|

市場調査レポート

商品コード

1684021

中東のチョコレート:市場シェア分析、産業動向、成長予測(2025年~2030年)Middle East Chocolate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東のチョコレート:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 193 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

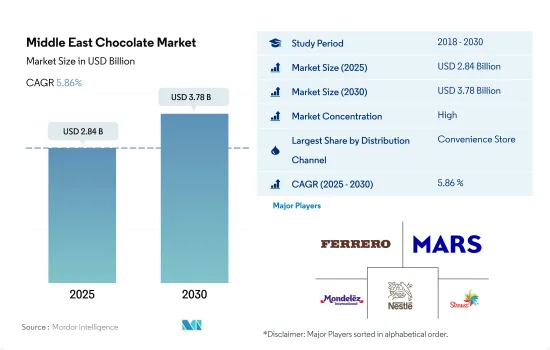

中東のチョコレート市場規模は2025年に28億4,000万米ドルと推計され、2030年には37億8,000万米ドルに達し、市場推計・予測期間(2025年~2030年)のCAGRは5.86%で成長すると予測されます。

ショッピング施設の増加やブランドの入手可能性により、コンビニエンスストアやスーパーマーケット/ハイパーマーケットがこの地域のチョコレート販売に優位性を発揮

- 中東では、全体的な小売セグメントが2022年と比較して2023年には金額ベースで5.28%の成長率を維持しています。予測される拡大は、同市場における消費者のコンビニエンス・ショッピング施設に対する嗜好の高まりによるものです。小売セグメントでは、コンビニエンスストアが2023年の数量ベースで最大の小売単位です。中東で人気のあるコンビニエンスストアには、Spinneys、LuLu Express、7-Eleven、Zoom、Fresh Plus、Circle Kなどがあります。2028年までに、中東のコンビニエンスストア・セグメントは数量ベースで6.37%の成長を記録すると推定されます。

- スーパーマーケットとハイパーマーケットは中東の菓子類市場で2番目に大きなチャネルです。このチャネルは2023年の中東のチョコレート菓子類販売における流通チャネル全体のセグメントにおいて、2022年と比較して金額ベースで4.77%の成長を示しました。スーパーマーケットやハイパーマーケットのような近代的な小売チャネルの開発により、消費者は高品質のチョコレート製品を購入することが可能になりました。これらのチャネルは各国において近接しているため、市場で入手可能な多種多様な製品の中から消費者の購入決定に影響を与えるという利点があります。

- オンライン・チャネルは最も急速に成長している流通チャネルであり、2023年から2030年までのCAGRは6.43%です。消費者は、迅速で便利な配達オプションを提供するオンライン・チャネルを好みます。同地域のインターネット普及率の高さも、こうしたチャネルの需要を後押ししています。この地域のすべての国の中で、アラブ首長国連邦とサウジアラビアのインターネット普及率が最も高く、2023年7月現在で99%です。

サウジアラビアとUAEがリードするチョコレートの大幅な生産と消費で、2023年の金額シェアはほぼ70%。

- 中東のチョコレート市場は、2023年に金額ベースで2022年比5.28%の成長を記録しました。シングルオリジンチョコレート、オーガニックチョコレート、ハンドメイドチョコレート、職人チョコレートなどの高品質チョコレート製品に対する消費者の需要が、この地域のチョコレート市場を牽引する大きな要因となっています。サウジアラビアとUAEがこの地域の主要市場として特定され、2023年の同地域のチョコレート販売全体における金額シェアは合計で63.38%を占めました。主な促進要因は、生産量の多さ、高級チョコレートに対する消費者の嗜好の高まり、チョコレートの製造と取引を促進するための適切な業界規制です。

- サウジアラビアはGCC諸国で最大のチョコレート生産国であり、ミルクチョコレートやダークチョコレート製品を含む同国のチョコレート消費の高さに支えられています。2023年現在、サウジアラビアには1,000以上のチョコレート生産拠点があり、そのうちリヤドが最も多い(約35%)。また、サウジアラビアは消費するチョコレートの約50%を生産しています。サウジアラビアのチョコレート消費量は、2023年から2030年にかけて4.45%のCAGRを記録し、2030年には約15億3,401万米ドルに達すると予測されます。

- クウェートはこの地域で最も急成長しているチョコレート市場です。クウェートのチョコレート市場は、2023年から2025年にかけて16.03%の成長が見込まれます。ダークチョコレートが主要カテゴリーで、2023年にはチョコレート市場全体の26.15%を占める。この成長は、同国の生活習慣病の割合が高いことに起因しています。クウェートは肥満率で世界第1位、糖尿病罹患率で世界第2位であり、2023年にはクウェート人口の77%が過体重、40%以上が肥満となっています。

中東のチョコレート市場動向

中東の若年層はイード、ラムザンなどの特別な機会にチョコレートを購入する傾向が強く、2022年のチョコレート部門の売上は40%以上を占める。

- 同地域は若者人口が多く、中東諸国の全人口がチョコレート需要の増加に寄与しています。サウジアラビアではミルクチョコレートが好まれ、中学生(13~16歳)前後に消費のピークを迎えるが、2022年にはUAEの消費者の40%がダークチョコレートを消費します。

- パッケージは消費者のチョコレート菓子の第一印象を決定づけ、購入の可能性を左右します。柔軟性のあるプラスチック製が最も人気があり、箱入りの詰め合わせや、場合によってはバーチョコレートに使用されるカートンもあります。

- 中東の消費者は高級チョコレート菓子類への関心を高め、贅沢な菓子類を選ぶようになっており、所得の増加や高級品志向の高まりに伴い、高級プレミアムチョコレート製品を求める傾向が強まっています。

- 中東の菓子類好きはよく知られているが、チョコレート菓子に対する欲求は変化しており、より健康的な素材へと徐々に移行しています。健康への配慮から、ダークチョコレートやナッツ入りチョコレートが人気となっています。

中東のチョコレート産業の概要

中東のチョコレート市場はかなり統合されており、上位5社で74.02%を占めています。この市場の主要企業は以下の通り。 Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA and Strauss Group Ltd.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子類

- ダークチョコレート

- ミルクチョコレートとホワイトチョコレート

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット/ハイパーマーケット

- その他

- 国名

- バーレーン

- クウェート

- オマーン

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他の中東

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Berry Callebaut

- Bostani Chocolatier Inc.

- Chocoladefabriken Lindt & Sprungli AG

- Dadash Baradar Industrial Co.

- Ferrero International SA

- IFFCO

- Lee Chocolate LLC

- Makaw Chocolate LLC

- Mars Incorporated

- Mondelez International Inc.

- Nestle SA

- Parand Chocolate Co.

- Patchi LLC

- Shirin Asal Food Industrial Group

- Strauss Group Ltd

- The Hershey Company

- YIldIz Holding AS

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001793

The Middle East Chocolate Market size is estimated at 2.84 billion USD in 2025, and is expected to reach 3.78 billion USD by 2030, growing at a CAGR of 5.86% during the forecast period (2025-2030).

Dominance of convenience stores and supermarkets/hypermarkets due to increased shopping facilities and brand availability led to chocolate sales in the region

- In the Middle East, the overall retailing segment has maintained a growth rate of 5.28% by value in 2023 as compared to 2022. The projected expansion is driven by consumers' increasing preference for convenience shopping facilities within the market. Within the retailing segment, the convenience stores segment is the largest retailing unit in terms of volume in 2023. Some of the popular convenience stores in the Middle East are Spinneys, LuLu Express, 7-Eleven, Zoom, Fresh Plus, and Circle K. By 2028, the convenience store segment in the Middle East is estimated to register a growth of 6.37% by volume.

- Supermarkets and hypermarkets are the second-largest channels in the Middle Eastern chocolate confectionery market. The channel grew by 4.77% by value in 2023 compared to 2022 in the overall distribution channels segment for the Middle East's chocolate confectionery sales in 2023. The development of modern retail channels such as supermarkets or hypermarkets has made it feasible for consumers to purchase high-quality chocolate products. The proximity factor of these channels in the countries provides them with an added advantage of influencing the consumer's decision to purchase among the large variety of products available in the market.

- Online channels are the fastest-growing distribution channels, attaining a CAGR of 6.43% from 2023 to 2030, through which chocolate confectionery products are consumed in the region. Consumers prefer online channels as they provide quick, convenient delivery options. The high internet penetration in the region also drives the demand for these channels. Among all the countries in the region, the United Arab Emirates and Saudi Arabia had the highest internet penetration, at 99% as of July 2023.

Substantial production and consumption of chocolates led by Saudi Arabia and UAE with value share of almost 70% in 2023

- The Middle Eastern chocolate market registered a growth of 5.28% by value in 2023 compared to 2022. The consumer demand for high-quality chocolate products, such as single-origin chocolates, organic chocolates, handmade chocolates, artisan chocolates, and other chocolate products, is a major factor driving the chocolate market across the region. Saudi Arabia and UAE were identified as the major markets in the region, which collectively accounted for a 63.38% value share in the overall chocolate sales in the region in 2023. The key driving factors are high production, rising consumer preference for premium chocolates, and adequate industry regulation to facilitate the manufacturing and trading of chocolates.

- Saudi Arabia is the largest chocolate producer in the GCC countries, supported by the highest consumption of chocolates in the country, including milk and dark chocolate products. As of 2023, there are more than 1,000 chocolate-producing sites in Saudi Arabia, with Riyadh accounting for the largest number of these (around 35%). Also, Saudi Arabia produces roughly 50% of the chocolate that it consumes. The consumption of chocolates in Saudi Arabia is anticipated to reach around USD 1534.01 million in 2030, registering a value CAGR of 4.45% between 2023 and 2030.

- Kuwait is the fastest-growing chocolate market in the region. The Kuwaiti chocolate market is anticipated to grow by a value of 16.03% during 2023-2025. Dark chocolate is the leading category, accounting for 26.15% of the value of the overall chocolate market in 2023. The growth is attributed to the country's higher rates of lifestyle disorders. Kuwait ranks first worldwide in obesity and second in diabetes rates, with 77% of Kuwait's population being overweight and over 40% obese in 2023.

Middle East Chocolate Market Trends

The younger population in the Middle East purchases more chocolates for special occasions such as Eid, Ramzan, and others, which resulted in more than 40% of sales in the chocolate segment in 2022

- The region has a large population of young people and the entire population in Middle Eastern countries, contributing to the increasing demand for chocolates in the region. In Saudi Arabia, milk chocolate is preferred, and consumption peaks around middle school age (13-16), while in 2022, 40% of UAE consumers consumed dark chocolate.

- Packaging remains consumers' first impression of chocolate confectioneries among other attributes, which determines the likelihood of purchasing. Flexible plastic is most popular, with some cartons used for boxed assortments and, in some cases, bars.

- Consumers in the Middle East are becoming more interested in premium chocolate confectionary items and are choosing luxurious confectionery, and they are increasingly seeking out high-end premium chocolate products in line with rising incomes and the increased desire for premium products.

- The Middle East's love of confectionery is well known but its appetite for chocolate confectionery is changing, gradually moving toward more healthy ingredients. Health concerns are making dark chocolate and chocolate with nuts popular options.

Middle East Chocolate Industry Overview

The Middle East Chocolate Market is fairly consolidated, with the top five companies occupying 74.02%. The major players in this market are Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA and Strauss Group Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Dark Chocolate

- 5.1.2 Milk and White Chocolate

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Bahrain

- 5.3.2 Kuwait

- 5.3.3 Oman

- 5.3.4 Qatar

- 5.3.5 Saudi Arabia

- 5.3.6 United Arab Emirates

- 5.3.7 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Berry Callebaut

- 6.4.2 Bostani Chocolatier Inc.

- 6.4.3 Chocoladefabriken Lindt & Sprungli AG

- 6.4.4 Dadash Baradar Industrial Co.

- 6.4.5 Ferrero International SA

- 6.4.6 IFFCO

- 6.4.7 Lee Chocolate LLC

- 6.4.8 Makaw Chocolate LLC

- 6.4.9 Mars Incorporated

- 6.4.10 Mondelez International Inc.

- 6.4.11 Nestle SA

- 6.4.12 Parand Chocolate Co.

- 6.4.13 Patchi LLC

- 6.4.14 Shirin Asal Food Industrial Group

- 6.4.15 Strauss Group Ltd

- 6.4.16 The Hershey Company

- 6.4.17 YIldIz Holding AS

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms