|

市場調査レポート

商品コード

1684008

ベトナムの殺菌剤市場:シェア分析、産業動向と統計、成長予測(2025年~2030年)Vietnam Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ベトナムの殺菌剤市場:シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 162 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

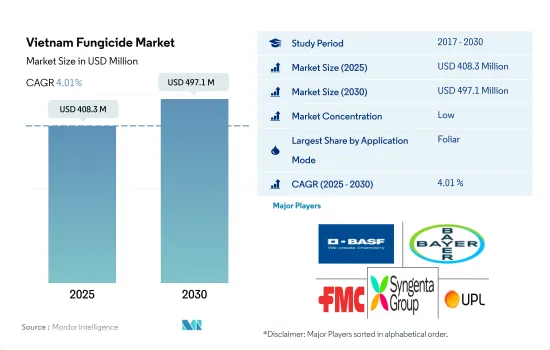

ベトナムの殺菌剤市場規模は2025年に4億830万米ドルと推定され、2030年には4億9,710万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは4.01%で成長すると予測されます。

害虫圧力の高まりが、様々な適用方法での殺虫剤需要を牽引している

- ベトナムの殺菌剤市場は、化学的散布、葉面散布、燻蒸、土壌治療など、さまざまな用途によって分類されます。これらの異なる散布方法は、国内の多様な農業状況において殺菌剤を効果的に散布するための重要な手段となっています。

- 葉面散布が市場を独占この分野の殺菌剤の市場価値は、予測期間中(2023~2029年)にCAGR 4.3%を記録すると予想されます。これは、葉が病害の主な発生場所である穀物、穀類、果物、野菜など、様々な作物に広く適用されるためです。

- ベトナムでは、植物の健康と生産性に重大な脅威をもたらす土壌媒介菌から保護するために、土壌治療が一般的に使用されています。作物の損失を避けるための予防措置として種子処理剤の採用が増加していることから、同市場のCAGRは4.0%になると予想されます。

- また、ベトナムでは、果物や野菜など、一貫して制御された散布が必要な作物には、化学灌漑法が一般的に使用されています。より多くの農家が殺菌剤を効率的に作物に散布する手段としてこの方法を採用しているため、予測期間(2023~2029年)にCAGR 3.8%を記録し、この分野は成長すると予想されます。

- 燻蒸は土壌の健全性を維持し、脆弱な作物への病原菌の拡散を防ぐのに役立つため、ベトナムの農業慣行において特に重要です。殺菌剤の製剤の改良とともに、燻蒸技術や設備の進歩が市場の成長に貢献すると予想されます。新しい技術と改良された燻蒸散布方法が殺菌剤の効率を高めているからです。

ベトナムの殺菌剤市場動向

気候の変化と病害圧力の上昇が殺菌剤の消費を促進する見込み

- ベトナムにおける殺菌剤の使用量は、2019年から2022年の間に1ヘクタール当たり31.2グラムの顕著な増加を経験しました。これは、農業慣行と植物保護における殺菌剤の需要拡大に寄与したいくつかの要因によるものと考えられます。

- ベトナムの農業面積は2022年に前年比1.7% ha増加しました。農業生産の拡大と、作物の収量と品質を向上させたいという願望により、殺菌剤の使用量が増加すると予想されます。ベトナムの農家は、増大する食糧需要を満たし、作物の生産性を向上させようと努力しています。

- 気候条件や環境要因の変化も、ベトナムにおける殺菌剤の消費を促進すると予想されます。気温と湿度の変化は、真菌病の開発と蔓延に好都合な条件を作り出す可能性があります。その結果、農家はこれらの病害に関連するリスクを軽減し、農作物を保護するために、殺菌剤への依存度を高めていくと予想されます。

- 病害管理と作物保護の重要性に対する認識と知識の高まりが、ベトナムの農家における殺菌剤の採用を後押ししています。病害の予防と管理に対する考え方の転換が、同国における殺菌剤の需要に拍車をかけています。

- さらに、殺菌剤製剤の進歩や、効果的で的を絞った幅広い殺菌剤製品が入手可能になったことも、使用量の増加に寄与しています。有効性と安全性が改善された革新的な殺菌剤の開発により、農家は病害防除の選択肢が増えました。このことは、総合的病害虫管理戦略の一環として殺菌剤を採用することをさらに後押ししています。

真菌性病害の増加と、国内における有効成分の輸入依存が、有効成分の価格を押し上げる可能性があります。

- ベトナムには幅広い農業気候地域があります。例えば、中部と北部の地方では、冬は冷涼から寒冷となり、温帯性の病原菌に有利となります。気温が低いため、作物によっては生育が阻害され、苗やその他の病気にかかりやすくなります。さらに、1年の天候サイクルには、非常に雨の多い時期と乾燥した時期があります。このような天候は作物にストレスを与え、特に病原菌による根や茎の病気を誘発します。テブコナゾール、アゾキシストロビン、メタラキシルは、ベトナムで一般的に使用されている殺菌活性成分です。

- テブコナゾールは、2022年に1トン当たり8,700米ドルと評価される系統殺菌剤を使用しています。テブコナゾールは、さび病、紋枯病、葉斑病、炭疽病を治療することが知られています。ベトナムはテブコナゾールの大半を中国、ドイツ、インドから輸入しています。

- アゾキシストロビンは、卵菌類、子のう菌類、子のう菌類、担子菌類に属する真菌類に有効な広域殺菌剤です。フザリウム菌やトリコデルマ菌のような真菌の蔓延が増加したため、アゾキシストロビンの価格は2017年の1トン当たり4,000米ドルから2022年には1トン当たり4,600米ドルに上昇しました。同様に、メタラキシルは、真菌によって引き起こされる植物病害を防除するために使用される浸透性殺菌剤であり、2022年にはメートルトン当たり4,400米ドルと評価されました。

- ベトナムでは、真菌性病害の増加とこれらの有効成分の輸入依存が、これらの有効成分の価格を押し上げる可能性があります。

ベトナムの殺菌剤産業の概要

ベトナムの殺菌剤市場は細分化されており、上位5社で29.06%を占めています。この市場の主要企業は以下の通り。 BASF SE, Bayer AG, FMC Corporation, Syngenta Group and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 種子治療

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001710

The Vietnam Fungicide Market size is estimated at 408.3 million USD in 2025, and is expected to reach 497.1 million USD by 2030, growing at a CAGR of 4.01% during the forecast period (2025-2030).

The rising pest pressure is driving the demand for insecticides in various application methods

- The fungicide market in Vietnam is categorized by various applications, including chemigation, foliar application, fumigation, and soil treatment. These different application methods serve as important means of effectively applying fungicides in diverse agricultural contexts within the country.

- Foliar application dominates the market. Fungicide's market value in this segment is expected to register a CAGR of 4.3% during the forecast period (2023-2029) because it is widely applied in various crops, including grains, cereals, fruits, and vegetables, where the foliage is the primary site of disease occurrence.

- Soil treatment is commonly used in Vietnam to protect from soil-borne fungi that pose a significant threat to the plant's health and productivity. The market is expected to register a CAGR of 4.0% due to the rising adoption of seed treatment chemicals as a preventive measure to avoid crop losses.

- The chemigation method is also commonly used in Vietnam for crops that require a consistent and controlled application, such as fruits and vegetables. The segment is expected to grow, registering a CAGR of 3.8% during the forecast period (2023-2029) because more farmers are adopting this practice as a means to efficiently deliver fungicides to their crops.

- Fumigation is particularly important in Vietnam's agricultural practices, as it helps maintain soil health and prevent the spread of pathogens to vulnerable crops. Advancements in fumigation technologies and equipment, along with improved formulations of fungicides, are expected to contribute to the growth of the market as new technologies and improved fumigation application methods are enhancing the efficiency of fungicides.

Vietnam Fungicide Market Trends

The changing climate and rising disease pressure are expected to drive the consumption of fungicides

- The usage of fungicides in Vietnam experienced a notable increase of 31.2 grams per hectare between 2019 and 2022. This can be attributed to several factors that have contributed to the growing demand for fungicides in agricultural practices and plant protection.

- Vietnam's agricultural acreage increased by 1.7% ha in 2022 from the previous year. The expansion of agricultural production and the desire to enhance crop yields and quality are expected to increase the usage of fungicides. Farmers in Vietnam are striving to meet the growing demand for food and improve the productivity of their crops.

- Changing climatic conditions and environmental factors are also expected to drive the consumption of fungicides in Vietnam. Shifts in temperature and humidity levels can create favorable conditions for the development and spread of fungal diseases. As a result, farmers are expected to increasingly rely on fungicides to mitigate the risks associated with these diseases and safeguard their crops.

- The increasing awareness and knowledge about the importance of disease management and crop protection have driven the adoption of fungicides among farmers in Vietnam. The shift in mindset toward disease prevention and management has fueled the demand for fungicides in the country.

- Additionally, advancements in fungicide formulations and the availability of a wide range of effective and targeted fungicide products have also contributed to increased usage. The development of innovative fungicides with improved efficacy and safety profiles has provided farmers with more options for disease control. This has further encouraged the adoption of fungicides as part of their integrated pest management strategies.

Increase in the fungal diseases, coupled with the dependence on imports for these active ingredients in the country, may drive the prices of these active ingredients

- Vietnam has a wide range of agroclimatic regions. For example, the central and northern provinces experience a cool to cold winter that favors temperate pathogens. The low temperatures inhibit the growth of some crops, making them more susceptible to seedlings and other diseases. Additionally, the yearly weather cycle includes very wet and dry periods. Such weather can also lead to crop stress and favor some diseases, especially of the roots and stems caused by pathogens. Tebuconazole, azoxystrobin, and metalaxyl are commonly used fungicide-active ingredients in Vietnam.

- Tebuconazole uses a systematic fungicide valued at USD 8.7 thousand per metric ton in 2022. Tebuconazole is known to treat rust fungus, sheath blight, leaf spot, and anthracnose. Vietnam imports most of its tebuconazole from China, Germany, and India.

- Azoxystrobin is a broad-spectrum fungicide active against fungal pathogens belonging to oomycetes, ascomycetes, deuteromycetes, and basidiomycetes. Owing to the increase in infestation of fungi like Fusarium and Trichoderma, the price of azoxystrobin increased from USD 4.0 thousand per metric ton in 2017 to USD 4.6 thousand per metric ton by 2022. Similarly, metalaxyl is a systemic fungicide used to control plant diseases caused by Oomycete fungi, valued at USD 4.4 thousand per metric ton in 2022.

- An increase in fungal diseases, coupled with dependence on imports for these active ingredients, in the country may drive the prices of these active ingredients.

Vietnam Fungicide Industry Overview

The Vietnam Fungicide Market is fragmented, with the top five companies occupying 29.06%. The major players in this market are BASF SE, Bayer AG, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Syngenta Group

- 6.4.8 UPL Limited

- 6.4.9 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms