが市場を後押し

- MLCCの需要は、航空宇宙・防衛(A&D)分野、特に軍用機やUAVのような電子戦防衛システムなどの用途で高まっています。これらの産業では、特定の機能を持つ部品を利用する信頼性の高いパワーエレクトロニクスシステムが必要とされます。MLCCは、高い信頼性、高品質ファクターによる最適性能、効果的なEMI抑制、ノイズ低減、ライン・フィルタリング、エネルギー蓄積機能、高周波ノイズのデカップリング、電圧レギュレーション機能を提供するため、これらの要求を満たす上で極めて重要です。MLCCは、UAVやその他の航空宇宙および防衛パワーエレクトロニクスシステムの信頼性の高い動作を保証する上で非常に重要です。

- UAVの生産台数は、2021年の384万7,000台から2022年には444万8,000台へと14%の大幅増を記録しました。この成長により、特にUAV向け、特に高電圧電源アプリケーション向けのMLCC需要が大幅に増加しています。MLCCはUAVにおいて、電源バイパスコンデンサ、DC-DCコンバータの入出力フィルタ、平滑コンデンサ、デジタル回路やLCDモジュールの必須部品として重要な役割を果たしています。A&D企業は、特定の要件を満たし、システムの性能を向上させるMLCCの価値と重要性をますます認識するようになっています。

- 小型化や機能強化など、MLCCの進歩は需要を増大させています。その結果、より高性能な自動操縦システムの開発や、機能を損なうことなくMLCCをコンパクトに統合することで容易になったリアルタイムUAVアプリケーションの拡大につながっています。高信頼性や高速応答時間といったMLCCの機能向上が、リアルタイムUAVアプリケーションの採用に拍車をかけています。

地政学的緊張の高まりと老朽化した軍用機を置き換えるための近代化計画が軍事支出を促進しています。

- MLCCは防衛用電子機器に不可欠な部品であり、重要なエネルギー貯蔵と信号フィルタリング機能を提供します。MLCCの需要は防衛費の変動に直接影響され、特にミサイルシステムや防衛通信機器などの分野では、支出の増加が需要の増加を促進します。しかし、COVID-19パンデミック時の国防支出の減少は、業界が医療技術に重点を移したため、MLCC市場にマイナスの影響を与えました。防衛費の安定化に伴い、防衛用電子機器におけるMLCCの需要は回復すると予想されます。

- COVID-19パンデミックは、世界の優先順位が医療技術と実験用試験装置にシフトしたため、防衛エレクトロニクスに重大な影響を与えました。このため、高信頼性の防衛用電子機器に対する需要が減少し、高電圧防衛市場を安定させる努力が必要となりました。パンデミックは多くの防衛垂直プラットフォームにも悪影響を及ぼし、予期せぬ混乱に直面した場合の適応性と回復力の重要性を浮き彫りにしました。

- 2012年から2016年にかけては、政府による緊縮財政の結果、防衛市場は停滞しました。しかし、2017年から2019年にかけては顕著な好転が起こり、航空機や宇宙エレクトロニクスといった特定の狭い最終市場分野で著しい成長が見られました。しかし、2020年にはパンデミックがこの成長軌道を乱し、防衛エレクトロニクス需要が11%減少しました。米国の主導権が交代したことで、2022年までの国防支出は抑制されました。それでも2023年には、ミサイルとミサイル防衛システムに焦点を当てた、小規模で精密な欧州の防衛エレクトロニクス市場に新たなビジネスチャンスがもたらされると予想されました。

航空宇宙・防衛MLCC産業の概要

航空宇宙・防衛MLCC市場は適度に統合されており、上位5社で44.17%を占めています。この市場の主要企業は以下の通り。 Murata Manufacturing, Samsung Electro-Mechanics, Taiyo Yuden, Walsin Technology Corporation and Yageo Corporation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 無人航空機の生産

- 世界の無人航空機生産台数

- 軍事支出

- 世界の軍事支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両タイプ

- 有人航空機

- 無人航空機

- ケースサイズ

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- その他

- 電圧

- 600V~1100V

- 600V未満

- 1100V以上

- 静電容量

- 10μF~100μF

- 10μF未満

- 100μF以上

- 誘電タイプ

- クラス1

- クラス2

- 地域

- アジア太平洋

- 欧州

- 北米

- 世界のその他の地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Yageo Corporation

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Aerospace and Defence MLCC Market size is estimated at 1.09 billion USD in 2024, and is expected to reach 2.86 billion USD by 2029, growing at a CAGR of 21.39% during the forecast period (2024-2029).

Optimized avionic MLCC selection enhances aerospace and defense systems

- The aerospace and defense industries are witnessing a rapid transformation with the increasing adoption of advanced avionics technologies, including AI, IoT, and 5G communications. These trends drive the need for MLCCs with higher capacitance, lower ESR, and improved reliability to support cutting-edge electronic systems in aircraft. Case sizes 0 201 and 0 402 MLCCs are popular for compact and lightweight electronic circuits in avionics. Their small form factor and high capacitance make them ideal for miniaturized devices, such as flight control systems, navigation systems, and communication equipment in UAVs and other small aircraft. The trend toward miniaturization and weight reduction in avionics drives the demand for case sizes 0 201 and 0 402 MLCCs.

- Case sizes 0 603 and 1 005 MLCCs balance compactness and capacitance, making them versatile components in various avionic applications. They are commonly used in cockpit displays, sensor systems, and power distribution networks in manned and unmanned aerial vehicles. The increasing adoption of advanced avionics systems in modern aircraft enhances the demand for case sizes 0 603 and 1 005 MLCCs.

- Case size 1 210 MLCCs offer higher capacitance values and are well-suited for power management, energy storage, and filtering applications in avionics. These larger-sized MLCCs are commonly utilized in critical avionic systems like radar systems, satellite communications, and advanced avionics control units. The evolving need for more powerful and sophisticated avionic technologies contributes to the demand for case sizes 1 210 and other MLCCs. The demand for UAVs and MAVs is growing, and MLCCs play a vital role in ensuring stable and efficient electronic components for successful operation.

The global aerospace and defense MLCC market thrives amid rising defense expenditures and geopolitical dynamics

- The aerospace and defense MLCC market experiences robust growth globally. In Asia-Pacific, led by China and India, the segment generated USD 362.03 million in 2022, with a projected surge to USD 1.06 billion by 2028, showcasing a robust CAGR of 20.37% from 2023 to 2028. India, with a substantial INR 5.94 lakh crore budget for FY 2023-24, emphasizes MLCCs' pivotal role in advancing defense capabilities, particularly in unmanned aerial vehicles (UAVs).

- Europe witnessed a noteworthy uptick in defense spending, reaching USD 116.05 million by 2021, reflecting a 3% increase from 2020 to 2021. Amid the Russia-Ukraine conflict in 2022, Europe reinforced its defense capabilities, resulting in a 14% surge in defense expenditures to USD 345 billion. MLCCs play a vital role in this context, ensuring signal integrity in military aircraft and defense systems and contributing to the sector's envisioned revenue target of USD 331.16 million by 2028.

- North America, as the dominant force in global military expenditures, invests significantly in defense, with a cumulative expenditure of USD 912 billion in 2022. The aerospace and defense sector, particularly in the United States, contributes USD 391 billion to the economy, with MLCCs playing a pivotal role in ensuring the reliable operation of military aircraft and electronic warfare defense systems.

- The Rest of the World, encompassing the Middle East, Africa, and South America, grapples with geopolitical challenges, terrorism threats, and increased defense spending. Across these regions, the aerospace and defense MLCC market reflects a convergence of economic dynamics, geopolitical influences, and defense priorities, with MLCCs emerging as critical components ensuring the reliability and efficiency of aerospace and defense systems.

Global Aerospace and Defence MLCC Market Trends

Growing demand for improved surveillance solutions is propelling the market

- The demand for MLCCs is rising in the aerospace and defense (A&D) sectors, especially in applications such as military aircraft and electronic warfare defense systems like UAVs. These industries require reliable power electronic systems that utilize components with specific functionalities. MLCCs are crucial in meeting these demands as they offer high reliability, optimal performance with a high-quality factor, effective EMI suppression, noise reduction, line filtering, energy storage capabilities, decoupling of high-frequency noise, and voltage regulation capabilities. MLCCs are critical in ensuring the dependable operation of UAVs and other aerospace and defense power electronic systems.

- The production of UAVs experienced a significant 14% increase from 3.847 million in 2021 to 4.448 million in 2022. This growth has led to a substantial rise in the demand for MLCCs, particularly for UAVs, specifically for high-voltage power supply applications. MLCCs play critical roles in UAVs as power supply bypass capacitors, input/output filters in DC-DC converters, smoothing capacitors, and essential components in digital circuits and LCD modules. A&D companies are increasingly recognizing the value and significance of MLCCs in meeting their specific requirements and enhancing the performance of their systems.

- Advancements in MLCCs, including smaller sizes and enhanced capabilities, have increased demand. This has led to the development of more capable autopilot systems and the expansion of real-time UAV applications facilitated by the compact integration of MLCCs without compromising functionality. Improved capabilities of MLCCs, such as high reliability and fast response times, have fueled the adoption of real-time UAV applications.

Growing geopolitical tensions and the modernization plans to replace aging military aircraft are propelling military spending

- MLCCs are vital components in defense electronics, providing crucial energy storage and signal filtering capabilities. The demand for MLCCs is directly influenced by fluctuations in defense spending, with increased spending driving higher demand, particularly in areas such as missile systems and defense communication equipment. However, the decline in defense spending during the COVID-19 pandemic negatively affected the MLCC market as the industry shifted focus to medical technology. As defense spending stabilizes, the demand for MLCCs in defense electronics is expected to rebound.

- The COVID-19 pandemic had significant implications for defense electronics as global priorities shifted toward medical technology and laboratory test equipment. This led to a decline in demand for high-reliability defense electronics, requiring efforts to stabilize the high-voltage defense markets. The pandemic also adversely affected many defense vertical platforms, highlighting the importance of adaptability and resilience in the face of unexpected disruptions.

- Between 2012 and 2016, government-imposed sequestering resulted in a stagnant defense market. However, a notable turnaround occurred from 2017 to 2019, with remarkable growth in specific narrow end-market areas such as aircraft and space electronics. However, the pandemic disrupted this growth trajectory in 2020, causing an 11% decline in defense electronics demand. The shift in the US leadership restrained defense spending through 2022. Nonetheless, 2023 was expected to bring new opportunities in the small and precise European markets for defense electronics, focused on missiles and missile defense systems.

Aerospace and Defence MLCC Industry Overview

The Aerospace and Defence MLCC Market is moderately consolidated, with the top five companies occupying 44.17%. The major players in this market are Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd, Walsin Technology Corporation and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Aerial Vehicle Production

- 4.1.1 Global Unmanned Aerial Vehicles Production

- 4.2 Military Spending

- 4.2.1 Global Military Spending

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Manned Aerial Vehicle

- 5.1.2 Unmanned Aerial Vehicle

- 5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

- 5.3 Voltage

- 5.3.1 600V to 1100V

- 5.3.2 Less than 600V

- 5.3.3 More than 1100V

- 5.4 Capacitance

- 5.4.1 10 μF to 100 μF

- 5.4.2 Less than 10 μF

- 5.4.3 More than 100 μF

- 5.5 Dielectric Type

- 5.5.1 Class 1

- 5.5.2 Class 2

- 5.6 Region

- 5.6.1 Asia-Pacific

- 5.6.2 Europe

- 5.6.3 North America

- 5.6.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 234 Pages

- 納期

- 2~3営業日