|

市場調査レポート

商品コード

1683991

インドの除草剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)India Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの除草剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 167 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

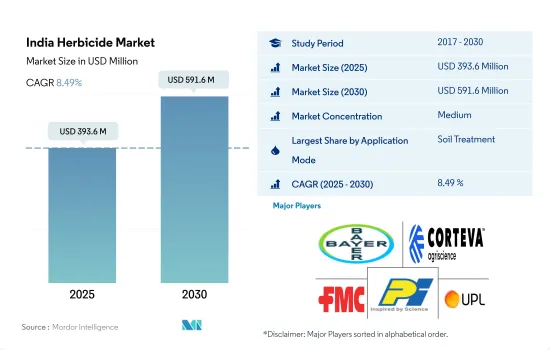

インドの除草剤市場規模は2025年に3億9,360万米ドルと推定され、2030年には5億9,160万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは8.49%で成長する見込みです。

最も重要な除草剤散布の主要モードは土壌治療散布である

- 雑草はインドの農業部門に大きな脅威をもたらし、年間約45.0%の大幅な作物損失をもたらしています。農家は、輪作、文化的慣行、手作業による除草、化学除草剤の散布など、さまざまな戦略を実施して雑草を防除しています。

- しかし、代替方法に伴う生産コストの上昇により、作物の雑草に対処するために化学除草剤を採用する農家が増えています。農家は除草剤を散布することで、雑草の成長を効率的に制御し、農業収量への悪影響を最小限に抑えることができます。

- 雑草防除にはさまざまな散布方法があります。除草剤を用いた土壌治療は、雑草の生育初期段階での管理に有効であるため、大きなシェアを占めています。この散布方法は、出穂前の雑草を防除するのに有利なため、穀物や穀類を栽培する農家の間で人気を博しています。

- 土壌治療は、除草剤を土壌に直接散布するもので、雑草の種子や生え始めた苗を効果的に狙い、その成長と定着を阻害することができます。土壌治療を行うことで、農家は雑草の問題に積極的に対処し、重要な初期段階で作物の健全な生育を促進することができます。

- 土壌治療に続いて、葉面散布や化学的散布といった他の散布方法も、国内では雑草防除のために人気が急上昇しています。これらのモードはその有効性を実証し、作物の生産性向上にさまざまなメリットをもたらしています。2022年には、葉面散布が33.2%、化学散布が18.7%と大きな市場シェアを記録しました。

インドの除草剤市場動向

作物の損失拡大による雑草の課題を管理するため、除草剤の消費拡大が予想されます。

- 機械化された化学ベースの雑草防除アプローチが、従来の手作業による除草方法に急速に取って代わりつつあります。農家は、小規模および大規模な農作業で雑草を管理する費用対効果が高く効率的な方法として除草剤を使用しています。

- インドでは、農作物の生産性を向上させる目的で、農家が作付けサイクルを1年以内に何度も繰り返す作物集約化を実践しています。この作物集約化によって雑草圧が高まることが多く、作物の生産性を維持するために除草剤の散布が必要となります。ヘクタール当たりの除草剤消費量は平均49.7 g/haでした。

- ヘクタール当たりの除草剤消費量は、作物の種類、雑草の侵入レベル、農業慣行、雑草管理戦略など多くの側面によって異なります。インドにおける1ヘクタール当たりの除草剤消費量は、2017年から2022年にかけて6.0%増加しました。インドの一人当たりの除草剤使用量は増加し、1ヘクタール当たりの平均農業生産高を押し上げました。除草剤の利点に対する農家の意識の高まりに加え、幅広い種類の除草剤が市場に出回っていることが、使用量の増加に寄与しています。

- 除草剤耐性綿(Bt綿)のような除草剤耐性の特性を持つ遺伝子組み換え(GM)作物の利用や、遺伝子組み換えのための「バーナーゼ/バースター」技術を用いたDMH-11のようなハイブリッド・マスタードの開発により、農家は雑草管理により幅広く除草剤を使用できるようになりました。これらの改良作物は特定の除草剤に耐えるように設計されており、農家は効果的な雑草防除のために除草剤をより多く利用できるようになりました。

アトラジン、パラコート、グリホサートは、インドで使用されている主な除草剤です。

- インドにはさまざまな農業気候と土壌があります。多様性の高い農業と農業システムは、さまざまな種類の雑草問題に悩まされています。雑草は、製品の品質を損ない、健康や環境に害を及ぼすだけでなく、10%から80%の作物収量の損失を引き起こしています。アトラジン、パラコート、グリホサートが、国内で使用されている主な除草剤です。

- アトラジンは、インドのトウモロコシや稲作において、エキノクロア、エルシン属、アマランサスビリジスなどの広葉雑草やイネ科雑草の防除に広く使用されている除草剤です。除草剤は2022年に1万3,500米ドルと評価されました。インドは世界最大のアトラジン技術輸入国であり、主に中国、イタリア、イスラエルから輸入しています。

- パラコートは広範囲の接触型除草剤で、2022年には4,600米ドルを占める。インドでは合計14種類のパラコートジクロライドの商品名が販売されています。穀物、豆類、油糧種子、野菜、換金作物など約25の作物に使用されています。しかし、中央殺虫剤委員会・登録委員会(CIBRC)が使用を承認しているのは9作物のみです。

- グリホサートは非選択性除草剤で、Cynodon dactylon、Imperata cylindrica、Arundinella bengalensisなどの雑草の防除に使用されます。2022年9月にインド政府が出した通達によると、グリホサートは茶園と非農耕地でのみ使用できます。2022年には1,100米ドルと評価されました。

- インド政府は、農村経済を活性化させ、農家の収入を増やすために継続的に予算支援を行ってきました。22年度予算では、農業セクターと農村経済の改善のため、多くの施策や取り組みが提案・発表されました。このことは、同国の除草剤価格にさらなる影響を与えると予想されます。

インドの除草剤産業の概要

インドの除草剤市場は適度に統合されており、上位5社で61.28%を占めています。この市場の主要企業は以下の通り。 Bayer AG, Corteva Agriscience, FMC Corporation, PI Industries and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Gharda Chemicals Ltd

- PI Industries

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001693

The India Herbicide Market size is estimated at 393.6 million USD in 2025, and is expected to reach 591.6 million USD by 2030, growing at a CAGR of 8.49% during the forecast period (2025-2030).

The primary mode of herbicide application of utmost significance is the soil treatment application

- Weeds pose a significant threat to the agricultural sector in India, resulting in substantial annual crop losses of around 45.0%. Farmers are implementing various strategies, including crop rotation, cultural practices, manual weeding, and spraying chemical herbicides to control weeds.

- However, due to rising production costs associated with alternative methods, more farmers are adopting chemical herbicides to tackle weeds in their crops. Farmers can efficiently control weed growth and minimize the detrimental effects on their agricultural yield by spraying herbicides.

- There are various application modes for weed control. Soil treatment using herbicides holds a prominent share due to its effectiveness in managing weeds during their early growth stages. This application method has gained popularity among farmers cultivating grain and cereal crops due to its advantageous effects in controlling pre-emergence weeds.

- Soil treatment involves applying herbicides directly to the soil, where they can effectively target weed seeds and emerging seedlings, inhibiting their growth and establishment. By employing soil treatment applications, farmers can proactively address weed issues and promote healthier crop growth in the crucial early stages.

- Following the soil treatment mode, other application modes such as foliar and chemigation have witnessed a surge in popularity for weed control in the country. These modes have demonstrated their effectiveness and offered various benefits in enhancing crop productivity. In 2022, foliar and chemigation registered a significant market share of 33.2% and 18.7%, respectively.

India Herbicide Market Trends

Herbicide consumption is anticipated to expand to manage the weed challenges due to growing losses of crops

- Mechanized and chemical-based weed control approaches are rapidly replacing traditional manual weeding methods. Farmers use herbicides as a cost-effective and efficient way to manage weeds in small-scale and large-scale farming operations.

- With the aim of increasing crop productivity, farmers in India have been practicing crop intensification, which involves repeated cropping cycles within a year. This intensification frequently results in increased weed pressure, necessitating the application of herbicides to maintain crop productivity. The average herbicide consumption per hectare accounted for 49.7 g/ha.

- Herbicide consumption per hectare can vary based on numerous aspects such as crop type, weed infestation level, agricultural practices, and weed management strategies. The consumption of herbicides in India per hectare increased by 6.0% from 2017 to 2022. Herbicide usage per capita in India increased to boost the average agricultural output per hectare. Farmers' growing awareness of the advantages of herbicides, along with the availability of a wide range of herbicides on the market, has contributed to their increased usage.

- The utilization of genetically modified (GM) crops that possess herbicide-tolerant characteristics, like herbicide-tolerant cotton (Bt cotton), and the development of hybridized mustard such as DMH-11 using the "barnase/barstar" technique for genetic modification has enabled farmers to employ herbicides more extensively in weed management. These modified crops are designed to endure specific herbicides, empowering farmers to utilize herbicides to a greater extent for effective weed control.

Atrazine, paraquat, and glyphosate are major herbicides used in the country

- India has a wide range of agroclimates and soil types. The highly diverse agriculture and farming systems are beset with different types of weed problems. Weeds cause 10% to 80% crop yield losses, besides impairing product quality and causing health and environmental hazards. Atrazine, paraquat, and glyphosate are major herbicides used in the country.

- Atrazine is an herbicide widely used to control broadleaf and grassy weeds like Echinocloa, Elusine spp, and Amaranthus viridis in maize and rice crops in India. The herbicide was valued at USD 13.5 thousand in 2022. India is the world's largest importer of Atrazine technical and imports majorly from China, Italy, and Israel.

- Paraquat is a broad-spectrum contact herbicide, accounting for USD 4.6 thousand in 2022. A total of 14 commercial names of paraquat dichloride are sold in India. It is used in about 25 crops, including cereals, pulses, oil seeds, vegetables, and cash crops. However, the Central Insecticide Board & Registration Committee (CIBRC) has approved its use in only nine crops.

- Glyphosate is a non-selective herbicide used to control weeds like Cynodon dactylon, Imperata cylindrica, and Arundinella bengalensis. As per the notice issued by the Government of India in September 2022, glyphosate can be used only in tea gardens and non-crop areas. It was valued at USD 1.1 thousand in 2022.

- The Government of India has continuously provided budgetary support to revive the rural economy and increase farmers' income. A number of measures and initiatives were proposed and announced during the FY22 budget for the improvement of the agriculture sector and the rural economy. This is expected to influence the prices of herbicides in the country further.

India Herbicide Industry Overview

The India Herbicide Market is moderately consolidated, with the top five companies occupying 61.28%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, PI Industries and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Gharda Chemicals Ltd

- 6.4.7 PI Industries

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms